Quick Answer

The federal gift tax exclusion 2026 stands at $15 million per person ($30 million per married couple), up from $13.99 million in 2025. This means high-net-worth individuals can transfer up to $15 million during their lifetime without triggering federal gift or estate tax. For California residents, this increase creates strategic planning opportunities to move wealth efficiently, especially given the state’s proposed Billionaire Tax Act targeting net worth over $1 billion.

What the $15 Million Federal Gift Tax Exclusion Actually Means

Most taxpayers hear “$15 million exclusion” and assume it only matters to billionaires. Wrong.

The federal gift tax exclusion 2026 is a unified lifetime exemption that applies to both gifts you make while alive and assets you leave when you die. Think of it as a single $15 million coupon you can use across your entire life. Every taxable gift you make chips away at this exclusion. When you die, whatever you haven’t used protects your estate from federal taxes.

Here’s what catches people off guard: California has no state estate tax, but it does have complicated probate rules and income tax traps that can cost heirs six figures even when federal estate tax isn’t owed. The 2026 exclusion increase gives wealthy families a short window to lock in transfers before these rules potentially sunset in 2026.

How the Unified Credit System Works

The IRS treats gifts and estate transfers as one integrated system. Under IRC Section 2505, you receive a lifetime credit equal to the tax on $15 million. Use $3 million of your exclusion on lifetime gifts? Your estate exemption drops to $12 million at death.

The math: Gift tax rate is a flat 40% above the exclusion. On a $20 million estate with a $15 million exclusion, you’d owe $2 million in federal estate tax on the $5 million overage. California doesn’t add a state estate tax, but your heirs still face California income tax on inherited retirement accounts, rental income on inherited property, and capital gains if they sell appreciated assets.

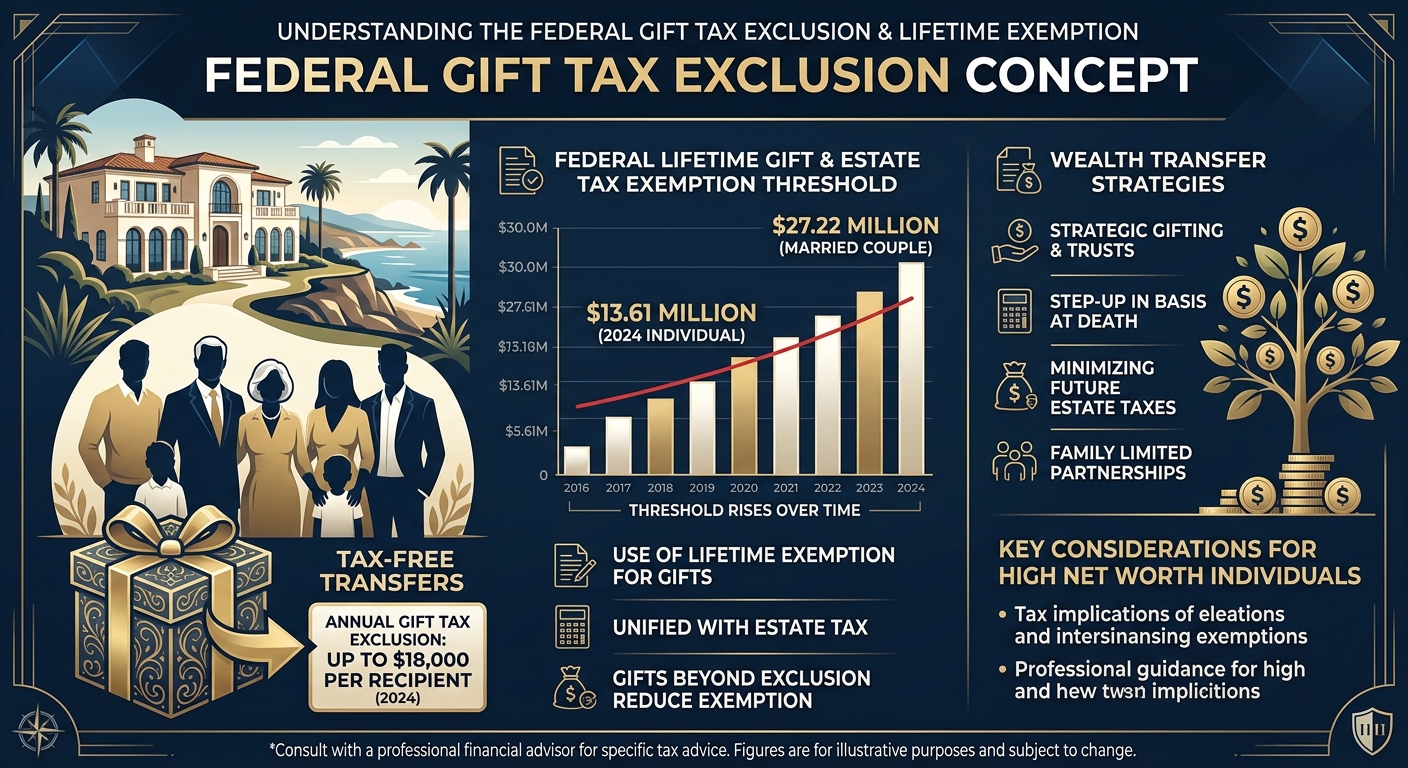

Annual Exclusion vs. Lifetime Exclusion

Don’t confuse the two. The 2026 annual gift exclusion remains at $18,000 per recipient ($36,000 if married filing jointly). You can give $18,000 to as many people as you want each year without filing Form 709 or touching your $15 million lifetime exemption.

Strategy: A married couple with three adult children and six grandchildren can gift $324,000 per year ($18,000 × 9 people × 2 spouses) completely tax-free, forever, without reducing their combined $30 million lifetime exclusion.

Why High-Net-Worth Californians Must Act Before 2027

The current $15 million exclusion expires on December 31, 2025, unless Congress extends it. Without action, the exemption drops to roughly $7 million per person (adjusted for inflation) starting January 1, 2026. That’s an $8 million reduction in tax-free transfer capacity per person, or $16 million per married couple.

For California high-net-worth individuals, this creates a compound problem. Not only does federal capacity shrink, but California’s proposed Billionaire Tax Act would impose a one-time 5% levy on net worth exceeding $1 billion for residents as of January 1, 2026. Even if you’re not a billionaire, the political momentum toward wealth taxation makes strategic gifting more urgent.

The Sunset Cliff: What Actually Happens

The Tax Cuts and Jobs Act of 2017 doubled the estate tax exemption temporarily. The increase was always scheduled to expire after 2025. IRS Revenue Procedure 2022-32 clarified that taxpayers who make large gifts under the current high exemption won’t be penalized if the exemption later drops. This “anti-clawback” rule protects completed gifts even if you die after 2025 when the exemption is lower.

Translation: If you gift $14 million in 2026 using the current exclusion, and the exemption drops to $7 million in 2027, the IRS won’t claw back the extra $7 million when you die. Your estate calculation uses the higher of the exclusion in effect when you made the gift or when you died.

Deadline pressure: Gifts must be completed by December 31, 2025 to lock in the $15 million exemption. “Completed” means legal title transfers to the recipient, not just signing documents. For real estate, that means recorded deeds. For business interests, that means updated operating agreements and capital accounts.

Advanced Gifting Strategies Using the 2026 Exclusion

Simply writing a $15 million check to your kids isn’t always the smartest move. Strategic gifting combines the exclusion with valuation discounts, income tax planning, and asset protection to multiply the benefit.

Spousal Lifetime Access Trusts (SLATs)

A SLAT lets you gift assets to an irrevocable trust for your spouse’s benefit, removing the assets from your taxable estate while maintaining indirect access. Your spouse can receive distributions from the trust during life, and remaining assets pass to your children estate-tax-free at death.

The setup: You gift $15 million of appreciated stock to a SLAT in 2026. Your spouse is the beneficiary, with your children as remainder beneficiaries. The $15 million (plus all future growth) is removed from your estate. If your spouse needs funds, the trustee can distribute to them. At their death, the trust continues for your kids without estate tax.

California advantage: Because California is a community property state, careful planning around separate vs. community property becomes critical. Gifts of community property require spousal consent. Gifts of separate property (owned before marriage or received by gift/inheritance) can be made without spousal joinder, but proper characterization documentation is essential.

Grantor Retained Annuity Trusts (GRATs)

A GRAT lets you transfer appreciating assets while retaining an annuity payment for a term of years. If the assets grow faster than the IRS Section 7520 rate (currently 5.6% for May 2026), the excess growth passes to beneficiaries gift-tax-free.

Real-world example: You own $10 million in privately held business stock you expect to grow 15% annually. You contribute it to a 2-year GRAT with annuity payments totaling $10.4 million. If the business grows as projected to $13.2 million, the $2.8 million excess passes to your kids without using any gift tax exclusion. The GRAT “uses” only a small fraction of your exemption (the present value of the remainder interest, which can be structured near zero).

The risk: If you die during the GRAT term, the assets return to your estate. That’s why shorter GRAT terms (2-3 years) are popular despite lower wealth transfer potential.

Qualified Personal Residence Trusts (QPRTs)

A QPRT removes your primary or vacation home from your estate at a discounted value. You gift the home to an irrevocable trust but retain the right to live there rent-free for a specified term (typically 10-20 years). At the end of the term, the home belongs to the trust beneficiaries (usually your children).

The discount comes from the IRS actuarial calculation. A $5 million home transferred via a 15-year QPRT might have a taxable gift value of only $2.1 million (using May 2026 Section 7520 rates and assuming you’re age 60). You’ve moved a $5 million asset using only $2.1 million of your $15 million exclusion.

California wrinkle: Your property tax basis under Proposition 19 may reset when the home transfers to your children, unless they use it as their primary residence. For a $5 million home, reassessment could mean $50,000+ in annual property tax increases. Factor this into your planning.

Red Flag Alert: Common Federal Gift Tax Mistakes

The IRS audits large gift tax returns more aggressively than most tax filings. Gift tax returns (Form 709) don’t have a statute of limitations until you file them, meaning the IRS can audit decades-old transfers if you never disclosed them properly.

Mistake 1: Not Filing Form 709 When Required

You must file Form 709 by April 15 of the year after making a taxable gift (gifts exceeding the $18,000 annual exclusion). Extensions for your income tax return automatically extend your gift tax return deadline to October 15, but you must request the extension by the April deadline.

Penalty: Failure to file Form 709 means the statute of limitations never starts running. The IRS can challenge the valuation of a gift you made 20 years ago if you never reported it. Even if no tax is owed (because you’re under the $15 million lifetime exclusion), the reporting requirement still applies.

Mistake 2: Inadequate Valuation Documentation

Claiming a 40% lack of marketability discount on private business interests without a qualified appraisal is an audit magnet. The IRS will revalue the gift and assess penalties if your valuation doesn’t meet the adequate disclosure standard under Treasury Regulation Section 301.6501(c)-1(e).

The fix: Obtain a qualified appraisal from an accredited appraiser (ASA, ABV, or CBA designation) before filing Form 709. Attach the full appraisal to your return, not just a summary. This starts the statute of limitations running (typically three years) and limits the IRS’s ability to challenge your valuation later.

Mistake 3: Retaining Too Much Control Over Gifted Assets

If you gift business interests to your children but retain voting control, decision-making authority, or the ability to revoke the transfer, the IRS may argue the gift was incomplete under IRC Section 2511. Incomplete gifts don’t use your exclusion and remain in your taxable estate.

Case law: In Estate of Powell (T.C. Memo 2011-94), the Tax Court found that transfers to a family partnership were incomplete because the donor retained the power to change partnership terms. The transferred assets were pulled back into the estate, costing the family over $4 million in unnecessary estate tax.

KDA Case Study: Real Estate Investor

Meet David Chen, a 62-year-old California real estate investor with a $22 million portfolio of commercial properties and marketable securities. David’s estate was on track to owe approximately $2.8 million in federal estate tax when the exemption drops in 2027 (calculated as 40% tax on $7 million excess over the projected $7 million exemption).

David came to KDA in March 2026 concerned about the sunset provision. He wanted to protect his wealth for his two adult children but needed liquidity for living expenses and didn’t want to lose control of his rental properties.

Our strategy: We established two Spousal Lifetime Access Trusts, one for each spouse (David and his wife each gifted $12 million of their $15 million exemption). We transferred $24 million of David’s real estate portfolio using conservative appraisals showing 25% lack of marketability discounts for the properties (fractional interests in LLCs holding the real estate). The actual transferred value was approximately $18 million in real property after discounts.

Tax savings result: By acting in 2026, David locked in $24 million of exemption that would have dropped to approximately $14 million in 2027. This removed $10 million from his taxable estate, saving $4 million in future estate tax. The properties continue generating $420,000 in annual rental income inside the trusts, which can be distributed to David’s wife if needed. At current appreciation rates (4% annually), the $18 million in real estate will grow to approximately $26.3 million over 10 years, all estate-tax-free.

Cost: David paid $18,500 for qualified appraisals, $24,000 for trust drafting and LLC restructuring, and $3,200 for gift tax return preparation. Total cost: $45,700.

First-year ROI: $4 million in future estate tax savings for $45,700 in upfront costs equals an 87.5x return on investment.

Ready to see how we can help you? Explore more success stories on our case studies page to discover proven strategies that have saved our clients thousands in taxes.

How to Calculate Your Remaining Gift Tax Exclusion

Most high-net-worth individuals have already used a portion of their lifetime exclusion through prior gifts. Here’s how to calculate what you have left.

Step 1: Gather All Prior Gift Tax Returns

Pull every Form 709 you’ve ever filed. You need the total amount of adjusted taxable gifts reported across all years. Don’t include annual exclusion gifts (under $18,000 per recipient per year), as those don’t count against your lifetime exclusion.

Step 2: Add Up Cumulative Taxable Gifts

Sum the “taxable gifts” column from Part 2, line 3 of every Form 709. This is your cumulative lifetime taxable gifts to date.

Step 3: Subtract From Current Exclusion

Take the 2026 exemption ($15 million) and subtract your cumulative taxable gifts. The result is your remaining available exclusion.

Example: You gifted $500,000 to your daughter in 2018 for a down payment (after applying your $15,000 annual exclusion, the taxable gift was $485,000). You gifted $2 million in business interests to your son in 2022. Your cumulative taxable gifts total $2,485,000. Your remaining 2026 exclusion is $12,515,000 ($15,000,000 minus $2,485,000).

Special Calculation: Portability from Deceased Spouse

If your spouse died after 2010 and their estate elected portability on Form 706, you inherited their unused exclusion amount. This “deceased spousal unused exclusion amount” (DSUE) is added to your own $15 million exemption.

Check your deceased spouse’s Form 706, Part 6, line 9c for the DSUE amount. Add this to your remaining exclusion. A surviving spouse could have up to $30 million in combined exclusion if their spouse died without using any exemption and portability was properly elected.

California-Specific Estate Planning Considerations

Federal gift tax rules apply nationwide, but California’s unique laws create additional planning layers high-net-worth residents must navigate.

Community Property Characterization

California is one of nine community property states. Assets acquired during marriage (with certain exceptions) are community property, owned 50/50 by each spouse regardless of whose name is on the title.

Gifting impact: You cannot gift your spouse’s half of community property without their written consent. If you gift $10 million of community property stock without spousal consent, only $5 million (your half) is a completed gift. The other $5 million remains in limbo and could be challenged by your spouse or their creditors.

Documentation requirement: California Family Code Section 1100 requires written consent for gifts of community property. Best practice is to have both spouses sign the Form 709 when gifting community assets, and attach a spousal consent form drafted by a California attorney.

Proposition 19 and Property Tax Reassessment

Proposition 19 (effective February 16, 2021) eliminated the parent-child property tax exclusion for transfers of real estate that isn’t the child’s primary residence. When you gift California real estate to your children, the property will be reassessed to current market value unless the child moves in as their primary residence within one year.

Tax cost example: You gift a $4 million Malibu beach house to your daughter that you purchased in 1985 for $300,000. Your current property tax bill (based on the 1985 value) is approximately $4,200 annually. After reassessment, the new property tax bill will be approximately $44,000 annually (1% of $4 million). If your daughter doesn’t use it as her primary residence, she’ll pay an extra $39,800 per year in property tax.

Planning strategy: Consider keeping California real estate in your estate to preserve the current property tax basis for your children. Use your gift tax exclusion for other assets (stocks, business interests, out-of-state real estate) that don’t trigger California property tax reassessment.

California’s Proposed Billionaire Tax Act

California voters will decide in November 2026 whether to adopt a one-time 5% wealth tax on individuals with net worth exceeding $1 billion who were California residents as of January 1, 2026. While this affects fewer than 200 taxpayers, the political climate signals potential for expanded wealth taxation.

Proactive gifting: If you’re concerned about future California wealth taxes, gifting assets out of your estate in 2026 removes them from your California tax base. Once assets are transferred to an irrevocable trust or to your children, they’re no longer “your” wealth for purposes of any future California net worth tax calculations.

Gift Splitting: How Married Couples Double Their Annual Exclusion

Married couples can elect gift splitting under IRC Section 2513, treating any gift made by either spouse as if each made half the gift. This effectively doubles your annual exclusion from $18,000 to $36,000 per recipient.

How Gift Splitting Works

Your daughter buys her first home, and you want to help with the down payment. You write a check for $70,000 from your separate property account. Without gift splitting, you’ve made a $52,000 taxable gift ($70,000 minus $18,000 annual exclusion) and must file Form 709.

With gift splitting: You and your spouse elect on Form 709 to split the gift. Now each of you is treated as giving $35,000. After each spouse’s $18,000 annual exclusion, you’ve each made a $17,000 taxable gift (total $34,000 combined). You’ve reduced your total taxable gift from $52,000 to $34,000 simply by checking a box.

Requirements for Gift Splitting

Both spouses must be U.S. citizens or residents at the time of the gift. Both must consent to split all gifts made during the calendar year (you can’t pick and choose). Both must sign Form 709 even if only one spouse made the gifts. If you file separate returns, you must attach a statement showing you’ve consented to split gifts.

When Not to Split Gifts

If one spouse has a large estate and the other has a small estate, gift splitting might not be optimal. Splitting uses both spouses’ lifetime exclusions equally. If one spouse is likely to die with unused exclusion, it may be better to have the wealthier spouse make all the gifts, preserving the other spouse’s full $15 million exemption.

Special Situations and Edge Cases

Standard gift tax rules don’t always apply cleanly to complex family situations. Here are scenarios that require special planning.

Gifts to Non-Citizen Spouses

The unlimited marital deduction (IRC Section 2523) doesn’t apply if your spouse is not a U.S. citizen. In 2026, you can only gift $185,000 per year to a non-citizen spouse without using your lifetime exclusion or owing gift tax.

Strategy: Consider a Qualified Domestic Trust (QDOT) if you want to leave assets to a non-citizen spouse without immediate estate tax. The QDOT defers estate tax until distributions are made to the spouse or until the spouse dies.

Gifts to Irrevocable Life Insurance Trusts (ILITs)

Life insurance death benefits are income tax-free but includible in your estate if you own the policy. An ILIT removes the policy from your estate, but premium payments are gifts to the trust beneficiaries.

Crummey powers: To qualify premium payments for the $18,000 annual exclusion, the trust must give beneficiaries a temporary right to withdraw contributions (typically 30 days). You must send formal Crummey notices to beneficiaries each time you make a premium payment, documenting their withdrawal rights. If you skip this step, your premium payments become taxable gifts that use your lifetime exclusion.

Part-Gift, Part-Sale Transactions

Selling an asset to a family member for less than fair market value is a part-gift, part-sale. The IRS treats the below-market portion as a gift. You must recognize capital gain on the sale portion, even though you received less than full value.

Example: You sell $5 million of stock with a $1 million basis to your son for $3 million. The $2 million discount is a gift. You must recognize $2 million in capital gain (($3 million sale price ÷ $5 million FMV) × $4 million total gain). Your son’s basis is $3.8 million (the $3 million he paid plus $800,000 of your basis allocated to the gift portion).

Better approach: Gift the entire $5 million to your son outright or to a trust. He receives a carryover basis of $1 million. If he sells immediately, he’ll owe capital gains tax on $4 million, but you’ve avoided recognizing any gain yourself and can potentially reimburse him for the tax cost from other assets.

Ready to Reduce Your Tax Bill?

KDA Inc. specializes in strategic tax planning for business owners, S Corps, LLCs, and high-net-worth individuals. Book a personalized consultation and walk away with a clear plan.

Frequently Asked Questions

Do I Need to File a Gift Tax Return If I’m Under the $15 Million Lifetime Exclusion?

Yes, if you make any taxable gift exceeding the $18,000 annual exclusion. Even though you owe no gift tax, Form 709 is required to document the gift and start the statute of limitations running. Failure to file means the IRS can audit and revalue the gift decades later.

Can the IRS Reverse Gifts I Made Under the $15 Million Exclusion If It Drops in 2027?

No. IRS Revenue Procedure 2022-32 established an anti-clawback rule. If you make gifts under the current $15 million exclusion and die after it decreases, your estate calculation uses the higher exclusion amount that was in effect when you made the gift.

What Happens If I Use My Entire $15 Million Exclusion During Life?

You’ll have no remaining exclusion to protect your estate at death. Every dollar in your taxable estate will be subject to the 40% federal estate tax. For this reason, most planners recommend leaving some exclusion unused to cover estate growth and unexpected asset accumulation.

How Do I Gift Real Estate Without Triggering Due-on-Sale Clauses?

Most mortgages contain due-on-sale clauses allowing the lender to demand full payment if you transfer the property. Transfers to irrevocable trusts typically don’t trigger this clause if you retain a beneficial interest, but check your loan documents. For income-producing properties, consider gifting LLC interests instead of direct real estate transfers.

Document Checklist: What You Need to Execute Large Gifts

Properly documenting large gifts protects you from IRS challenges and family disputes. Here’s what you need before transferring assets.

Required Documents for All Taxable Gifts

- Form 709 (U.S. Gift Tax Return) filed by April 15 of the following year

- Qualified appraisal for any non-cash assets valued over $10,000 (real estate, business interests, artwork)

- Appraiser credentials showing ASA, ABV, or equivalent designation

- Gift letter or memorandum documenting donor intent and gift completion date

- Transfer documentation (updated deeds, stock certificates, LLC membership certificates)

Additional Documents for California Residents

- Spousal consent form if gifting community property (California Family Code Section 1100)

- Separate property transmutation agreement if converting community property to separate property before gifting

- Preliminary change of ownership report (Form BOE-502-A) filed with county assessor within 45 days of real estate transfer

- Proposition 19 analysis documenting property tax reassessment impact

Trust-Specific Documents

- Irrevocable trust agreement signed and notarized before transfers

- EIN application confirmation (Form SS-4) for the trust

- Crummey withdrawal notices if using annual exclusion for trust gifts

- Trust funding memorandum listing all assets transferred and valuation dates

What Happens If You Miss the December 31, 2025 Deadline?

If Congress doesn’t extend the current exemption and you miss the deadline, your planning options narrow but don’t disappear.

Post-Sunset Strategies

Even with a reduced $7 million exemption starting in 2027, you can still execute meaningful wealth transfers. Focus on maximizing valuation discounts, using annual exclusion gifts, and leveraging the grantor trust rules.

Annual exclusion gifts: $18,000 per recipient per year never uses your lifetime exclusion. A couple with four children and eight grandchildren can still transfer $432,000 per year ($18,000 × 12 recipients × 2 spouses) completely tax-free forever.

Valuation discounts: A $10 million business transferred directly uses $10 million of exclusion. The same $10 million business restructured as minority interests in a family limited partnership might have a discounted gift value of $6.5 million after lack of control and lack of marketability discounts. You’ve moved $10 million of value using only $6.5 million of exclusion.

Installment sales to grantor trusts: Sell appreciating assets to an intentionally defective grantor trust (IDGT) in exchange for a promissory note. The sale freezes the value in your estate at the note amount while all future appreciation occurs in the trust, estate-tax-free. You must “seed” the trust with at least 10% of the sale price as a gift, but the remaining 90% moves without using additional exclusion.

When to Use Your Exclusion vs. Other Strategies

Using your $15 million lifetime exclusion isn’t always optimal. Sometimes other techniques accomplish the same goal without burning irreplaceable exemption.

Use Your Exclusion When:

- Assets are highly appreciating (growth stocks, startup equity, development real estate) and you want to lock in today’s value

- You have more than $15 million in assets and will owe estate tax regardless

- You’re in poor health and may not survive the term of a GRAT or other time-limited strategy

- The exclusion is sunsetting soon (as it is on December 31, 2025) and you risk losing transfer capacity

Consider Alternatives When:

- Assets are income-producing but low-growth (bonds, mature rental properties, utility stocks) – keep these for living expenses

- You’re unsure about future liquidity needs – once gifted, you can’t get assets back

- You qualify for valuation discounts (family business, real estate partnerships) that let you move more value per exclusion dollar

- Your estate is under $7 million and you’ll likely remain below the exclusion even after it drops

State Estate Tax Trap: Not All States Follow Federal Rules

While California has no state estate tax, twelve states plus D.C. impose their own estate taxes with exemptions far below the $15 million federal level. If you own property or have business interests in multiple states, you face complex planning issues.

States With Estate Tax (2026)

Connecticut, Hawaii, Illinois, Maine, Maryland, Massachusetts, Minnesota, New York, Oregon, Rhode Island, Vermont, and Washington all impose estate tax. Exemptions range from $1 million (Oregon) to $13.61 million (Connecticut).

Massachusetts is particularly aggressive, taxing estates over $2 million at rates up to 16%. A Massachusetts resident with a $10 million estate owes $815,000 in Massachusetts estate tax even though no federal estate tax is due.

California Residents With Multi-State Property

If you’re a California resident but own a vacation home in Oregon or rental property in Washington, your estate may owe estate tax to those states based on the proportional value of property located there.

Example: You’re a California resident with a $20 million estate, including a $3 million Oregon vacation home. Oregon will impose estate tax on the $3 million home (approximately $300,000 after Oregon’s $1 million exemption). Your California residency doesn’t protect you from Oregon estate tax on Oregon-situs property.

Planning solution: Transfer out-of-state real estate to an LLC, then gift LLC interests to an irrevocable trust. The LLC removes the real estate from your personal ownership, potentially avoiding state estate tax. Consult with tax counsel licensed in both California and the property’s state before implementing this strategy.

How KDA Helps High-Net-Worth Clients Maximize the 2026 Exclusion

The federal gift tax exclusion is powerful but complex. Most taxpayers need coordinated planning across gift tax, income tax, estate planning, and California property law to maximize the benefit without triggering unintended consequences.

KDA’s approach combines tax strategy with legal execution. We don’t just calculate numbers – we implement complete gifting plans with proper appraisals, trust documents, family LLC restructuring, and IRS reporting. Our clients receive actionable roadmaps, not theoretical advice.

If you’re sitting on appreciated assets, worried about the 2026 sunset, or facing California’s evolving wealth tax environment, you need a strategy before December 31. Explore our comprehensive tax planning services to see how we help high-net-worth individuals protect wealth across generations.

Book Your Estate Planning Strategy Session

The $15 million federal gift tax exclusion creates a limited-time opportunity to move wealth out of your taxable estate before the exemption drops in 2027. Whether you’re planning for California’s proposed wealth tax, managing multi-state property, or simply want to reduce your future estate tax bill, the time to act is now.

Don’t let the December 31, 2025 deadline pass without a plan. Book a personalized consultation with KDA’s estate planning team and get a clear roadmap for maximizing your 2026 exclusion. Click here to schedule your strategy session today.

This information is current as of May 29, 2026. Tax laws change frequently. Verify updates with the IRS or a qualified tax professional if reading this later.