Most California Business Owners Pick the Wrong Entity and Never Find Out Until Tax Day

A Sacramento consultant earned $220,000 in net profit last year. She filed as a default C Corporation because her attorney told her it was “the standard business structure.” She paid $78,400 in total federal and state taxes. Her neighbor, running the same type of consulting practice at the same income level, filed as an S Corporation. He paid $39,100. Same city, same profession, same revenue, a $39,300 gap in taxes owed. The only difference was one IRS election form.

The distinction between a C Corporation and S Corporation is not academic. It is the single most consequential tax decision a California business owner makes, and the wrong choice quietly drains thousands of dollars every single year. This guide breaks down exactly how both entities work in 2026, what each one costs you in real taxes, who wins with each structure, and how to switch if you are stuck in the wrong one.

Quick Answer

A C Corporation is taxed as a separate entity at 21% federal plus 8.84% California franchise tax, and profits are taxed again when distributed to shareholders as dividends. An S Corporation passes income directly to shareholders on their personal returns, avoids double taxation, qualifies for the 20% QBI deduction under IRC Section 199A, and pays only 1.5% California franchise tax. For most California business owners earning $80,000 to $350,000 in annual profit, the S Corporation saves between $14,000 and $65,000 per year in combined taxes.

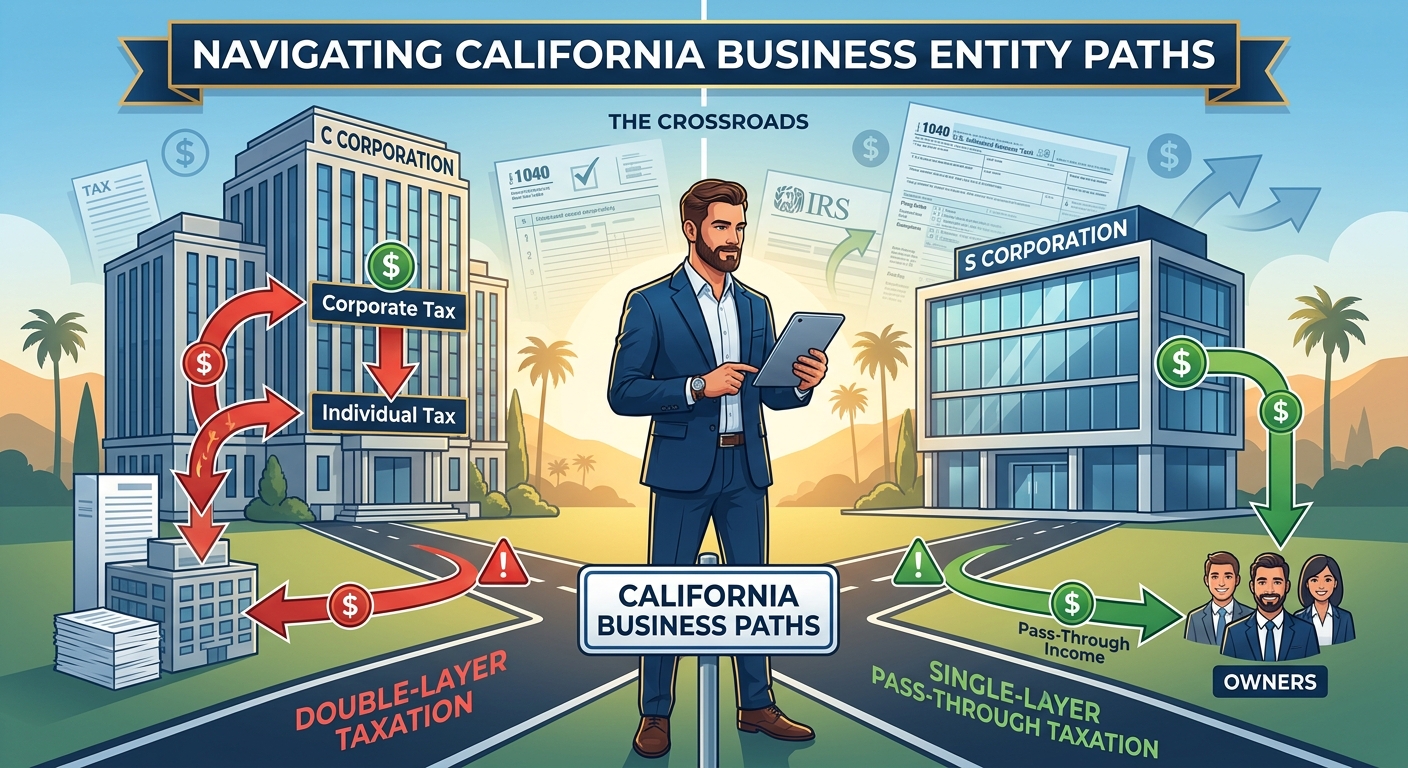

C Corporation S Corporation: How Each Entity Actually Gets Taxed in 2026

The tax treatment gap between these two entities is not a small technicality. It is a structural difference that compounds year after year. Here is exactly how each entity handles your money at the federal and state level.

C Corporation Tax Mechanics

A C Corporation, sometimes called a “regular corporation,” is treated by the IRS as a completely separate taxpayer from its owners. That means the corporation files its own return (Form 1120) and pays its own tax bill. When the remaining profits are distributed to shareholders as dividends, those shareholders pay tax again on their personal returns. This is what tax professionals call double taxation.

Here is the layer-by-layer breakdown for a California C Corp owner with $200,000 in net profit who distributes all remaining earnings:

- Federal corporate tax: 21% on $200,000 = $42,000

- California franchise tax: 8.84% on $200,000 = $17,680

- After-tax corporate profit: $200,000 minus $59,680 = $140,320

- Federal dividend tax: 15% on $140,320 = $21,048

- California dividend tax: 9.3% on $140,320 = $13,050

- Total tax paid: Approximately $93,778

- Effective rate: 46.9%

That number shocks most business owners the first time they see it calculated. The 21% federal rate looks attractive in isolation, but once you add the state layer and the shareholder dividend layer, the true cost is nearly half of every dollar you earn. For reference, see IRS Publication 542 for the complete rules on corporate taxation.

S Corporation Tax Mechanics

An S Corporation is a pass-through entity. The corporation itself pays zero federal income tax. Instead, all profits flow directly to the shareholders’ personal tax returns through Schedule K-1. California charges a reduced franchise tax of just 1.5% on S Corporation net income (minimum $800).

Same scenario: $200,000 net profit, single owner, California resident:

- Reasonable salary: $85,000 (subject to payroll taxes)

- Payroll taxes on salary: Approximately $13,005 (employer and employee combined FICA/Medicare)

- Federal income tax on $200,000 pass-through: Approximately $36,400 (after QBI deduction)

- QBI deduction: 20% of $115,000 distribution = $23,000 reduction in taxable income

- California income tax: Approximately $14,200

- California franchise tax: 1.5% on $200,000 = $3,000

- Total tax paid: Approximately $54,605

- Effective rate: 27.3%

Annual savings with S Corp: $39,173. That is not a rounding error. That is a second salary going straight to the IRS because of one entity selection choice.

Side-by-Side Tax Comparison Table

| Net Profit | C Corp Total Tax | S Corp Total Tax | Annual S Corp Advantage |

|---|---|---|---|

| $100,000 | $44,800 | $27,200 | $17,600 |

| $150,000 | $66,500 | $38,900 | $27,600 |

| $200,000 | $93,778 | $54,605 | $39,173 |

| $250,000 | $118,200 | $69,400 | $48,800 |

| $350,000 | $168,900 | $104,200 | $64,700 |

These numbers assume a single California resident, reasonable S Corp salary calibrated to industry standards, and full profit distribution. Your actual numbers will depend on filing status, other income sources, and deduction strategies. Want to run your own scenario? Plug your business profit into this small business tax calculator to estimate your total tax burden under both structures.

Five Tax Layers That Separate C Corporations From S Corporations

The gap between these two entities is not driven by one factor. It stacks across five distinct tax layers, and understanding each one reveals why the difference is so dramatic for California business owners.

Layer 1: Federal Entity-Level Tax

C Corporations pay a flat 21% federal tax on all net income before any money reaches the owner. S Corporations pay 0% at the entity level. Every dollar of C Corp profit loses 21 cents before the owner sees it. For a comprehensive breakdown of S Corp tax strategy, see our complete guide to S Corp tax strategy in California.

Layer 2: Federal Double Taxation on Dividends

When a C Corp distributes after-tax profits to shareholders, those dividends are taxed again at the shareholder level. Qualified dividends face rates of 0%, 15%, or 20% depending on income, plus the 3.8% Net Investment Income Tax (NIIT) for high earners under IRC Section 1411. S Corporation distributions from the Accumulated Adjustments Account (AAA) are generally tax-free because the income was already taxed on the shareholder’s personal return.

Layer 3: California Franchise Tax Differential

This is where California makes the gap even wider. C Corporations pay 8.84% franchise tax on net income. S Corporations pay 1.5% franchise tax on net income (with an $800 minimum). That is a 7.34 percentage point difference applied directly to your business profits every single year. On $200,000 in net income, the franchise tax differential alone is $14,680.

Layer 4: QBI Deduction Under IRC Section 199A

The Qualified Business Income (QBI) deduction, now made permanent under the One Big Beautiful Bill Act (OBBBA), allows S Corporation shareholders to deduct up to 20% of their qualified business income from their federal taxable income. C Corporation shareholders get zero QBI benefit. On $200,000 in S Corp profit (assuming $85,000 salary and $115,000 in distributions), the QBI deduction eliminates roughly $23,000 from your taxable income, saving approximately $5,060 in federal tax at the 22% bracket. California does not conform to the QBI deduction, so this benefit applies only at the federal level.

Layer 5: AB 150 Pass-Through Entity Tax Election

California’s AB 150 allows S Corporations and partnerships to elect to pay a 9.3% entity-level state tax, which generates a corresponding federal tax deduction that bypasses the $40,000 SALT deduction cap established under OBBBA. This election is exclusive to pass-through entities. C Corporations cannot use it. For a California business owner in the 32% or higher federal bracket, this election creates additional real savings of $3,000 to $8,000 per year by converting a lost state tax payment into a deductible business expense.

KDA Case Study: Construction Firm Owner Saves $41,200 With Entity Restructure

Marcus ran a Sacramento-based commercial construction management firm. His attorney had formed the business as a C Corporation in 2019, and Marcus never questioned the structure. With $240,000 in net profit in 2025, he paid $109,400 in combined federal and California taxes, including double taxation on his dividend distributions.

KDA’s team analyzed his full tax picture and recommended converting to an S Corporation through Form 2553 with a corresponding FTB Form 3560 notification to California. We set his reasonable salary at $95,000 based on Bureau of Labor Statistics data for construction management professionals in the Sacramento metro area, restructured his payroll, activated the AB 150 PTE election to bypass the $40,000 SALT cap, and established dual depreciation schedules to handle California’s bonus depreciation nonconformity under R&TC Sections 17250 and 24356.

In his first full year as an S Corp, Marcus’s total tax bill dropped to $68,200. That is a $41,200 annual savings. KDA’s engagement fee was $5,800, producing a 7.1x first-year return on investment. Over five years, projected cumulative savings exceed $196,000, assuming stable income and current tax law.

Ready to see how we can help you? Explore more success stories on our case studies page to discover proven strategies that have saved our clients thousands in taxes.

Five Costliest C Corporation S Corporation Mistakes California Owners Make

Choosing between a C Corporation and S Corporation is only the starting point. These five mistakes cost California business owners between $4,200 and $64,700 per year, and every single one is preventable.

Mistake 1: Staying in a Default C Corp Without Running the Numbers

Many business owners form a corporation with their attorney and never realize they defaulted into C Corp status. Every corporation is automatically a C Corp unless you file Form 2553 to elect S Corp treatment. If your attorney did not file that election, you have been paying double taxation since day one. The cost at $200,000 in annual profit: $39,173 per year in unnecessary taxes.

Mistake 2: Setting an Unreasonable S Corp Salary

The IRS requires S Corp owner-employees to pay themselves a “reasonable salary” before taking tax-free distributions. Setting your salary too low triggers IRS reclassification of distributions as wages, plus back payroll taxes, interest, and penalties. The landmark case Watson v. Commissioner established that compensation must reflect what a similar business would pay for similar services. Setting it too high eliminates the self-employment tax savings that make S Corps beneficial. The sweet spot is typically 40% to 60% of net profit, calibrated to industry benchmarks.

Mistake 3: Ignoring California’s Franchise Tax Differential

Some business owners compare federal rates only and conclude the C Corp’s flat 21% rate is “simpler.” But California’s franchise tax swings from 1.5% for S Corps to 8.84% for C Corps. On $200,000 in profit, that differential alone is $14,680. Add double taxation and lost QBI, and the gap widens to $39,000 or more. Always model both federal and California taxes before picking an entity.

Mistake 4: Missing the March 15 Form 2553 Deadline

To elect S Corp status for the current tax year, Form 2553 must be filed by March 15. Miss this deadline, and you are stuck as a C Corp for the entire year, costing you tens of thousands in avoidable taxes. Rev. Proc. 2013-30 provides late election relief if you qualify, but it requires demonstrating reasonable cause and filing within 3 years and 75 days of the intended effective date. Do not rely on this as your backup plan.

Mistake 5: Skipping California FTB Form 3560

California requires a separate S Corp election notification (FTB Form 3560) filed with the Franchise Tax Board. Filing Form 2553 with the IRS alone is not sufficient. If you skip the FTB notification, California will continue treating your entity as a C Corp and charging the 8.84% franchise tax rate instead of 1.5%. That mistake costs $14,680 per year on $200,000 in profit, and many business owners do not discover it until they receive an FTB notice years later.

Three Narrow Scenarios Where a C Corp Actually Wins

The S Corporation wins for the vast majority of California business owners, but three specific situations favor the C Corp structure. Before switching, verify that none of these apply to you.

Scenario 1: Venture Capital Funding

If you have a signed VC term sheet or are actively raising institutional capital, most investors require a Delaware C Corporation with multiple share classes (common and preferred stock). S Corporations cannot issue preferred stock because IRC Section 1361(b)(1)(D) limits them to one class of stock. If fundraising is your immediate priority, form a C Corp. If you are bootstrapping or growing organically, the S Corp saves you dramatically more.

Scenario 2: Qualified Small Business Stock (QSBS) Under IRC Section 1202

QSBS allows C Corp founders to exclude up to 100% of capital gains (up to $10 million or 10x basis) on the sale of qualified stock held for at least five years. OBBBA expanded the QSBS framework, making it more attractive for certain growth companies planning a future exit. However, QSBS is limited to original issuance stock in active C Corporations with gross assets under $50 million at issuance. It does not apply to SSTBs (specified service trades or businesses like consulting, law, accounting, or medical), and California does not fully conform to the federal QSBS exclusion. Run the numbers before assuming QSBS will save you more than annual S Corp tax savings.

Scenario 3: Full Profit Retention Below $250,000

If your business retains all profits for reinvestment and never distributes dividends, the C Corp avoids the second layer of dividend taxation. The flat 21% federal rate plus 8.84% California franchise tax (29.84% combined) can be lower than the top individual rate for high earners. But be careful: if accumulated retained earnings exceed $250,000 without a documented business purpose, the IRS can impose the accumulated earnings tax under IRC Section 531 at 20%. And the moment you distribute those retained profits, double taxation kicks in retroactively.

How to Switch From C Corp to S Corp in California: Eight Steps

If you are currently stuck in a C Corporation and want to capture the S Corp advantage, here is the precise process for California business owners in 2026. Our entity formation services team handles this conversion regularly and can guide you through each step.

Step 1: Verify S Corp Eligibility Under IRC Section 1361(b)

Your corporation must meet all five requirements: domestic corporation, no more than 100 shareholders, only individuals (plus certain trusts and estates) as shareholders, one class of stock only, and no nonresident alien shareholders. If any requirement fails, the S election is invalid.

Step 2: Evaluate Built-In Gains Tax Exposure

If your C Corp holds appreciated assets at the time of conversion, those assets may trigger Built-In Gains (BIG) tax under IRC Section 1374 if sold within five years of the S election. The BIG tax applies at the highest corporate rate (21% federal) on the built-in gain. Calculate your exposure before converting and plan asset dispositions accordingly.

Step 3: Calculate and Document Accumulated Earnings and Profits (AE&P)

Your C Corp’s AE&P under IRC Section 312 follows you into the S Corp. If not eliminated, it creates a permanent dividend tax trap under IRC Section 1368(c) distribution ordering rules. Calculate your AE&P balance precisely and develop a distribution or elimination strategy before converting.

Step 4: File IRS Form 2553 by March 15

Submit the completed Form 2553 to the IRS. All shareholders must consent by signing the form. File by March 15 for the election to be effective for the current tax year, or file at any time during the preceding tax year.

Step 5: File FTB Form 3560 With California

Submit the California S Corporation election notification to the Franchise Tax Board. This is a separate filing from the federal form and is mandatory for California to recognize your S Corp status. The California deadline aligns with the federal Form 2553 deadline.

Step 6: Set Up Payroll With Reasonable Salary

Register with the California Employment Development Department (EDD), establish payroll withholding, and set your owner salary at a defensible level based on industry compensation data. Keep documentation of comparable salary surveys in your files.

Step 7: Activate the AB 150 PTE Election

File the pass-through entity tax election to bypass the $40,000 SALT deduction cap. The election must be made annually and requires timely estimated payments. The 9.3% entity-level tax generates a federal deduction that would otherwise be lost under the SALT cap.

Step 8: Establish Dual Depreciation Schedules

California does not conform to federal bonus depreciation under R&TC Sections 17250 and 24356. You must maintain separate federal and California depreciation schedules for all depreciable assets. Failure to track both creates filing errors and potential FTB audit exposure.

OBBBA Permanent Changes That Affect the C Corporation S Corporation Decision

The One Big Beautiful Bill Act (OBBBA) made several formerly temporary provisions permanent, shifting the math on entity selection in favor of S Corporations:

- QBI deduction under IRC Section 199A: Now permanent. Previously set to expire after 2025. This locks in the 20% pass-through deduction exclusively for S Corp and partnership shareholders indefinitely.

- 100% bonus depreciation: Restored retroactively and made permanent. Applies to qualified property placed in service. California still does not conform (R&TC 17250/24356), requiring dual schedules.

- Section 179 expensing: Increased to $2.5 million with a $3.5 million phase-out threshold. Available to both C Corps and S Corps, but the S Corp combination with QBI and PTE elections makes the overall package stronger.

- SALT cap: Set at $40,000 (up from $10,000). The AB 150 PTE election allows S Corp owners to effectively bypass this cap, while C Corp shareholders cannot.

- Estate tax exemption: Increased to $15 million per person. This benefits business succession planning for both entity types but is particularly relevant for S Corp shares transferred through estate planning.

This information is current as of April 23, 2026. Tax laws change frequently. Verify updates with the IRS or FTB if reading this later.

What If You Already Filed as a C Corp This Year?

If you missed the March 15 deadline for the current tax year, you have options. Rev. Proc. 2013-30 allows late S Corp elections if you can demonstrate reasonable cause for the missed deadline and you intended to be treated as an S Corporation from the effective date. The relief window extends 3 years and 75 days from the intended effective date. You will need to file a completed Form 2553 with a reasonable cause statement attached.

If you do not qualify for late election relief, file Form 2553 before March 15 of next year so the election takes effect at the start of the following tax year. Every additional year in C Corp status costs you between $17,600 and $64,700 depending on your profit level, so this is not a decision to postpone.

IRS Audit Considerations for Entity Selection

The IRS Palantir SNAP AI system now cross-references entity classification filings with payroll records, Form 1120/1120-S submissions, and state tax filings. Here are the primary audit triggers related to the C Corporation S Corporation decision:

- S Corp salary below industry minimums: If your W-2 salary is significantly below comparable market rates, the AI flags the return for potential reclassification of distributions as wages.

- C Corp excessive accumulated earnings: Retained earnings exceeding $250,000 without documented business justification triggers accumulated earnings tax review under IRC Section 531.

- Mismatched federal and state entity elections: If your federal return shows S Corp status but California records show C Corp (or vice versa), expect a notice from the FTB within 12 to 18 months.

- Late S Corp elections without proper documentation: Rev. Proc. 2013-30 relief claims without adequate reasonable cause statements are flagged for review.

Key Takeaway: The IRS is not looking to penalize you for choosing S Corp status. It is looking for S Corp owners who abuse the salary-distribution split. Set a reasonable salary, document your rationale, and file correctly, and you have nothing to worry about.

Ready to Reduce Your Tax Bill?

KDA Inc. specializes in strategic tax planning for business owners, S Corps, LLCs, and high-net-worth individuals. Book a personalized consultation and walk away with a clear plan.

Frequently Asked Questions

Can an LLC be taxed as a C Corporation or S Corporation?

Yes. An LLC is a legal structure, not a tax classification. By default, a single-member LLC is taxed as a sole proprietorship and a multi-member LLC as a partnership. You can elect C Corp treatment by filing Form 8832 or S Corp treatment by filing Form 2553. Most California LLC owners earning above $60,000 in net profit benefit from the S Corp election.

Does California tax S Corporation income differently than the federal government?

California imposes a 1.5% franchise tax on S Corp net income (minimum $800 under R&TC Section 23153) plus a gross receipts fee under R&TC Section 17942 for LLCs taxed as S Corps with total income exceeding $250,000. California does not allow the QBI deduction at the state level. However, the AB 150 PTE election at 9.3% generates a federal deduction that partially offsets the state tax burden.

How long does the C Corp to S Corp conversion take?

The Form 2553 election can be processed by the IRS in 60 to 90 days. California FTB Form 3560 processing takes a similar timeframe. If you file by March 15, the S Corp election is effective January 1 of the current year. The full payroll setup, AB 150 election, and dual depreciation schedule configuration typically take an additional 30 to 45 days with a qualified tax team.

What happens to my C Corp net operating losses after converting to S Corp?

C Corporation NOLs do not carry over to the S Corp return. They remain suspended at the corporate level and can only offset BIG tax under IRC Section 1374 during the five-year recognition period. If your C Corp has significant NOLs, factor this into your conversion timeline and consider using them against C Corp income before electing S status.

Can I switch back from S Corp to C Corp if I change my mind?

Yes, but IRC Section 1362(g) imposes a five-year lockout before you can re-elect S Corp status after revocation. Given that the S Corp saves $17,600 to $64,700 per year, a five-year lockout represents $88,000 to $323,500 in potential lost savings. Revocation should only be considered if you have a signed VC term sheet, a genuine QSBS play, or a documented full-retention strategy.

Is the QBI deduction really permanent now?

Yes. OBBBA made the IRC Section 199A QBI deduction permanent. It was originally set to expire after December 31, 2025. The deduction is now available indefinitely for S Corp shareholders, partnership members, and sole proprietors. C Corp shareholders remain permanently excluded.

Book Your Entity Structure Review

If you are running a California business as a C Corporation and have never seen the five-layer tax comparison side by side, you are almost certainly overpaying by $17,000 to $65,000 every year. Our team will analyze your entity structure, model your S Corp savings, calculate your optimal salary-distribution split, and build a conversion roadmap that captures every available deduction. Click here to book your entity structure consultation now.

“The IRS does not reward you for picking the simpler entity. It rewards you for picking the right one.”