Most Nevada business owners assume that simply forming a corporation in a state with no corporate income tax means their tax problem is solved. That belief quietly costs some of them five figures every year because they pick the wrong corporate structure and do not find out until the IRS bill lands.

The core decision for a Nevada corporation is simple on the surface: “**s corp or c corp in nevada**”. In practice, that choice determines how much of your profit gets hit by federal double tax, how much payroll tax you pay on your own compensation, and how aggressive you can be with retirement and fringe benefit strategies.

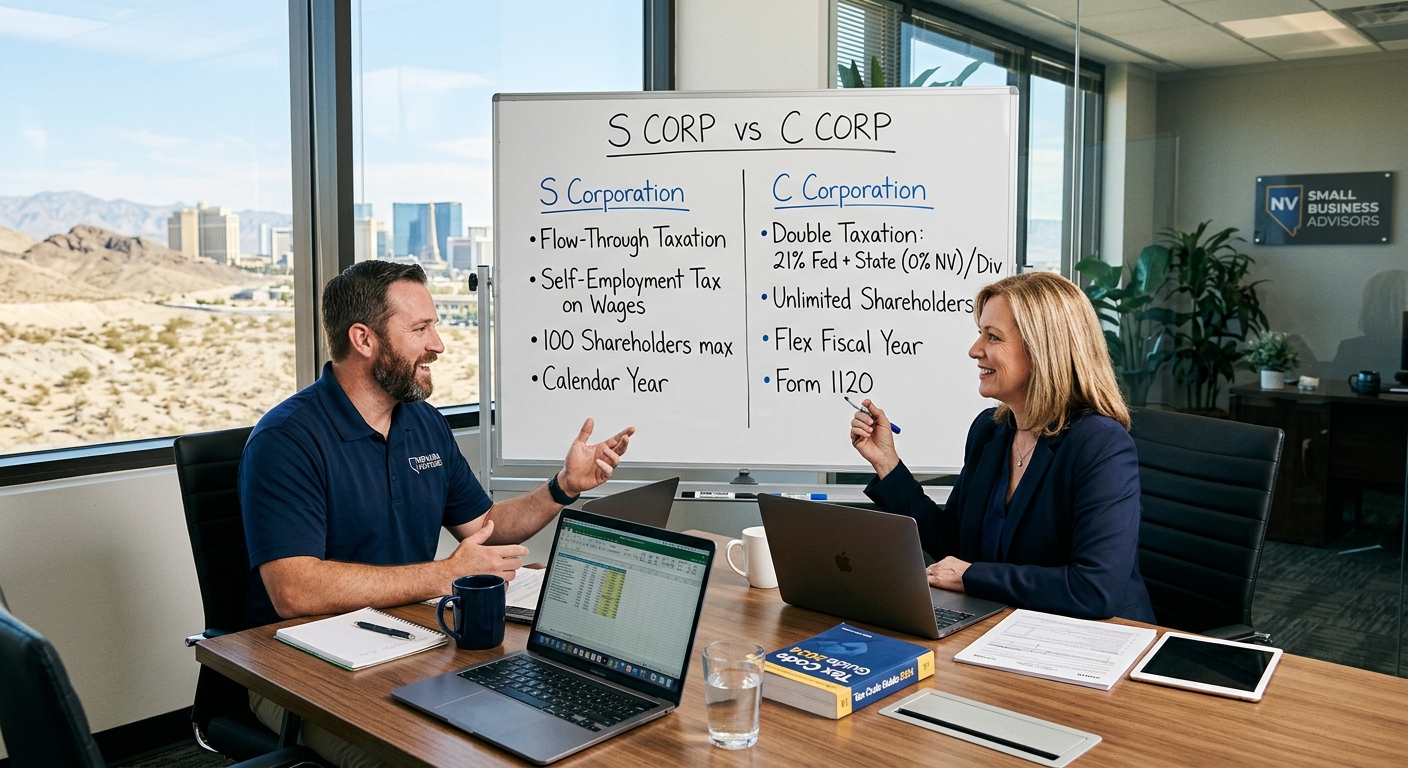

Quick Answer: How Nevada Corporations Are Really Taxed

Nevada does not impose a traditional corporate income tax or personal income tax. That sounds like tax paradise, but it does not change the federal rules. A C corporation still pays federal corporate income tax on its profits and shareholders may pay additional tax on dividends. An S corporation is generally a pass-through: there is no federal corporate income tax and profits flow through to shareholders’ personal returns.

The real question is whether your Nevada business is better off accepting C corporation double taxation in exchange for broader fringe benefits, or using S corporation pass-through treatment and salary plus distributions to cut federal employment taxes. The answer depends on your profit level, how much cash you want to pull out of the company, and your long term exit plan.

How C Corporations Work For Nevada Owners

A C corporation is the default federal tax treatment for a corporation. It files Form 1120 and pays federal corporate tax on its taxable income. When it pays dividends to shareholders, those shareholders pay tax again on their personal returns. That double layer is the main downside, but it is not always a dealbreaker.

Federal tax math on a Nevada C corporation

Assume Maria owns a Nevada marketing agency that earns $400,000 in taxable profit inside a C corporation. For simplicity, assume a flat 21 percent federal corporate tax rate. The corporation pays $84,000 of federal tax and keeps $316,000 after tax. If Maria distributes $200,000 of that as qualified dividends, she could easily face a combined 15–23.8 percent tax on the dividend, say roughly $38,000. Total federal tax burden is about $122,000.

Because Nevada has no corporate or personal income tax, there is no additional state income tax on either the corporate profit or the dividend. However, the corporation may still owe Nevada Commerce Tax if gross receipts exceed the state’s threshold and may owe Modified Business Tax on certain payroll, plus annual list and business license fees to the Nevada Secretary of State.

When a C corporation can still make sense

Despite the double tax issue, C corporations offer real advantages for certain owners:

- Richer fringe benefits: C corporations can fully deduct many employee benefits and, within limits, those benefits may be tax free to owner employees. Health reimbursement arrangements and some executive benefits are much more flexible in a C corporation environment. See IRS Publication 15-B for fringe benefit rules.

- Retained earnings strategy: If you plan to reinvest most profits into the business rather than distribute them, the corporate level tax may be acceptable, especially for high growth companies targeting a sale.

- Professional investor expectations: Venture capital and many institutional investors strongly prefer C corporations, especially if a future public offering is on the roadmap.

If you are a growth focused Nevada owner who plans to raise capital, does not need to pull out most of the profit personally, and wants maximum benefit flexibility, a C corporation can be the right vehicle even without Nevada income tax.

Red Flag Alert: Accumulated earnings and personal expenses

The IRS expects C corporations to distribute earnings or reinvest them in the business. If the corporation stockpiles excess cash beyond its reasonable business needs, it can be hit with the accumulated earnings tax. Personal expenses disguised as corporate deductions are another red flag; they can be reclassified as constructive dividends and taxed again at the shareholder level. See IRS Publication 542 for corporation specific rules.

Why Nevada S Corporations Are So Popular

Electing S corporation status is a federal decision that changes how your corporation is taxed, not how it is formed under Nevada law. An S corporation files Form 1120-S and passes its income, deductions, and credits through to shareholders who report them on their personal returns, generally avoiding federal corporate level income tax.

The salary plus distribution advantage

For active owners, the main S corporation advantage is employment tax savings. You must pay yourself a reasonable salary subject to Social Security and Medicare taxes, but profits above that salary can usually be distributed as S corporation income that is not subject to those payroll taxes.

Consider Jacob, a Nevada consultant with $200,000 of net profit. As a sole proprietor, that entire $200,000 is hit by the 15.3 percent self employment tax, resulting in roughly $30,600 of federal employment taxes on top of income tax. If he operates as an S corporation, pays himself an $110,000 salary and takes $90,000 as a distribution, only the $110,000 is subject to Social Security and Medicare. That alone can cut his federal employment taxes by roughly $13,000 a year, depending on wage base limits.

Nevada’s lack of personal income tax means the pass through S corporation income is not taxed at the state level, which further strengthens this structure for owner operators.

Reasonable salary is not optional

The IRS scrutinizes S corporation owners who pay themselves artificially low salaries to avoid payroll taxes. In audits, agents often reclassify some distributions as wages and assess back employment taxes, penalties, and interest. According to IRS guidance on S corporation compensation, factors like your training, time devoted to the business, and what similar businesses pay are part of the reasonable salary test.

This is where working with advisors who understand owner compensation benchmarks is critical. KDA regularly helps business owners document and defend their salary numbers so they enjoy employment tax savings without painting a target on their backs.

How S corporations interact with other benefits

S corporation owners can still sponsor retirement plans such as a Solo 401(k) or SEP IRA, and in many cases they can shelter a large share of their salary and profits. Health insurance and certain fringe benefits are treated differently for more than 2 percent S corporation shareholders, so you have to be precise about how premiums are paid and reported on Form W-2. See the health insurance guidance in IRS rulings for S corporation shareholders.

Comparing Nevada S Corp and C Corp For Different Owners

There is no universal rule that one type is always better. The right answer for you depends on your income pattern, exit goals, and how you plan to use the cash the business generates.

Scenario 1: Solo consultant or 1099 professional

For a solo CPA, designer, or consultant earning between $120,000 and $350,000, an S corporation structure in Nevada is often hard to beat. You can pull a defensible salary and take the rest as distributions, reducing self employment tax while still contributing heavily to retirement. In this range, a C corporation normally pushes more total tax because the owner needs to withdraw most of the profit personally, triggering both corporate and dividend level tax.

To quantify the difference for your own numbers, plug your expected profit into a tool like a small business tax calculator so you can see how corporate and pass through options compare at a high level.

Scenario 2: Real estate investor with Nevada property holding company

Passive income behaves differently. If you hold rental property inside a C corporation, you may find it difficult and expensive to extract profits or exit the structure cleanly. Many real estate investors instead hold properties in LLCs taxed as partnerships or disregarded entities and use separate S corporations for management companies and active income. KDA’s work with real estate investors often involves multiple entities to keep liability, financing, and tax planning aligned.

Scenario 3: High growth startup eyeing a sale

Tech, manufacturing, and product startups that expect to raise capital or go through an exit often favor a Nevada C corporation, partly because professional investors are used to that structure. If the corporation qualifies for Section 1202 qualified small business stock (QSBS), some shareholders may exclude a large portion of their gain from federal tax when they eventually sell, subject to strict rules in IRS guidance on QSBS. That potential upside can outweigh payroll tax savings in certain cases.

KDA Case Study: Nevada Consultant Restructures For S Corporation Savings

Michael is a 1099 software engineer who moved from California to Nevada for both lifestyle and tax reasons. His one person LLC was reporting $260,000 of net Schedule C income, all of which was subject to the 15.3 percent self employment tax. After moving, he correctly paid no Nevada personal income tax, but his federal employment tax bill was still around $34,000 a year.

When Michael engaged KDA, we analyzed whether a Nevada C corporation or S corporation would better fit his situation. Because he takes home most of his profit each year and has no plans to raise outside capital, we recommended a corporation with an S election. We helped him incorporate in Nevada, file Form 2553 on time, and implement payroll with an initial salary of $135,000 based on market data for his role.

In the first full year after the restructuring, the corporation reported $270,000 of profit. Michael’s $135,000 salary was subject to payroll taxes, but the remaining $135,000 was treated as S corporation distributions not subject to Social Security and Medicare. The shift reduced his federal employment taxes by about $10,500 that year even after factoring in additional payroll costs and our advisory fee of $3,200. That is more than a 3x first year return, with similar or higher savings expected in future years as his income grows.

Ready to see how we can help you? Explore more success stories on our case studies page to discover proven strategies that have saved our clients thousands in taxes.

What About Nevada State Level Entity Costs?

Nevada’s tax reputation is based on the absence of traditional corporate and personal income tax, but every entity still deals with state level fees and, for larger businesses, the Commerce Tax and Modified Business Tax. Those costs should be part of your S versus C corporation analysis even though they do not change the federal rules.

Nevada Commerce Tax and gross receipts

The Commerce Tax applies to Nevada businesses whose gross revenue exceeds a statutory threshold during a fiscal year. The rate depends on your industry classification. Because this tax is based on gross revenue, not profit, it can still bite thin margin businesses that are barely breaking even.

A corporation may deduct state level taxes for federal purposes subject to the limitations in the Tax Cuts and Jobs Act, but the cash impact is real. When owners focus only on income tax and ignore Commerce Tax exposure, they underestimate the total cost of doing business in Nevada.

Modified Business Tax and payroll planning

Nevada’s Modified Business Tax is a payroll based tax on employers that exceed a certain wage threshold. For S corporation owners whose primary goal is to reduce employment taxes, this additional state payroll tax may slightly change the ideal salary versus distribution mix. However, because there is no state personal income tax on S corporation distributions, the net benefit of the structure generally remains intact for profitable owner operators.

Our tax planning services explicitly model the interaction between reasonable salary, federal employment taxes, Nevada payroll taxes, and retirement contributions so owners are not fixing one problem while accidentally creating another.

Annual list, licenses, and compliance friction

Regardless of whether you choose an S corporation or C corporation, Nevada requires annual list filings and business license renewals through the Secretary of State. Missing deadlines can lead to penalties or administrative dissolution. These are not tax costs in the strict sense, but they are part of the cost of maintaining a Nevada entity and should be budgeted alongside accounting and payroll costs.

Common Mistakes Nevada Owners Make With S And C Corporations

Choosing the wrong structure costs money, but the mistakes inside each structure are just as dangerous. The IRS and state agencies look for certain patterns that often signal deeper problems.

Underpaying S corporation salary

Owners attracted to S corporation status for payroll tax savings sometimes forget the reasonable salary requirement. If you are taking home $250,000 a year from your Nevada business and only paying yourself $30,000 of W-2 wages, the IRS does not need sophisticated analytics to know something is off. During an audit, they can reclassify a large portion of your distributions as wages and assess employment taxes under IRS Publication 15, plus penalties.

Running personal lifestyle through a C corporation

Some C corporation owners treat the corporate bank account as an ATM for personal spending, booking vacations, family vehicles, or personal subscriptions as “business” expenses. The IRS can reclassify these as constructive dividends, meaning the corporation loses the deduction and the shareholder owes tax on the deemed dividend. That double hit often dwarfs any short term benefit from the write off.

Ignoring retirement and fringe benefit opportunities

Both S and C corporations can sponsor powerful retirement plans and provide valuable benefits. Too many owners fixate entirely on today’s tax bill and ignore the chance to shelter $60,000, $100,000, or more per year through defined benefit or cash balance plans layered on top of 401(k) plans. According to IRS guidance on defined benefit plans, older, high earning owners are often in the best position to use these strategies.

How To Decide: A Practical Framework

Instead of asking which structure is best in the abstract, work through a basic framework for your own Nevada business. The right answer for a W-2 engineer with a new side consulting practice will not match the right answer for a multi founder startup planning a venture round.

Key questions to answer before you choose

- How much profit do you realistically expect over the next three years?

- How much of that profit will you need to live on versus reinvest in the business?

- Do you anticipate raising outside equity capital or staying closely held?

- Is your industry better matched to pass through treatment or C corporation norms?

- How important are fringe benefits like health reimbursements, executive benefits, and large retirement contributions?

Once you have those answers, you can model each structure side by side. KDA often starts with a simple comparison: what is your total federal and Nevada tax burden if you operate as a sole proprietor, an S corporation, and a C corporation, assuming the same underlying profit?

Bottom Line: Use the right tool for the right job

If you are an owner operator who needs to pull out most of your Nevada business profit each year and does not plan to raise institutional capital, S corporation status usually offers better long term results when executed correctly. If you are building a capital intensive, growth oriented company where reinvestment and outside equity are central, a C corporation can still be the strategic choice, especially with QSBS potential.

This information is current as of 5/14/2026. Tax laws change frequently. Verify updates with the IRS or Nevada Department of Taxation if you are reading this at a later date.

Will Switching Structures Trigger An Audit?

Changing from a default C corporation to an S corporation, or converting an LLC into a corporation that then elects S status, does not automatically trigger an IRS audit. What gets attention is sloppy execution: late or incomplete elections, inconsistent reporting between corporate and shareholder returns, or sudden drastic shifts in reported wages without a clear business reason.

Handled correctly, a restructuring can actually reduce your long term audit risk by cleaning up messy books, clarifying how owners are compensated, and aligning distributions with documented board decisions.

Ready to Reduce Your Tax Bill?

KDA Inc. specializes in strategic tax planning for business owners, S Corps, LLCs, and high-net-worth individuals. Book a personalized consultation and walk away with a clear plan.

FAQ: Nevada S Corp vs C Corp

Does Nevada’s lack of income tax automatically make an S corporation better?

No. The absence of state income tax benefits both C corporation and S corporation shareholders. The key differences between S and C status are still driven by federal rules on corporate income tax, dividends, employment taxes, and benefits.

Can a Nevada LLC choose S corporation or C corporation tax treatment?

Yes. A Nevada LLC can elect to be taxed as a corporation and then further elect S corporation status if it meets the eligibility rules in IRS guidance on corporations. You do not always need to form a traditional corporation under Nevada law to access S corporation tax treatment.

What if I change my mind later?

Moving from S corporation back to C corporation is possible but constrained by built in gains tax rules and timing restrictions. Moving the other direction from C to S can also trigger built in gains tax if the corporation holds appreciated assets. These transitions must be modeled carefully before you file any elections.

Book Your Tax Strategy Session

If you are wrestling with the s corp or c corp in nevada decision and guessing instead of running the numbers, you are leaving money on the table and adding risk you cannot see yet. KDA’s advisory team builds entity structures for W-2 professionals with side businesses, 1099 consultants, real estate investors, and high net worth families so each dollar of profit goes to the right place with the right tax cost. Click here to book your consultation now.

Key Takeaway: The IRS is not hiding these tax outcomes; you just have to match the structure to your real goals instead of copying what your friend did.

Top three takeaways you can reuse for social or email:

- Nevada’s lack of state income tax does not eliminate federal double taxation for C corporations, but it amplifies S corporation pass through advantages for owner operators.

- For profitable Nevada consultants and 1099 professionals, a properly executed S corporation can cut federal employment taxes by five figures while keeping compliance under control.

- High growth Nevada startups often accept C corporation double tax in exchange for investor access and potential QSBS gains exclusion; the right answer depends on your exit plan, not just today’s tax bill.