Many C corporation owners know they are probably overpaying the IRS but have been warned that switching to an S corporation is “complicated” or “risky.” That hesitation is expensive. Get the timing wrong and you can trigger extra tax on built in gains, lose access to valuable deductions, or miss out on five figures of annual savings.

The quick reality check is this: the tax code gives you several windows where converting from C status to an S election is not only safe, it is often one of the highest ROI moves a closely held company can make. The real question is not whether you should convert, but when to convert c corp to a s corp based on your profits, exit plans, and shareholder mix.

Quick Answer: When Does Converting Make Tax Sense

For a profitable, closely held operating company, the sweet spot to elect S status is usually when:

- Annual net taxable profit (before owner wages) is at least 80,000 to 100,000 dollars

- You expect to keep distributing most of those profits to owners rather than stockpiling cash

- You do not plan to sell appreciated assets in the next five years

- All shareholders are US individuals or certain qualifying trusts

At that point, shifting to an S corporation can often cut shareholder level tax on profits by 8,000 to 30,000 dollars per year, mainly by avoiding double taxation on distributions and reducing exposure to the 3.8 percent net investment income tax. The mechanics sit in Subchapter S of the Internal Revenue Code, but the decision itself should be framed in plain language: do you want profits taxed once or twice, and how soon might you sell?

This information is current as of 5/19/2026. Tax laws change frequently. Verify details with the IRS or your state tax agency if you are reading this later.

How C Corporation Tax Really Works In Practice

Before you can decide on timing, you need a clear view of how your C corporation is being taxed right now. Under Internal Revenue Code section 11, your corporation pays federal corporate income tax on its taxable income. For 2024 and 2025, that is a flat 21 percent federal rate, plus any applicable state corporate income or franchise tax.

Then, when you pay dividends from after tax profits to shareholders, those individuals pay a second layer of tax, often at 15 or 20 percent for qualified dividends plus the 3.8 percent net investment income tax if they are high earners. See the IRS instructions for Form 1120 and IRS Publication 542 for the official framework.

A Simple Double Tax Example

Assume your C corporation has 200,000 dollars of pre tax profit in 2025. You are in California.

- Federal corporate tax at 21 percent: 42,000 dollars

- California corporate tax at 8.84 percent: about 17,680 dollars

- After tax profit left in the company: roughly 140,320 dollars

If you distribute the full amount as a dividend to yourself as a shareholder, and your federal qualified dividend rate is 15 percent, with no net investment income tax for simplicity, that is another 21,048 dollars of federal tax. Add California tax on the dividend and your combined burden on that same 200,000 dollars of profit can easily exceed 40 percent.

This structure still works for certain businesses, especially if you are reinvesting aggressively or preparing for a sale to a buyer who prefers C stock. But if you are essentially running a closely held consulting firm, medical practice, engineering company, or e commerce business and pulling most profits out each year, that double tax is dead weight.

How The S Corporation Alternative Taxes Profits

An S corporation is a pass through entity. The company generally does not pay federal income tax at the entity level. Instead, shareholders receive a Schedule K 1 reporting their share of the company’s income, which they include on their individual Form 1040. See IRS Publication 589 and Form 1120 S instructions for the baseline rules.

The critical difference is that there is no second layer of tax when you distribute cash. If your S corporation has 200,000 dollars of profit and there are no built in gains issues, that 200,000 shows up once on your personal return. You may still owe the 3.8 percent net investment income tax depending on facts, but you are not stacking entity tax and shareholder tax on top of each other.

Income Levels Where Conversion Starts To Pay Off

The most common timing question is not just technical, it is practical. You want to know when your profit level justifies the paperwork, payroll setup, and potential built in gains exposure of an S election.

Break Even Range For Small Owners

For many closely held businesses, the math starts to shift in your favor when pre owner wage profit consistently exceeds 80,000 to 100,000 dollars per year. Here is a simplified scenario for a single owner business that is currently a C corporation and considering when to convert c corp to a s corp.

- Company profit before owner wage: 180,000 dollars

- Reasonable owner salary as an employee: 90,000 dollars

- Remaining business profit: 90,000 dollars

Under C rules, the 90,000 of remaining profit is taxed inside the corporation. Then distributions later are taxed again. Under S rules, the 90,000 of remaining profit is generally passed through to you and taxed once on your personal return. Depending on your bracket and state, that structural shift alone can often reduce combined annual tax by 8,000 to 15,000 dollars or more.

If you are a business owner in this income range and primarily use your company to pay your own household, it is worth reviewing your situation with a team that understands both entity elections and ongoing compliance. Our tax planning services are built to do this analysis in plain English before you touch any IRS forms.

Higher Profits And High Net Worth Shareholders

Once annual pre wage profit crosses 300,000 dollars, the opportunity cost of staying C status can become severe, especially for high net worth owners whose personal tax rates are already elevated. Not only are you dealing with double taxation, but C level profits can also push more income into the net investment income tax regime.

For an owner couple filing jointly with 600,000 dollars of combined income and a C corporation throwing off 400,000 dollars of pre tax profit, the difference between leaving that profit inside the C structure and flowing it through an optimized S election with appropriate wages can cross into six figure annual savings. That is a level where you should rarely be making decisions without sophisticated modeling.

If you want to run your own high level estimate before you talk to anyone, plug your projected business profit into this small business tax calculator and compare scenarios with and without an S style pass through.

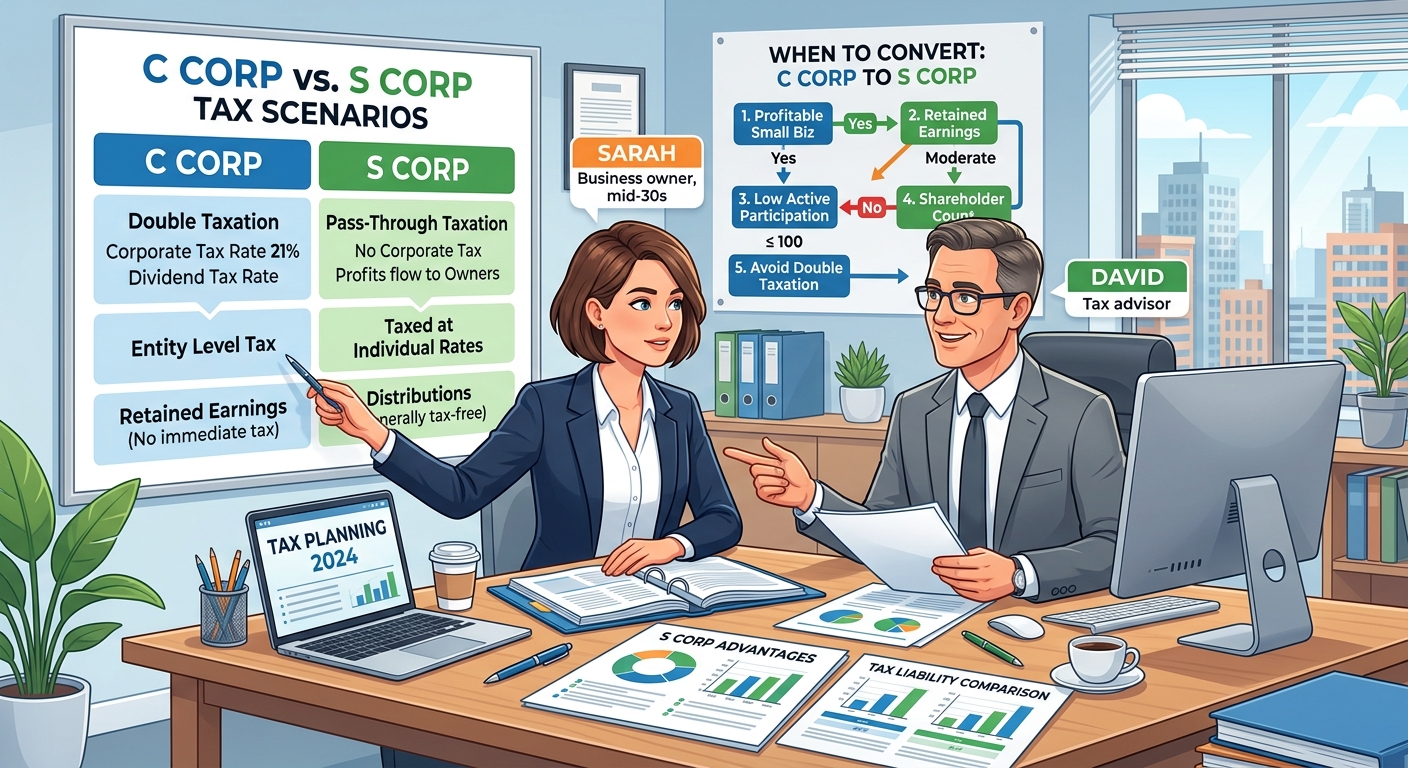

Technical Triggers: Built In Gains, Shareholder Rules, And Deadlines

Tax savings alone is not enough. The timing of your election has to respect several technical rules in the Internal Revenue Code, or you can accidentally create new tax bills.

Watching The Built In Gains Clock

When a C corporation converts to S status, the IRS wants to make sure you do not dodge corporate level tax on appreciation that built up while you were a C corporation. So it created the built in gains tax in section 1374. In very simple terms, for a fixed recognition period after the conversion, if the S corporation sells appreciated assets that existed on the date of the election, the company may owe a corporate level tax on that built in gain.

Congress has adjusted the length of that recognition period several times. For planning purposes, many advisors still work with a conservative five year mindset. You will want to confirm the current recognition period and any special relief in effect for the year of your conversion by reviewing the instructions for Form 1120 S and IRS Publication 542.

The practical takeaway is this. If you plan to sell a building, a large block of appreciated stock, or a business segment in the next few years, that might be a reason to delay your S election or adjust the transaction structure. On the other hand, if your company’s value is largely in current year service revenue and equipment that is already fully depreciated, built in gains risk may be minimal.

Shareholder Eligibility And The 100 Shareholder Cap

To qualify for S status, your corporation must meet several strict shareholder rules laid out in Internal Revenue Code section 1361.

- No more than 100 shareholders

- Only one class of stock, with equal rights to distributions and liquidation proceeds

- Only eligible shareholders, generally US individuals, certain estates, and specific types of trusts, no partnerships or corporations as owners

If your C corporation already has multiple classes of preferred stock, foreign shareholders, or entity owners, you may need to redesign your cap table before filing Form 2553. This is where high income entrepreneurs, real estate syndicators, and investor backed e commerce sellers often need careful entity work to avoid a blown election.

For owners in those categories, reviewing the structure with a team that regularly supports business owners with complex capitalization tables is essential before you send anything to the IRS or the California Franchise Tax Board.

Election Timing, Late Relief, And State Rules

Federal S elections are made on Form 2553. To be effective as of the start of a tax year, the general rule is that you must file within two months and 15 days after the beginning of that year. The IRS does provide late election relief in some circumstances. See the Form 2553 instructions and associated revenue procedures for details.

States have their own timing and conformity rules. California, for example, generally respects the federal election for tax purposes but still imposes an annual 1.5 percent tax on S corporation net income and minimum franchise taxes. You will typically need to update your status with the Franchise Tax Board either directly or through your return on Form 100 S.

Reasonable Salary: The Often Misunderstood Lever

When you explore when to convert c corp to a s corp, you will quickly run into the concept of reasonable compensation. The IRS expects S corporation owner operators who perform services to receive a fair W 2 wage. That wage is subject to payroll taxes, just like any other employee.

Why does this matter so much? Because once a C corporation becomes an S corporation, your tax profile changes:

- Your W 2 salary from the S corporation remains subject to Social Security and Medicare taxes

- Your share of remaining S corporation profit is generally not subject to self employment tax under current rules

- The IRS uses the reasonable salary requirement to prevent owners from calling all income “distributions” to dodge payroll tax

Calibrating Salary To Your Industry

The right salary number depends on your role, industry norms, and company performance. The IRS references multiple sources, including market wage data and your own corporate history, when challenging salaries in audits. While there is no simple formula in the Code, cases and IRS Publication 15 provide a roadmap.

For example, if you run a consulting firm with 300,000 dollars of net income and provide nearly all billable work, paying yourself a 40,000 dollar salary with 260,000 dollars of distributions is asking for scrutiny. A more defensible structure might be a 140,000 to 170,000 dollar salary with the remainder as profit distributions, backed by comparable W 2 wage data for similar roles.

Done properly, tuning reasonable salary after conversion can preserve tens of thousands of dollars in payroll taxes over a decade while still passing an IRS smell test.

KDA Case Study: LLC Owner Uses C To S Timing To Unlock Savings

Consider Maria, a California based software consultant. She originally formed an LLC that elected to be taxed as a C corporation on the advice of a prior accountant who focused on corporate benefits. Within three years, the company was generating 260,000 to 320,000 dollars of pre tax profit, and Maria was taking most of it out as dividends after a modest W 2 wage.

Her effective combined tax rate on distributed profits was creeping above 40 percent once corporate tax, shareholder level tax, and net investment income tax were stacked together. She also planned to keep operating the business for at least another seven to ten years, with no plans to sell major appreciated assets. That combination made her a strong candidate for S status.

Our team built a side by side projection comparing five more years of C status with an S election effective January 1 of the next year. We set a reasonable salary of 150,000 dollars based on market data and left the remaining profit to flow through as S corporation income.

The results were straightforward. Even after accounting for California’s 1.5 percent S corporation tax and slightly higher Medicare tax on wages, the switch produced projected federal and state tax savings of roughly 24,000 dollars per year at her current profit level. Over a conservative five year horizon, that was 120,000 dollars of projected savings against a one time planning and implementation fee of under 7,000 dollars, a first year ROI north of 3x.

Ready to see how we can help you? Explore more success stories on our case studies page to discover proven strategies that have saved our clients thousands in taxes.

Red Flag Alert: Situations Where You Should Wait

There are also clear scenarios where rushing into an S election can backfire, even if your profit is growing.

Imminent Asset Sales Or Major Appreciation

If your C corporation holds real estate, valuable intellectual property, or a business line you intend to sell in the next few years, switching to S status too close to the sale can trigger built in gains tax. In that situation, the timing of when to convert c corp to a s corp becomes a blend of tax cost modeling and deal strategy.

Sometimes it is better to close the sale under C rules and then restructure for future operations. Other times, if the primary value is in current cash flow rather than appreciation, you may still move forward with an S election but adjust how you handle specific assets. This is exactly the kind of nuance that generalist preparers tend to miss.

Investor Backed Or Multi Class Capital Structures

Venture backed startups and real estate syndications often use preferred stock, convertible instruments, and entity shareholders, which are generally incompatible with S status. Forcing a conversion without realigning the capitalization table can cause the election to fail, pushing you back into C territory automatically.

That does not mean you can never use S status in those environments, but it typically requires parallel entities, holding structures, or careful transition plans.

Low Or Volatile Profit Profiles

If your business is consistently under 60,000 dollars of pre owner wage profit, or profitability is highly volatile year to year, the compliance cost and payroll complexity of S status may not be justified yet. In some cases, waiting until your numbers stabilize is the smarter move.

What The IRS Will Look At If You Change

Any time you change how an active business is taxed, you should assume that the IRS and state agencies may compare your before and after filings. They are mainly looking for three things.

Consistency Of Reported Income

If your company showed 400,000 dollars of gross receipts as a C corporation one year and then magically drops to 250,000 dollars in the first S year with no clear business reason, you are inviting questions. Keep your books clean, reconcile gross receipts to 1099s and bank deposits, and be ready to explain any major fluctuations.

Reasonableness Of Officer Compensation

As mentioned earlier, officer wages in the S years need to match your actual role and industry norms. The IRS can and does reclassify distributions as wages in audits, which can create back payroll tax assessments plus penalties. See IRS Publication 15 for baseline employment tax rules.

Proper Use Of Forms And Elections

Make sure your Form 2553, subsequent Form 1120 S filings, and state level submissions all line up. Late or inconsistent filings are one of the fastest ways to lose the benefit of a good strategy.

How To Decide Your Conversion Year Step By Step

Here is a structured way to approach the decision.

Step 1: Model The Next Three To Five Years

Start by projecting your company’s income statement under two scenarios, staying C and converting to S as of January 1 of a future year. Include salary assumptions, expected distributions, and planned asset sales. The goal is not perfection, but clarity on order of magnitude savings.

Step 2: Map Built In Gains And Exit Plans

List out any appreciated assets, such as real estate, major equipment, or intangible assets with real market value. For each, estimate when you might sell. If you see likely transactions inside the next recognition window, note the potential built in gains exposure.

Step 3: Check Eligibility And Clean Up The Cap Table

Review your shareholder list for ineligible owners, multiple stock classes, or complex instruments. If you have foreign shareholders, partnership owners, or preferred stock, map what it would take to transition to a single class of qualifying owners, or decide whether S status is realistically off the table.

Step 4: Align With State Requirements

Confirm how your home state and any major operating states treat S corporations. In California, that means planning for the 1.5 percent S corporation tax and minimum franchise fees, and making sure you follow Franchise Tax Board procedures so that your state treatment aligns with the federal election.

Step 5: Execute The Election And Payroll Changes

Once you lock in your target effective year, you will need to:

- Prepare and file Form 2553 with the IRS, including required shareholder consents

- Adjust your payroll system for new reasonable salary targets and withholding

- Update your bookkeeping so that retained earnings and distributions are tracked correctly

- Coordinate with your tax team on first year Form 1120 S and state returns

At each stage, keep in mind the core question that started this analysis, which is not just whether S status is good in the abstract, but specifically when to convert c corp to a s corp for your income curve, asset base, and exit timeline.

Ready to Reduce Your Tax Bill?

KDA Inc. specializes in strategic tax planning for business owners, S Corps, LLCs, and high-net-worth individuals. Book a personalized consultation and walk away with a clear plan.

Frequently Asked Questions On C To S Conversions

Will converting to an S corporation trigger an audit

There is no automatic audit trigger tied solely to filing Form 2553. However, substantial changes in reported income, officer compensation, or deductions around the same period can draw attention. Staying consistent and well documented is your best protection.

Can I reverse the decision if I do not like it

You can revoke an S election and return to C status, but the Code limits how often you can move back and forth. Generally, if you voluntarily terminate S status, you are barred from re electing for five years unless you obtain IRS consent. So treat the choice as a medium term commitment and plan accordingly.

What if my company has net operating losses as a C corporation

Existing C corporation net operating losses generally remain with the C corporation and cannot be used to offset S corporation income after the election. That is another reason to consider timing carefully. In some cases, it makes sense to use up NOLs under C rules before converting.

Is there any benefit to waiting until my company is bigger

Yes, in some situations. If your profit is currently modest and you expect large growth in a few years, modeling a delayed election can reveal a better answer. Sometimes you accept a bit of double tax now to avoid built in gains complications later, then convert once your structure and plans are clearer.

Book Your Tax Strategy Session

Choosing the right year and structure for your S election is not a forms question, it is a strategy decision that can move tens of thousands of dollars between your family and the IRS over the next decade. If you are wrestling with when to convert c corp to a s corp for your company, do not guess based on generic rules of thumb.

Our team at KDA works with business owners, high earning professionals, and real estate entrepreneurs across California and beyond to build conversion plans that respect both IRS rules and real world cash flow. If you want a clear, customized recommendation backed by actual numbers, book a one on one strategy session. Click here to book your consultation now.

The IRS is not hiding these elections from you, but it will not tell you the optimal year to make your move. That part is on your strategy.