Most business owners know S corporations and C corporations are taxed differently, but when they try to visualize the gap, they are stuck with vague articles and no numbers. If you cannot see how the tax flows through each structure, you cannot make a smart entity decision, especially once your profit crosses six figures.

In this guide, we will do what other articles skip. We will walk through the difference between c and s corp graph style comparison using plain English, real dollar amounts, and a simple framework you can sketch on a napkin. You will see exactly how money moves from your business to your pocket under each structure and where the IRS takes its cut.

Quick Answer

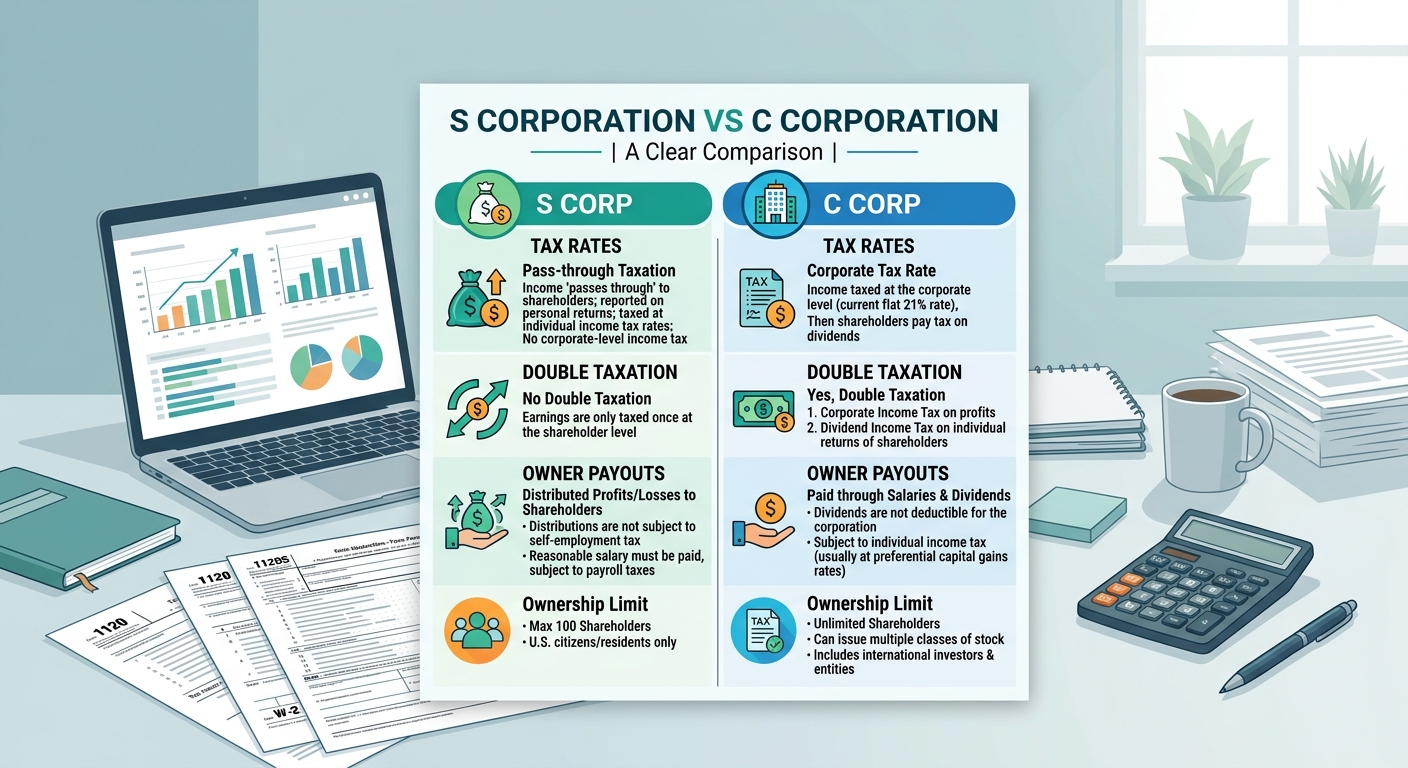

The core difference between a C corporation and an S corporation is how profit is taxed and how many layers of tax you face. A C corporation pays corporate income tax on its profits, then shareholders pay tax again on dividends. An S corporation generally does not pay federal income tax at the entity level. Instead, profit flows through to the owners personal returns, often allowing part of that income to avoid self employment tax if you pay yourself a reasonable salary. The right choice depends on your profit level, how you plan to pull cash out, and whether you expect to sell the company.

How Money Flows in a Corporation

Before we overlay an S corporation vs C corporation graph in your mind, you need to understand the money paths inside a corporation. There are only three ways cash gets out of a corporation to you as the owner.

- Salary and bonuses as a W 2 employee

- Distributions or dividends as an owner

- Sale proceeds when you sell stock or assets

Each path has its own tax treatment. The IRS explains the basics for corporations in IRS Publication 542 and for business expenses in IRS Publication 535, but those documents are not written for busy founders.

Here is the mental model you should use.

- The business earns profit before owner pay.

- Some of that profit becomes payroll to you and your team.

- What is left is either taxed inside the C corporation or flows through if you are an S corporation.

- Finally, whatever is left after taxes lands in your personal checking account.

If you draw that as a flow chart, the S corporation and C corporation look similar at the top but very different at the bottom where taxes hit.

Building a Simple Difference Between C and S Corp Graph in Your Head

Instead of staring at dense tables, imagine a horizontal bar that represents 100 percent of your business profit before owner pay. We will split that bar into slices to compare structures. This is the practical way to think about the difference between C and S corp graph style without fancy software.

Step 1: Start with $200,000 of Profit

Assume your LLC generates $200,000 of profit before paying you. You are the only owner and you are considering electing S corporation status or converting to a C corporation. You live in California, but we will focus on federal rules first to keep the picture clean.

Visually, your bar is $200,000 wide. Now we decide how much becomes salary and how much stays as profit.

Step 2: Choose a Reasonable Salary for an S Corporation

The IRS expects S corporation owners who work in the business to take a reasonable salary for the work they perform. Reasonable means what you would pay someone else to do your job. For a consultant with $200,000 of profit, a $100,000 salary is often defendable, assuming your market supports that rate. The IRS discusses reasonable compensation concepts in various guidance on S corporation compensation.

For the S corporation bar, we now have two segments.

- $100,000 salary segment

- $100,000 S corporation profit segment

Salary is subject to payroll taxes and income tax. The S corporation profit still gets taxed as income on your personal return, but it is not subject to self employment tax. That is where much of the savings often comes from.

Step 3: C Corporation Treatment of the Same $200,000

For a C corporation, you could also pay yourself a $100,000 salary and leave $100,000 of profit inside the company. In 2026, C corporations face a flat federal income tax rate of 21 percent under current law. So the corporation pays $21,000 of tax on the $100,000 profit, leaving $79,000 in after tax retained earnings.

If the corporation then distributes that $79,000 to you as a qualified dividend, you pay federal tax again at the dividend rate, which could range from 0 percent to 20 percent plus the 3.8 percent net investment income tax, depending on your total income. If you are in the 15 percent capital gains bracket, the second layer of tax is about $11,850, leaving roughly $67,150 in your pocket from that $79,000 distribution.

On a difference between C and S corp graph, the S corporation shows one layer of tax on the $100,000 profit at your individual rate. The C corporation shows two layers on that same segment.

Numerical Comparison of S Corporation and C Corporation at $200,000 Profit

Let us rough out the numbers so the picture is anchored in dollars. We will ignore state tax and certain smaller items to keep the illustration simple and focus on federal effects for the 2025 tax year.

S Corporation Scenario

- Profit before owner pay: $200,000

- Owner salary: $100,000

- Remaining S corporation profit: $100,000

Payroll taxes on the $100,000 salary are about 15.3 percent on the first $160,200 or so of wages for Social Security and Medicare combined, but half of that is the employer share and half is the employee share. Roughly $15,300 in payroll taxes are paid, though part is deductible to the business. On your individual return, you report $200,000 of income, but only $100,000 was subject to self employment style taxes.

If your blended federal income tax rate on that $200,000 is 22 percent, your income tax bill is about $44,000. Combined with $15,300 of payroll taxes, your total federal burden is roughly $59,300. Net after federal tax is around $140,700.

C Corporation Scenario

- Profit before owner pay: $200,000

- Owner salary: $100,000 (same assumption)

- Corporate profit: $100,000

The corporation pays 21 percent corporate tax, or $21,000, leaving $79,000. The $100,000 salary generates the same payroll tax load as the S corporation example.

If the corporation distributes all $79,000 as qualified dividends and you are in the 15 percent dividend bracket, you pay about $11,850 of federal tax on the dividend. So your total tax burden is $21,000 at the corporate level plus $11,850 on dividends plus the same $44,000 of income tax and $15,300 of payroll tax on your salary income. That stack adds up to about $92,150.

Your net after federal tax from both salary and dividends is around $107,850.

On a visual difference between C and S corp graph, the C corporation bar would show a noticeably larger red section for taxes. At these income levels, the S corporation structure delivers roughly $32,850 more after federal tax in this simplified example.

Where a C Corporation Can Still Win

There are cases where the C corporation comes out ahead, and your mental graph needs room for those, especially for high growth companies or those planning a sale.

Retained Earnings Strategy

If you do not need to pull all the profit out each year, a C corporation can keep money inside at the 21 percent rate, which may be lower than your personal bracket. Suppose your business earns $500,000 and you only need $200,000 personally.

- In an S corporation, all $500,000 flows through and is taxed at your personal rates, even if you leave some cash in the business bank account.

- In a C corporation, only the $200,000 of salary hits your personal return. The remaining $300,000 is taxed at 21 percent inside the corporation. If your marginal personal rate is 35 percent, that is a meaningful deferral.

The tradeoff is that if you later distribute those retained earnings as dividends, you face the second layer of tax. But if you reinvest the cash into growth, equipment, or an eventual sale, the math can tilt toward the C corporation. Long term planning around this involves capital gains rules and, for some businesses, potential exclusions under Section 1202 qualified small business stock.

Sale of the Business

When you sell, entity choice affects how the proceeds are taxed. Many small business sales are structured as asset sales for tax and legal reasons. For an S corporation, gain on the asset sale flows through to your return; parts may be taxed at long term capital gains rates, others at ordinary rates depending on asset type.

With a C corporation, an asset sale creates tax inside the corporation on the gain, then another layer of tax when the after tax proceeds are distributed to you. In contrast, if you can sell C corporation stock directly and meet the requirements for Section 1202, you might exclude a large portion of the gain from federal tax. That is an advanced planning area that requires careful modeling.

Red Flag Alert: Common Entity Mistakes Owners Make

Many owners focus only on the current year tax bill and ignore how flexible or painful the structure becomes as the business scales. Some of the most expensive mistakes we see include the following.

- Staying a sole proprietor with $150,000 plus of profit and paying self employment tax on every dollar, because no one explained the S corporation option.

- Electing S corporation status at very low profit levels where the added payroll and compliance costs outweigh any savings.

- Forming a C corporation chasing investor optics even though there is no realistic plan for a stock sale or Section 1202 benefit.

- Ignoring reasonable compensation rules in an S corporation and taking almost everything as distributions, which raises audit risk.

According to IRS Publication 334, self employed individuals face both income tax and self employment tax on net earnings. That double layer on every dollar is why entity planning matters.

For many business owners, the smartest move is to model two or three years ahead instead of making a decision based solely on this April.

KDA Case Study: Consultant Rebuilds Their Entity Strategy

Consider Maria, a 1099 marketing consultant in California who started as a sole proprietor. In 2023, she earned $180,000 of net income and filed on Schedule C. Between income tax and self employment tax, her combined federal liability was just over $55,000. She felt the pain but assumed that was simply what high earners pay.

In 2024, Maria engaged KDA to review her structure. After running the numbers, our team recommended forming an LLC and electing S corporation status for 2025. We set her on a $90,000 W 2 salary, consistent with market pay for a senior consultant in her niche, and allowed the remaining profit to pass through as S corporation income.

We also cleaned up her bookkeeping, shifted certain recurring expenses into accountable plans, and improved her retirement contributions. When we compared her prior year tax picture to the first full year using the new structure, Maria saved just under $12,000 in federal self employment and income taxes, even after factoring in payroll costs and KDA advisory fees of about $3,500. That is a first year return of more than 3 times her investment in planning.

More important for Maria, she now had a concrete framework for revisiting her salary as profit grows, including visual S corporation vs C corporation comparisons each time she considers adding partners or investors. She stopped guessing and started operating from numbers.

Ready to see how we can help you? Explore more success stories on our case studies page to discover proven strategies that have saved our clients thousands in taxes.

How To Sketch Your Own S Corporation vs C Corporation Comparison

You do not need software to compare structures. A pen, paper, and a bit of discipline will get you 80 percent of the way there so you can have a strategic conversation with your advisor.

Step 1: Estimate Next Year Profit Before Owner Pay

List your expected revenue and expenses for the next tax year and estimate your net profit before you pay yourself. If your numbers are volatile, sketch a conservative, realistic, and aggressive scenario so you can see how sensitive your choice is to profit swings.

Step 2: Choose a Reasonable Salary Range

Based on your role, market pay, and hours worked, define a reasonable salary band. For example, a solo software developer might pick $120,000 to $160,000. Document why that range is reasonable so that if the IRS ever asks, you have support.

Step 3: Draw Two Bars

Draw two horizontal bars for each scenario.

- Bar A: S corporation

- Bar B: C corporation

Slice each bar into segments for salary, profit, corporate tax, payroll tax, and owner level tax. Even a rough drawing will show you where the red (tax) slices grow or shrink.

Step 4: Run the Numbers with a Calculator

Once you have the picture, plug in real percentages. For many 1099 earners and small LLC owners, it is also useful to understand your current effective tax rate before changing anything. You can use KDA’s online small business tax calculator for a quick estimate of how much tax your current structure generates at different profit levels.

Strategic decisions come from comparing the current state to two or three modeled futures, not from guessing based on something you heard in a founder forum.

What If Your Profit is Under $80,000?

For lower profit businesses, the S corporation vs C corporation difference on a graph is much thinner. Once you account for payroll service fees, extra tax filings, and advisory costs, you might be better off staying a sole proprietor or simple LLC until your profit crosses a certain threshold.

As a rough guideline, if your consistent annual profit before owner pay is under $60,000 to $80,000, the tax savings from an S corporation often do not justify the extra complexity. That is not a hard rule; it depends on your state and whether you can also unlock other strategies like retirement plans. But it should be a signal to run a careful calculation rather than jumping straight into an entity change.

Will This Trigger an Audit?

Any time you change entity type or start splitting income between salary and distributions, owners worry about audit risk, especially around reasonable compensation. The IRS has explicitly stated in multiple reports that underpaid S corporation wages are an enforcement focus. That does not mean every S corporation will be audited, but if your salary is obviously low for your role and profit level, you are planting a flag.

Key ways to avoid unnecessary risk include the following.

- Document comparable salaries using job listings, industry surveys, or compensation reports.

- Avoid paying yourself rock bottom wages while taking six figure distributions.

- Review your salary annually as profit grows rather than leaving it static for years.

According to public IRS enforcement summaries, S corporation reasonable compensation cases often hinge on whether there is any support at all for the wage number and whether the owner can clearly explain their role. Good records and thoughtful modeling go a long way toward making your entity work for you without becoming a red flag.

How Entity Choice Interacts with Other Strategies

Entity choice does not exist in a vacuum. Your S corporation vs C corporation graph should sit alongside other planning tools, especially once you cross the six figure profit mark.

- Retirement plans like solo 401k or SEP IRAs are funded differently depending on whether you pay yourself wages or receive only pass through income.

- Health insurance deductions may run through the corporation differently for S corporation owner employees.

- Real estate strategies, including whether to hold property personally, in an LLC, or under a corporation, can shift your optimal structure.

If you own rental property or invest in syndications, coordinate your entity decision with a tax team that understands real estate investors so you are not solving one problem and creating another.

When modeling these layers, specialists often reference rules from documents like IRS Publication 541 for partnerships and Publication 560 for retirement plans. You do not need to memorize them, but your advisor should understand how they interact with entity choice.

What the IRS Will Not Tell You About Entity Elections

The IRS provides instructions on how to file Form 2553 to elect S corporation status and explains the tax rules for C corporations, but it does not tell you when you should switch. That is a planning decision, not a compliance rule.

For example, California charges an annual 1.5 percent tax on S corporation net income and has a separate franchise tax structure for LLCs and corporations. This means the clean federal comparison you see in most articles is only half the story. Once you add state level minimum taxes and fees, the break even point for an S corporation vs a simple LLC or C corporation shifts.

A good strategy engagement will overlay federal and state taxes, payroll costs, and your long term goals on the same graph. It will also factor in timing rules for elections. Missing the S corporation election deadline can lock you into another year of higher self employment tax, but in some cases late election relief is available if you meet IRS criteria.

When You Should Not Elect S Corporation Status

Despite the marketing hype, S corporations are not a magic switch for every small business. You should be cautious about electing S status if any of these apply.

- Your business regularly generates losses, and you rely on those losses to offset other income such as W 2 wages or rental income.

- You plan to bring in many types of investors who want preferred stock, which S corporation rules do not allow.

- You expect to keep most profits inside the company for many years rather than distribute them.

Sometimes the cleanest solution is to stay a default LLC taxed as a partnership or disregarded entity until your profit stabilizes and your capital structure is clearer. You can then revisit the S corporation versus C corporation decision with better data and a proper model.

How Professional Help Changes the Graph

Most do it yourself comparisons leave money on the table because they only consider federal income tax and a narrow slice of your situation. When we work with clients, we combine entity modeling with bookkeeping, payroll setup, and ongoing tax planning so that the S corporation or C corporation choice is just one piece of a broader system.

Our tax planning services integrate entity selection with reasonable compensation analysis, retirement plan design, and multi year projections. For clients with existing structures, we often rebuild their difference between C and S corp graph using actual historical numbers so they can see, in dollars, what a different choice would have produced over the last three years.

If you are still at the setup stage or considering a change, aligning your entity decision with professional bookkeeping and payroll through KDA can save you both taxes and the stress of fixing mistakes later. You can see an overview of how these solutions fit together in our general services page.

Bottom Line

Deciding between an S corporation and a C corporation is not about picking a trendy label; it is about controlling where and when your profit is taxed. A simple bar style comparison that shows salary, profit, corporate tax, and personal tax for both structures at your actual profit level is far more powerful than any generic rule of thumb.

This information is current as of 5/15/2026. Tax laws change frequently. Verify updates with the IRS or FTB if you are reading this in a later year.

Ready to Reduce Your Tax Bill?

KDA Inc. specializes in strategic tax planning for business owners, S Corps, LLCs, and high-net-worth individuals. Book a personalized consultation and walk away with a clear plan.

Book Your Tax Strategy Session

If you are unsure whether your current entity choice is quietly costing you five figures in unnecessary tax, it is time to see your numbers in a clear side by side comparison. Book a personalized consultation with our strategy team and get a custom S corporation versus C corporation model based on your real income, goals, and state rules. Click here to book your consultation now.

The IRS is not hiding these strategies; most owners simply have never seen their tax picture graphed clearly.