Quick Answer

The 2026 max gift amount you can give tax-free is $13.99 million per person ($27.98 million per married couple) for lifetime gifts, plus $19,000 per recipient annually without touching your lifetime exemption. Thanks to the One Big Beautiful Bill passed in 2025, these exemption levels are now permanent, eliminating the previous 2025 sunset deadline that caused wealthy families to rush their estate planning decisions.

Why the 2026 Max Gift Amount Matters More Than Ever

You’ve spent decades building wealth. Maybe you own multiple rental properties across California, hold executive stock positions worth seven figures, or run a successful medical practice that generates $800,000 annually. Now you want to pass assets to your children without the IRS claiming 40% of everything above the exemption threshold.

Here’s the problem most high-net-worth families face: they either give away too much too fast (and lose control), or they wait too long and get hit with massive estate taxes when they die. The 2026 gift tax rules offer a middle path, but only if you understand exactly how the system works.

The confusion stems from three separate gift tax numbers that all apply simultaneously. There’s the annual exclusion ($19,000 per recipient in 2026), the lifetime exemption ($13.99 million per person), and the estate tax exemption (same $13.99 million). Mix these up, and you’ll either overpay taxes or trigger an IRS audit.

What changed in 2025 is permanence. The Tax Cuts and Jobs Act was scheduled to sunset on December 31, 2025, which would have slashed the lifetime exemption in half to approximately $7 million per person. Wealthy families scrambled throughout 2024 and early 2025 to accelerate gifts into irrevocable trusts, only to discover in July 2025 that Congress made the higher exemptions permanent. Some now have buyer’s remorse for giving away assets they could have kept longer.

Breaking Down the 2026 Max Gift Amount Rules

The IRS structures gift tax rules in layers. Understanding each layer determines whether you owe tax, file paperwork, or operate completely under the radar.

Annual Exclusion: The Stealth Gifting Strategy

You can give $19,000 to as many people as you want in 2026 without filing a single form. This is the annual exclusion amount, indexed for inflation. If you’re married, you and your spouse can combine your exclusions to give $38,000 per recipient.

Example: David and Sarah Chen, both 62, have three adult children and seven grandchildren. In 2026, they can transfer $380,000 total ($38,000 to each of 10 family members) without filing IRS Form 709 or using any of their lifetime exemption. Over 10 years, that’s $3.8 million moved out of their taxable estate with zero tax consequences.

The annual exclusion resets every January 1. If you give your daughter $19,000 on December 30, 2026, you can give her another $19,000 on January 2, 2027. The IRS treats these as separate tax years.

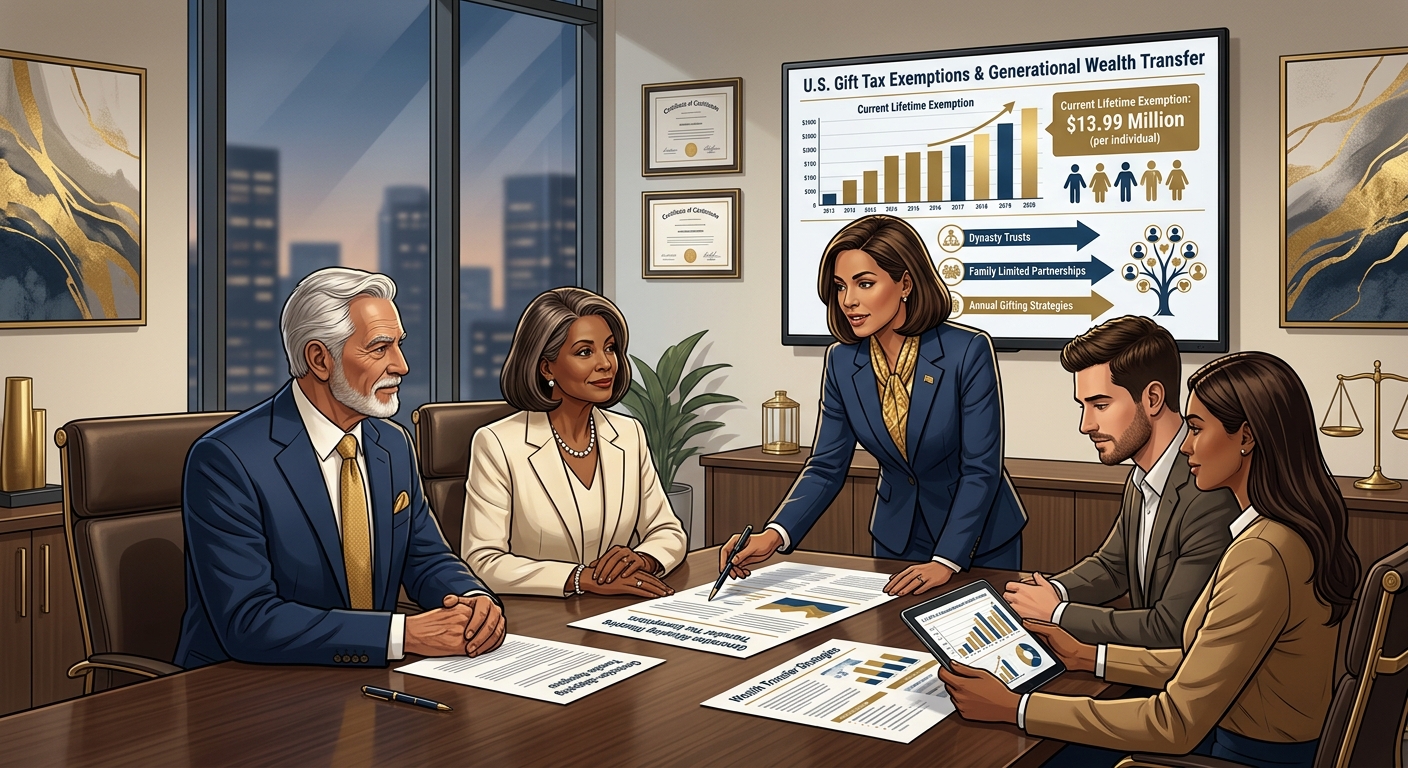

Lifetime Exemption: Your $13.99 Million Shield

Any gift above the annual exclusion amount counts against your lifetime exemption. The 2026 lifetime gift and estate tax exemption is $13.99 million per individual. Married couples can combine exemptions for a total of $27.98 million.

This means you can give away $13.99 million during your lifetime, beyond the annual exclusion gifts, without paying federal gift tax. When you die, whatever exemption you haven’t used applies to your estate. If you’ve used $5 million during life, you have $8.99 million remaining to shelter your estate from the 40% federal estate tax.

Here’s what triggers the lifetime exemption: Let’s say you give your son $100,000 in 2026 to help with a home down payment. The first $19,000 falls under the annual exclusion. The remaining $81,000 counts against your $13.99 million lifetime exemption. You must file IRS Form 709 (Gift Tax Return) to report this, but you owe zero tax because you’re still $13,909,000 below your lifetime limit.

The California Twist: No State Gift Tax

California does not impose a state-level gift tax. You can transfer millions to your children while living in San Diego or San Francisco without triggering California tax liability. However, California does have an estate tax consideration: assets you give away during life escape California estate tax (which doesn’t currently exist but could be reinstated by future legislation).

The strategy here for California residents: Use the federal lifetime exemption aggressively while California has no estate tax. If state legislation changes, assets already transferred are protected.

Strategic Gifting Moves for 2026

Knowing the rules is one thing. Applying them to reduce your family’s tax burden by six figures requires specific tactical moves.

Front-Loading 529 Plans with Five Years of Annual Exclusions

IRS rules allow you to contribute five years’ worth of annual exclusion gifts to a 529 college savings plan in a single year. In 2026, that means $95,000 per beneficiary ($190,000 if married). This technique, called “superfunding,” moves a large sum out of your taxable estate immediately while maintaining the annual exclusion treatment.

The catch: You cannot make additional annual exclusion gifts to that beneficiary for the next four years. If you die within the five-year period, a prorated portion of the contribution is pulled back into your estate for tax purposes.

Example: Dr. Michelle Rodriguez, an orthopedic surgeon earning $625,000 annually, has two grandchildren ages 3 and 5. In March 2026, she contributes $95,000 to each grandchild’s 529 plan, totaling $190,000. These gifts are treated as $19,000 per year for five years, using her annual exclusion without touching her lifetime exemption. By 2031, she can resume annual gifts. If the investments grow to $300,000 by the time her grandchildren attend college, that $110,000 of growth also escapes estate tax.

Paying Tuition and Medical Expenses Directly

There’s a gift tax loophole most families miss: unlimited tax-free transfers for education and medical expenses, as long as you pay the institution directly. This does not count against your annual exclusion or lifetime exemption.

You can write a $60,000 check directly to Stanford University for your grandson’s tuition, then give him an additional $19,000 cash gift for living expenses, all in the same year. The $60,000 tuition payment is completely exempt under IRC Section 2503(e). The $19,000 cash uses your annual exclusion. Total transferred: $79,000 with zero gift tax consequences.

This strategy works for medical insurance premiums, too, if paid directly to the insurance company. However, it does not apply to reimbursements. If your daughter pays her own medical bill and you reimburse her, that counts as a taxable gift.

Spousal Gifts: The Unlimited Marital Deduction

Gifts between U.S. citizen spouses are 100% tax-free with no limit. You can transfer $50 million to your spouse in 2026 without filing IRS Form 709 or using any exemption. This is the unlimited marital deduction under IRC Section 2523.

If your spouse is not a U.S. citizen, the rules change. In 2026, you can give up to $185,000 annually to a non-citizen spouse tax-free. Amounts above that trigger gift tax or use your lifetime exemption.

Strategic consideration: Equalizing estates between spouses before death maximizes the use of both exemptions. If one spouse has $20 million and the other has $2 million, transferring $9 million to the lower-net-worth spouse ensures both can use their full $13.99 million exemptions upon death, sheltering $27.98 million instead of $20 million.

What Happens If You Exceed the 2026 Max Gift Amount?

Let’s be clear: exceeding the lifetime exemption doesn’t automatically mean you owe tax. It means you need to file Form 709 and track your cumulative gifts. The IRS only collects the 40% gift tax when your total lifetime gifts exceed $13.99 million.

The Form 709 Filing Requirement

You must file IRS Form 709 if you make gifts exceeding the annual exclusion to any individual during the year. The deadline is April 15 of the year following the gift (the same deadline as your income tax return).

Form 709 requires you to report the recipient, the asset transferred, its fair market value, and whether you’re splitting the gift with your spouse. The IRS uses this form to track your cumulative lifetime gifts against your exemption.

Failure to file Form 709 keeps the statute of limitations open indefinitely for those gifts. The IRS can audit the valuation of gifts you made 20 years ago if you never filed the required form. Proper filing closes the audit window after three years (six years if the IRS believes you undervalued assets by more than 25%).

When You Actually Owe Gift Tax

Gift tax is due only when your cumulative lifetime gifts exceed $13.99 million (or $27.98 million for married couples). At that point, the tax rate is a flat 40% on the excess.

Example: Richard Park, a commercial real estate developer, has made $14.5 million in lifetime gifts by December 2026. He has exceeded his exemption by $510,000. He owes federal gift tax of $204,000 (40% of $510,000), payable with his 2026 Form 709 by April 15, 2027.

This rarely happens. Most high-net-worth individuals stop gifting once they approach their exemption limit, preserving the remaining exemption for estate tax purposes. The 40% gift tax and 40% estate tax are unified, meaning you’re indifferent between paying during life or at death from a pure tax perspective (though lifetime gifts allow appreciation to occur outside your estate).

Advanced Wealth Transfer Strategies Beyond Simple Gifting

Once you’ve maximized annual exclusion gifts and understand your lifetime exemption, the next level involves structures that leverage your exemption for greater tax efficiency.

Grantor Retained Annuity Trusts (GRATs)

A GRAT allows you to transfer appreciating assets to your children while using little to none of your lifetime exemption. Here’s how it works: You transfer assets (typically stock or business interests) into a trust and retain the right to receive an annuity for a set term (usually 2-5 years). At the end of the term, whatever remains in the trust passes to your beneficiaries tax-free.

The gift tax value is the present value of the remainder interest, which can be calculated to be near zero if the annuity payments are structured correctly. If the assets appreciate above the IRS assumed rate (currently 5.6% as of May 2026), that excess appreciation transfers tax-free.

Example: Jennifer Liu, a tech executive, transfers $3 million of pre-IPO company stock into a 3-year GRAT in January 2026. She receives annuity payments totaling $3.1 million over three years (designed to zero out the taxable gift). The stock appreciates to $8 million by December 2028. The $4.9 million of appreciation passes to her children without using any of her $13.99 million lifetime exemption. If Jennifer had simply gifted the stock, it would have used $3 million of her exemption.

The risk: If you die during the GRAT term, the assets are pulled back into your estate as if the GRAT never existed. For this reason, wealthy families often set up multiple “rolling” GRATs with short terms to minimize mortality risk.

Irrevocable Life Insurance Trusts (ILITs)

Life insurance death benefits are income tax-free, but they are included in your taxable estate if you own the policy when you die. For a high-net-worth individual with a $5 million policy, that means $2 million of unnecessary estate tax (40% of $5 million).

An ILIT removes life insurance from your estate. You create an irrevocable trust, transfer an existing policy (or purchase a new policy within the trust), and the trust owns the policy. When you die, the death benefit pays to the trust, which distributes proceeds to beneficiaries estate-tax-free.

The annual premiums you pay into the trust are gifts to the beneficiaries. If structured with “Crummey powers” (beneficiaries have the temporary right to withdraw contributions), the premiums qualify for the annual exclusion.

Example: Thomas and Rebecca Nguyen, both 58, have a $28 million estate and a $3 million second-to-die life insurance policy. They create an ILIT and transfer the policy to the trust. Annual premiums are $48,000. They gift the premium amount to the trust each year, and their three children receive Crummey notices giving them 30 days to withdraw the contribution (they never do). The $48,000 gift is covered by their combined annual exclusion ($38,000) plus $10,000 against their lifetime exemption. When both pass away, the $3 million death benefit escapes the 40% estate tax, saving $1.2 million.

Qualified Personal Residence Trusts (QPRTs)

A QPRT allows you to transfer your home to your children at a reduced gift tax value while continuing to live in it for a specified term. The gift value is discounted because your children don’t receive the property immediately.

If you transfer a $2 million home via a 10-year QPRT, the taxable gift might be only $800,000 (the present value of the remainder interest). After 10 years, the home belongs to your children, but the $1.2 million of future appreciation escapes your estate. If you want to continue living there, you pay your children fair market rent, which further reduces your estate while transferring wealth.

The catch: If you die during the 10-year term, the full value of the home is included in your estate, and the strategy fails.

KDA Case Study: High-Net-Worth Family Avoids $890,000 in Estate Tax

James and Patricia Hoffman, both 67, came to KDA in January 2026 with a $32 million estate: $18 million in commercial real estate, $9 million in brokerage accounts, $3 million in a primary residence, and $2 million in business interests. They have two adult children and wanted to reduce future estate taxes.

Without planning, their estate would exceed the $27.98 million combined exemption by $4.02 million, triggering $1.61 million in federal estate tax at 40%. California has no estate tax currently, but the Hoffmans were concerned about future state legislation.

KDA implemented a three-part strategy. First, we established a 3-year GRAT funded with $4 million of their highest-growth commercial property. The property appreciated 12% annually, transferring $1.6 million of appreciation to their children outside the estate. Second, we created an ILIT to hold their $2.5 million life insurance policy, removing it from the taxable estate and saving $1 million in estate tax. Third, we implemented annual exclusion gifting: $38,000 per child ($76,000 total) plus $95,000 superfunded 529 contributions for each of four grandchildren ($380,000 total).

Over three years, these strategies reduced their taxable estate from $32 million to $26.8 million, falling below the exemption threshold. Estimated estate tax savings: $2.08 million. KDA’s fee for planning and implementation: $18,500. First-year ROI: 112x. The Hoffmans now gift $76,000 annually and update their plan every two years to adapt to law changes and asset appreciation.

Ready to see how we can help you? Explore more success stories on our case studies page to discover proven strategies that have saved our clients thousands in taxes.

Common Mistakes That Trigger IRS Scrutiny

Gift tax planning is unforgiving. Small errors create large problems, especially when the IRS audits your estate after death and your family has to defend valuations and filing positions.

Red Flag Alert: Failing to File Form 709

The most common mistake is making a gift above the annual exclusion and not filing Form 709. Some taxpayers believe that because they owe no tax (their gift is under the lifetime exemption), no filing is required. Wrong. The IRS uses Form 709 to track cumulative gifts and start the statute of limitations. Without the form, the IRS can challenge gift valuations decades later.

If you gift your daughter $100,000 in 2026 and don’t file Form 709, the IRS can audit that gift in 2046 when you die, claiming the asset was worth $300,000 at the time of transfer. With a properly filed Form 709, the audit window closes in 2029 (three years after filing).

Red Flag Alert: Undervaluing Gifted Assets

Gifting a family business interest, real estate, or private company stock requires a qualified appraisal. The IRS scrutinizes these valuations, especially when applying minority interest discounts or lack-of-marketability discounts.

If you claim your 25% interest in a family LLC is worth $500,000 (with a 30% discount from its pro-rata value), but the IRS determines it should be valued at $750,000, you’ve underreported the gift by $250,000. If this exceeds 25% of the reported value (it does: $250,000 / $500,000 = 50%), the statute of limitations extends from three years to six years, and you may face a 20% accuracy-related penalty.

Pro Tip: Obtain a contemporaneous qualified appraisal for any gift of hard-to-value assets. The cost of a $3,500 appraisal is minor compared to defending an IRS challenge without documentation.

Red Flag Alert: Incomplete Gift Transfers

For a gift to be complete (and removed from your estate), you must relinquish all control over the asset. If you transfer stock to your son but retain the right to vote the shares or receive dividends, the IRS treats this as an incomplete gift. The asset remains in your taxable estate.

This issue arises frequently with family LLCs. Parents transfer LLC interests to children but retain 100% management control as the general partner. If the LLC operating agreement allows the general partner to unilaterally reclaim distributions or dissolve the entity, the IRS may argue the gifts are incomplete.

How the One Big Beautiful Bill Changed Everything

Before July 2025, estate planners operated under a ticking clock. The Tax Cuts and Jobs Act exemptions were set to expire on December 31, 2025, cutting the lifetime exemption roughly in half to $7 million per person. Wealthy families rushed to lock in gifts before the deadline.

Then Congress passed the One Big Beautiful Bill (OBBB) in July 2025, making the $13.99 million exemption permanent. No more sunset. No more cliff. The exemption will continue to adjust for inflation annually, but the base amount is now locked into law.

This created an unexpected problem: families who accelerated gifts into irrevocable trusts in 2024 and 2025 now have buyer’s remorse. They gave away assets they could have retained and enjoyed for years longer. Some have attempted to unwind these gifts using trust decanting provisions, but the options are limited once assets are in an irrevocable structure.

The takeaway: The permanence of the exemption means you can slow down. There’s no deadline pressure. You can implement a thoughtful, phased gifting strategy over 10-20 years instead of rushing to transfer millions by year-end.

Who Should Use Their Lifetime Exemption Now vs. Later?

Just because the exemption is permanent doesn’t mean you should use it immediately. The decision depends on your age, asset growth rate, and liquidity needs.

Use Your Exemption Now If:

- Your assets are appreciating rapidly (pre-IPO stock, high-growth real estate, crypto holdings above $1 million)

- You’re over age 60 and your estate exceeds the exemption threshold

- You have sufficient assets to maintain your lifestyle after gifting

- You want to remove future appreciation from your taxable estate

Example: A 55-year-old tech executive with $8 million in pre-IPO stock expecting a 5x return at IPO should gift now. If the stock becomes worth $40 million, the $32 million of appreciation occurs outside the estate. Waiting until after IPO means that appreciation is taxed at 40% upon death.

Wait to Use Your Exemption If:

- You’re under age 50 and uncertain about future financial needs

- Your assets are stable or slow-growth (bonds, CDs, blue-chip dividend stocks)

- You may need asset liquidity for long-term care or medical expenses

- You’re charitably inclined and plan to leave assets to tax-exempt organizations (which don’t benefit from lifetime gifting)

Remember: Gifts are irrevocable. Once transferred, you cannot reclaim assets if your circumstances change. The permanence of the exemption means there’s no penalty for waiting.

Ready to Reduce Your Tax Bill?

KDA Inc. specializes in strategic tax planning for business owners, S Corps, LLCs, and high-net-worth individuals. Book a personalized consultation and walk away with a clear plan.

Frequently Asked Questions

Can I gift my primary residence to my children and continue living in it?

Yes, but you must pay fair market rent to your children, or the IRS will treat your continued occupancy as a retained interest, pulling the home back into your taxable estate. A better strategy is a Qualified Personal Residence Trust (QPRT), which allows you to live rent-free during the trust term, then pay rent after the term ends.

What happens to my unused lifetime exemption when I die?

Your remaining exemption applies to your estate. If you used $4 million during life, you have $9.99 million remaining to shelter estate assets from the 40% federal estate tax. For married couples, portability allows the surviving spouse to use the deceased spouse’s unused exemption, but this requires filing IRS Form 706 within nine months of death, even if no estate tax is owed.

Do gifts affect my income taxes?

No. Gift tax is separate from income tax. The recipient of a gift pays no income tax on the amount received. However, the recipient inherits your cost basis in appreciated assets. If you gift stock you purchased for $100,000 (now worth $500,000), your child’s basis remains $100,000. When they sell, they owe capital gains tax on $400,000. By contrast, inherited assets receive a step-up in basis to fair market value at death, erasing the built-in gain.

Are there any assets I should never gift?

Highly appreciated assets with low basis are poor candidates for lifetime gifts because the recipient inherits your basis and loses the step-up at death. For example, if you own stock purchased for $50,000 now worth $2 million, gifting it costs your child $487,500 in future capital gains tax (25% federal and state on $1.95 million gain). If you hold it until death, they inherit it at $2 million with no built-in gain. Better gift candidates: cash, recently purchased assets, or assets expected to appreciate significantly in the future.

California-Specific Estate Planning Considerations

California does not currently impose a state estate tax or state gift tax, making it one of the most tax-friendly states for wealth transfer. However, California is one of nine community property states, which affects how assets are treated for gift and estate tax purposes.

Community Property Implications

Assets acquired during marriage while living in California are generally community property, meaning each spouse owns 50%. When gifting community property, both spouses must consent, even if only one spouse is the named owner. Failing to obtain spousal consent can result in incomplete gift treatment.

Community property receives a full step-up in basis for both halves when the first spouse dies, unlike separate property (which only steps up the deceased spouse’s half). For highly appreciated California real estate, this can save $200,000+ in capital gains taxes for the surviving spouse.

Proposition 19 Impact on Parent-to-Child Transfers

California voters passed Proposition 19 in 2020, which significantly limited property tax reassessment exclusions for parent-to-child transfers. Previously, you could transfer your primary residence and up to $1 million of other real property to your children without triggering a property tax reassessment.

Under current law (as of 2026), the exclusion only applies if the child uses the property as their primary residence and the assessed value increase doesn’t exceed $1 million. If your $2 million home (with a $400,000 assessed value) is gifted to your daughter who doesn’t live there, the assessed value resets to $2 million, increasing her annual property tax by approximately $19,200 (1.2% of $1.6 million increase).

Strategy: If you plan to transfer California real estate to children who won’t occupy it as a primary residence, consider holding the property until death (when it receives a step-up in income tax basis) or transferring it into a trust that allows children to rent it at fair market value while minimizing property tax reassessment issues.

Planning for Potential Future Law Changes

While the $13.99 million exemption is now permanent under current law, “permanent” in tax legislation means “until Congress changes it.” Future administrations could reduce the exemption, especially if federal deficits continue to grow.

Historical context: The estate tax exemption was $600,000 in 1997, $1 million in 2002, $3.5 million in 2009, $5 million in 2011, and $11.18 million in 2018. It has increased significantly over 25 years, but it could also decrease if political priorities shift.

Hedging Against Future Reductions

If you’re concerned about future exemption reductions, consider using a portion of your exemption now to lock in today’s levels. Even if the exemption drops to $7 million in 2030, gifts made in 2026 under the $13.99 million exemption are grandfathered. The IRS will not claw back gifts made when the exemption was higher.

This was confirmed in IRS regulations issued in 2019, which explicitly stated that if you make a $10 million gift today and the exemption later drops to $5 million, your estate will not be penalized. You used the exemption lawfully when it was available.

Book Your Tax Strategy Session

If you’re sitting on a $15 million estate and haven’t implemented a gifting strategy, you could be leaving $2 million on the table in unnecessary estate taxes. The 2026 max gift amount rules create powerful opportunities, but only if your planning is precise, timely, and structured to withstand IRS scrutiny.

KDA specializes in high-net-worth estate and gift tax planning for California families. We combine federal tax strategy with California property tax optimization, trust structuring, and multi-generational wealth transfer. Our clients typically save between $500,000 and $3 million in estate taxes over their lifetime. Book your personalized estate tax strategy session now and find out exactly how much your family can save.

This information is current as of 5/10/2026. Tax laws change frequently. Verify updates with the IRS or FTB if reading this later.