What Is the FICA Tax Rate for 2026?

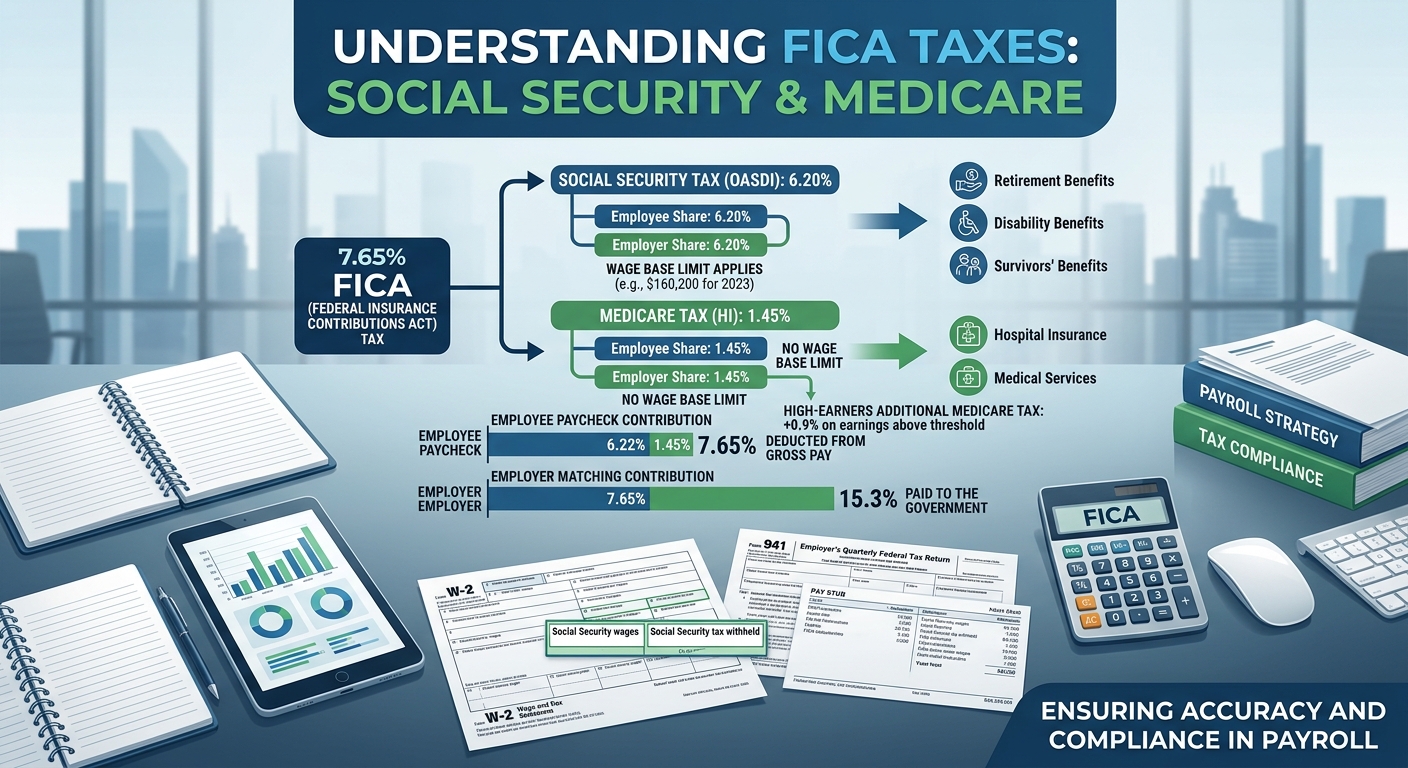

The FICA tax rate for 2026 remains at 15.3% total, split equally between employers and employees at 7.65% each. This breaks down into 6.2% for Social Security tax (capped at wages up to $176,100 for 2026) and 1.45% for Medicare tax (with no wage cap). High earners face an additional 0.9% Medicare surtax on wages exceeding $200,000 for single filers or $250,000 for married couples filing jointly. If you’re a W-2 employee, your employer withholds your 7.65% share automatically. If you’re self-employed, you pay the full 15.3% as self-employment tax, but you can deduct half of it on your Form 1040.

Most taxpayers don’t think about FICA until they see the deduction on their paycheck or scramble to estimate quarterly taxes. By then, it’s too late to optimize. Understanding how the FICA tax works in 2026 means you can plan smarter, reduce your overall tax burden if you’re self-employed, and avoid costly surprises at year-end.

How the 2026 FICA Tax Rate Breaks Down

FICA stands for the Federal Insurance Contributions Act, the law that funds Social Security and Medicare. The system operates on a pay-as-you-go model: current workers fund benefits for current retirees. Here’s the exact breakdown for 2026:

Social Security Tax Component

The Social Security portion is 6.2% for employees and 6.2% for employers, totaling 12.4%. This tax applies only to wages up to the annual wage base limit. For 2026, that limit is $176,100. Any income you earn above this threshold is exempt from Social Security tax. If you earn $200,000 in W-2 wages, you’ll pay Social Security tax on the first $176,100 only, saving you $1,482 in Social Security withholding on the remaining $23,900.

Medicare Tax Component

The Medicare portion is 1.45% for employees and 1.45% for employers, totaling 2.9%. Unlike Social Security, there’s no wage cap on Medicare tax. Whether you earn $50,000 or $5 million, every dollar is subject to the 1.45% Medicare tax. High-income earners also face the Additional Medicare Tax of 0.9% on wages exceeding $200,000 (single) or $250,000 (married filing jointly). This additional tax is withheld only from the employee’s share, not matched by employers.

Self-Employment Tax for 1099 Contractors and Business Owners

If you’re self-employed, you pay both the employee and employer portions, which totals 15.3% on net self-employment income. This is called self-employment tax, and it’s calculated on Schedule SE. The good news: you can deduct 50% of your self-employment tax on Line 15 of Schedule 1, reducing your adjusted gross income. For example, if you have $100,000 in net self-employment income, you’ll owe $15,300 in self-employment tax but can deduct $7,650, lowering your taxable income to $92,350.

For detailed guidance on managing payroll and bookkeeping for your business, explore our bookkeeping and payroll services to ensure compliance and optimize your tax position.

Who Pays FICA Tax in 2026?

Nearly every working American pays FICA tax, but the mechanics differ based on employment type. Here’s who pays and how:

W-2 Employees

If you receive a W-2 from an employer, your FICA taxes are automatically withheld from each paycheck. Your employer matches your contribution dollar-for-dollar. You don’t file anything separately for FICA; it’s already handled through payroll withholding. Your employer reports your wages and withheld taxes on your W-2, which you use to file your annual tax return. This system is simple but offers limited control. You can’t reduce FICA taxes on W-2 income through deductions or credits.

Self-Employed Individuals (1099 Contractors, Freelancers, Sole Proprietors)

Self-employed individuals pay self-employment tax, which covers both the employee and employer portions of FICA. You calculate this tax on Schedule SE and report it on Schedule 1 of Form 1040. The IRS requires you to pay estimated taxes quarterly if you expect to owe $1,000 or more in tax for the year. Miss a quarterly payment, and you’ll face underpayment penalties plus interest. The self-employment tax applies to net earnings from self-employment, which is your gross income minus business deductions. Maximize your deductions to lower your taxable profit and reduce your self-employment tax liability.

S Corporation Owners

S Corp owners occupy a unique position. You must pay yourself a reasonable salary subject to FICA tax, but profits distributed as shareholder distributions are exempt from FICA. This creates substantial tax savings. For example, if your S Corp generates $150,000 in profit and you pay yourself a $60,000 salary, you pay FICA on $60,000 only. The remaining $90,000 in distributions avoids the 15.3% self-employment tax, saving you $13,770 annually. The IRS scrutinizes S Corp salaries closely, so your salary must reflect industry standards for your role and experience. Setting it too low can trigger audits and reclassification of distributions as wages.

LLC Owners

Single-member LLCs are treated as sole proprietorships for tax purposes, meaning you pay self-employment tax on all net income. Multi-member LLCs taxed as partnerships follow the same rule: each partner pays self-employment tax on their share of partnership income. However, LLCs can elect S Corp taxation by filing Form 2553 with the IRS, allowing you to split income into salary (subject to FICA) and distributions (exempt from FICA). This election can save five-figure amounts annually for profitable businesses.

2026 FICA Tax Rate vs. 2025: What Changed?

The FICA tax rate itself hasn’t changed. It remains 15.3% total (12.4% Social Security + 2.9% Medicare). What does change annually is the Social Security wage base limit, which adjusts for inflation. For 2025, the wage base was $168,600. For 2026, it increased to $176,100, a $7,500 jump. This means higher earners will pay more Social Security tax in 2026. If you earn above the wage base in both years, you’ll pay an additional $465 in Social Security tax in 2026 ($7,500 x 6.2%).

The Additional Medicare Tax thresholds did not change. They remain $200,000 for single filers and $250,000 for married couples filing jointly. If your income exceeds these thresholds, you owe an extra 0.9% on the excess.

Common FICA Tax Mistakes That Cost Taxpayers Thousands

Red Flag Alert: Treating All Income the Same

Not all income is subject to FICA tax. Investment income, rental income (unless you’re a real estate professional), capital gains, and retirement distributions are exempt. Many taxpayers assume every dollar they earn is subject to FICA, leading to unnecessary tax anxiety. Only earned income from wages or self-employment triggers FICA obligations. If you’re retired and living on Social Security, pension income, and investment dividends, you owe zero FICA tax.

Red Flag Alert: Ignoring the Self-Employment Tax Deduction

Self-employed taxpayers often overlook the deduction for 50% of self-employment tax. This deduction appears on Schedule 1, Line 15, and reduces your adjusted gross income. It’s not an itemized deduction; you can claim it even if you take the standard deduction. Missing this deduction can cost you thousands in additional income tax. For example, if you owe $15,300 in self-employment tax, the $7,650 deduction saves you approximately $1,682 in federal income tax if you’re in the 22% bracket.

Red Flag Alert: Setting an Unreasonably Low S Corp Salary

S Corp owners sometimes set their salary at $20,000 or $30,000 to minimize FICA taxes, even when their business generates $200,000+ in profit. The IRS can reclassify distributions as wages, assess back taxes, penalties, and interest. Reasonable compensation is determined by factors like your role, hours worked, industry standards, and business profitability. The IRS uses comparable salary data from the Bureau of Labor Statistics and industry surveys. A safe approach: set your salary between 40% and 60% of total business income, adjusted for your specific circumstances.

Red Flag Alert: Missing Quarterly Estimated Tax Payments

Self-employed individuals must pay estimated taxes quarterly (April 15, June 15, September 15, and January 15 of the following year). These payments cover both income tax and self-employment tax. If you underpay by more than 10%, the IRS assesses underpayment penalties, typically around 8% annually. For someone owing $20,000 in annual self-employment tax, missing quarterly payments can result in $800 to $1,600 in penalties.

How to Reduce Your FICA Tax Burden Legally

Pro Tip: Elect S Corp Status for Your LLC

If your business generates consistent profit above $60,000 annually, S Corp taxation can save significant FICA taxes. You’ll need to run payroll, file Form 941 quarterly, and issue yourself a W-2, but the tax savings often justify the administrative costs. Many business owners save $8,000 to $15,000 annually through this strategy. Work with a tax professional to determine the optimal salary-to-distribution ratio for your situation.

Pro Tip: Maximize Business Deductions to Lower Net Self-Employment Income

Self-employment tax is calculated on net earnings, not gross revenue. Every dollar you deduct reduces both income tax and self-employment tax. Common overlooked deductions include home office expenses, mileage (67 cents per mile for 2026), health insurance premiums, retirement contributions (SEP-IRA or Solo 401(k)), professional development, and software subscriptions. If you’re a consultant earning $120,000 in gross income and you claim $30,000 in deductions, your self-employment tax drops from $18,360 to $13,770, saving you $4,590.

Pro Tip: Use Retirement Plans to Shelter Income

Contributions to SEP-IRAs, Solo 401(k)s, and SIMPLE IRAs reduce your taxable income but not your self-employment tax (you still pay SE tax on the income before contributing). However, the income tax savings can be substantial. For 2026, you can contribute up to $24,500 to a Solo 401(k) as an employee deferral, plus up to 25% of your compensation as an employer contribution, for a total potential contribution of $72,000 (or $80,000 if you’re 50 or older).

Pro Tip: Hire Your Children

If you’re a sole proprietor and you hire your child under age 18, their wages are exempt from Social Security and Medicare taxes. You can pay them a reasonable wage for legitimate work (filing, data entry, social media management), deduct the expense, and shift income into their lower tax bracket. If you pay your 16-year-old $12,000 for part-time work, you save $1,836 in self-employment tax (12,000 x 15.3%) plus income tax at your marginal rate. Your child can use the standard deduction to shelter most or all of that income from federal income tax.

FICA Tax for High Earners: The Additional Medicare Tax

High-income taxpayers face an extra 0.9% Medicare tax on earned income exceeding $200,000 (single) or $250,000 (married filing jointly). This Additional Medicare Tax is not matched by employers. It applies only to the employee portion. For example, if you’re single and earn $250,000 in W-2 wages, you’ll owe an extra $450 in Additional Medicare Tax on the $50,000 above the threshold ($50,000 x 0.9%).

Employers are required to withhold the Additional Medicare Tax once your year-to-date wages exceed $200,000, regardless of your filing status. If you’re married and your spouse also works, you might owe the tax even if neither of you individually exceeds the threshold. You reconcile any underwithholding or overwithholding when you file your tax return.

High earners can’t avoid this tax, but they can plan for it by adjusting withholding or increasing estimated tax payments to avoid a surprise bill in April.

California-Specific Considerations for FICA Tax

California does not impose a state-level FICA tax. FICA is a federal tax only, funding Social Security and Medicare at the national level. However, California employers must comply with State Disability Insurance (SDI) withholding, which is separate from FICA. For 2026, the SDI rate is 1.1% on wages up to $176,100 (the same wage base as Social Security). This is withheld from employees only; employers do not match it.

California also has its own Paid Family Leave (PFL) program, funded through SDI contributions. Self-employed individuals in California can opt into SDI coverage voluntarily through the state’s Elective Coverage program, but this does not affect federal FICA obligations.

If you operate a business in California, ensure you’re compliant with both federal payroll tax requirements and California’s SDI and PFL programs. Penalties for noncompliance can be severe.

KDA Case Study: Small Business Owner

Meet Jasmine, a 38-year-old marketing consultant operating as a single-member LLC in Sacramento. In 2025, her business generated $145,000 in net profit. As a sole proprietor for tax purposes, she paid self-employment tax on the entire amount, totaling $22,185 (15.3% x $145,000). She also faced a steep income tax bill and felt like she was working harder but keeping less.

KDA advised Jasmine to elect S Corp status for 2026 by filing Form 2553. We helped her establish a reasonable salary of $65,000 based on industry data for marketing consultants with her experience. The remaining $80,000 in profit was distributed as shareholder distributions, exempt from self-employment tax. Her FICA tax dropped to $9,945 (15.3% x $65,000), saving her $12,240 in the first year. We also set up a Solo 401(k), allowing her to contribute $24,500 in employee deferrals plus $13,000 in employer profit-sharing contributions, further reducing her taxable income.

Total tax savings in year one: $18,900. Jasmine paid KDA $4,200 for S Corp setup, payroll processing, and tax planning. Her first-year ROI was 4.5x, and the savings continue every year she operates as an S Corp.

Ready to see how we can help you? Explore more success stories on our case studies page to discover proven strategies that have saved our clients thousands in taxes.

Step-by-Step: How to Calculate Your 2026 FICA Tax

Step 1: Determine Your Employment Type

Are you a W-2 employee, self-employed, or an S Corp owner? Your employment classification determines your FICA calculation method. W-2 employees have FICA withheld automatically. Self-employed individuals calculate self-employment tax on Schedule SE. S Corp owners pay FICA on salary only.

Step 2: Calculate Your Social Security Tax

Multiply your wages or net self-employment income by 6.2% (employee portion) or 12.4% (if self-employed). If your income exceeds $176,100, apply the tax only to the first $176,100. For example, $150,000 in wages results in $9,300 in Social Security tax ($150,000 x 6.2%).

Step 3: Calculate Your Medicare Tax

Multiply your total wages or net self-employment income by 1.45% (employee portion) or 2.9% (if self-employed). There’s no wage cap. If you earn $150,000, your Medicare tax is $2,175 ($150,000 x 1.45%).

Step 4: Apply the Additional Medicare Tax (If Applicable)

If your income exceeds $200,000 (single) or $250,000 (married filing jointly), multiply the excess by 0.9%. For example, if you’re single and earn $220,000, you owe an additional $180 in Medicare tax ($20,000 x 0.9%).

Step 5: Combine and Report

Add your Social Security and Medicare taxes together. W-2 employees see this on their paystub and W-2 (Box 4 for Social Security, Box 6 for Medicare). Self-employed individuals report it on Schedule SE and Schedule 1 of Form 1040.

Ready to Reduce Your Tax Bill?

KDA Inc. specializes in strategic tax planning for business owners, S Corps, LLCs, and high-net-worth individuals. Book a personalized consultation and walk away with a clear plan.

Frequently Asked Questions About the FICA Tax Rate in 2026

Do I Pay FICA Tax on Retirement Income?

No. Social Security benefits, pension distributions, IRA withdrawals, and 401(k) distributions are not subject to FICA tax. FICA applies only to earned income from wages or self-employment. Once you retire, your FICA obligations end, though you may owe income tax on retirement distributions.

Can I Get a Refund of FICA Taxes?

Generally, no. FICA taxes fund Social Security and Medicare benefits you may receive in the future. They are not refundable like income tax overpayments. However, if you worked for two employers in the same year and your combined wages exceeded the Social Security wage base, you may have overpaid Social Security tax. You can claim the excess as a credit on Line 11 of Schedule 3.

What Happens If I Don’t Pay Self-Employment Tax?

The IRS treats unpaid self-employment tax like any other unpaid tax. You’ll face penalties, interest, and potential collection actions, including liens and levies. Additionally, failing to pay self-employment tax means you’re not earning Social Security credits, which could reduce your future Social Security benefits. You need 40 credits (typically 10 years of work) to qualify for retirement benefits.

Do S Corp Distributions Count as Earned Income for FICA?

No. Only your W-2 salary from the S Corp is subject to FICA tax. Distributions are not considered earned income and are exempt from self-employment tax. This is the primary tax advantage of S Corp election. However, you must pay yourself a reasonable salary. Taking zero salary and maximum distributions will trigger IRS scrutiny.

How Do I Know If My S Corp Salary Is Reasonable?

The IRS considers factors like your job duties, qualifications, time spent, company profitability, and compensation for comparable positions in your geographic area and industry. A common rule of thumb: your salary should represent 40% to 60% of total business income, though this varies by profession. Use Bureau of Labor Statistics data or compensation surveys as benchmarks. Document your reasoning in case of an audit.

What This Means for 2026 Tax Planning

The FICA tax rate for 2026 remains steady at 15.3%, but the rising Social Security wage base means higher earners will pay more. If you’re self-employed or running a profitable business, strategic planning can save you thousands. Electing S Corp status, maximizing deductions, and properly structuring compensation are all proven strategies to reduce your FICA burden legally.

Don’t wait until tax season to address FICA planning. The decisions you make now about entity structure, payroll setup, and income allocation will determine how much you keep versus how much you send to the IRS.

Key Takeaway: Understanding the FICA tax rate for 2026 and how it applies to your specific situation is the first step toward reducing your tax liability and maximizing your take-home income.

This information is current as of 5/31/2026. Tax laws change frequently. Verify updates with the IRS or FTB if reading this later.

Stop Overpaying FICA Taxes in 2026

If you’re tired of watching thousands disappear to payroll taxes every year, it’s time to take control. Whether you’re a W-2 employee exploring side income strategies, a 1099 contractor drowning in self-employment tax, or a business owner wondering if S Corp election makes sense, we can help you build a tax strategy that keeps more money in your pocket. Book a personalized consultation with KDA’s strategy team and discover exactly how much you could save this year. Click here to book your tax strategy session now.