Quick Answer

Are most businesses S Corp or C Corp? The answer surprises most business owners: S Corporations outnumber C Corporations in the United States by a wide margin. According to the most recent IRS Statistics of Income data, roughly 5 million S Corps file returns annually compared to about 1.7 million C Corps. That means for every C Corp in America, there are nearly three S Corps. And in California, where state-level taxes punish C Corps harder than almost anywhere else, the S Corp advantage is even more dramatic. Yet thousands of California business owners still operate under the wrong entity structure, overpaying by $16,000 to $64,000 every single year because they never asked this one question.

This information is current as of April 21, 2026. Tax laws change frequently. Verify updates with the IRS or FTB if reading this later.

Why S Corps Dominate the Small Business Landscape

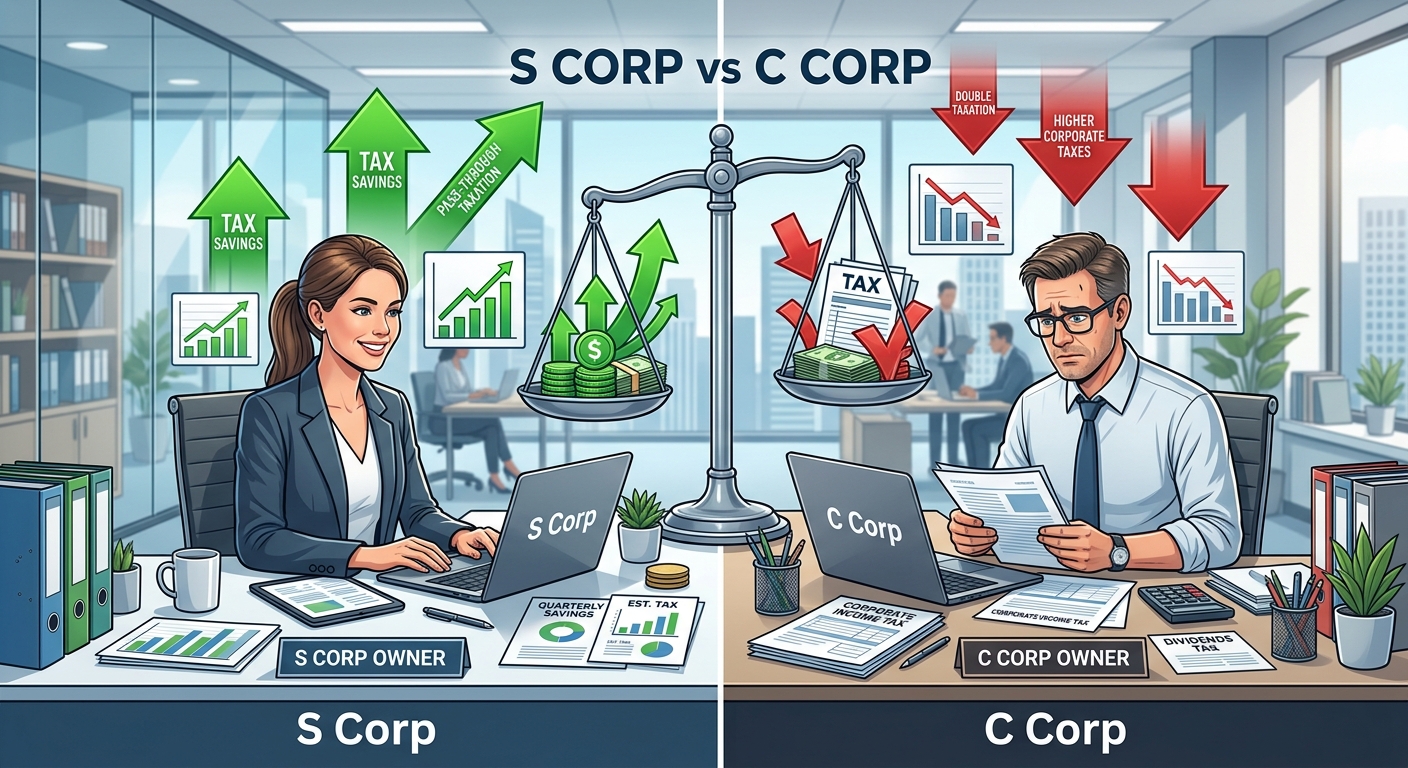

The IRS publishes entity classification data every year, and the trend has been clear for over two decades. S Corporations have been the most popular corporate entity type for small and mid-size businesses since the late 1990s. The reason is straightforward: pass-through taxation eliminates the double taxation problem that grinds away at C Corp profits.

When a C Corporation earns $200,000 in profit, the federal government takes 21% right off the top. That is $42,000 gone before the owner sees a dime. When the remaining $158,000 gets distributed as dividends, the owner pays another 15% to 23.8% in qualified dividend tax. The total federal tax burden on that $200,000 easily exceeds $65,000.

An S Corporation earning the same $200,000 pays zero entity-level federal tax. The profit flows through to the owner’s personal return, where it faces one layer of taxation. After the 20% Qualified Business Income deduction under IRC Section 199A, the effective rate drops further. The total federal tax burden on the same $200,000 typically lands between $28,000 and $35,000.

That gap of $30,000 or more is not theoretical. It is the reason nearly three out of every four corporate tax returns filed in the United States are S Corp returns. Business owners who understand the math choose S Corp status overwhelmingly. Those who remain as C Corps either have a specific strategic reason or, more commonly, they simply never evaluated the choice.

Key Takeaway: S Corps outnumber C Corps roughly 3 to 1 in the U.S. because pass-through taxation eliminates double taxation and saves the average owner $16,000 to $64,000 annually at profit levels between $100,000 and $350,000.

The Five Tax Layers That Separate S Corp Winners From C Corp Losers

Asking whether are most businesses S Corp or C Corp leads directly to the next question: why? The answer lives in five separate tax layers that compound against C Corp owners every single year. Many business owners discover these layers only after they have already locked themselves into the wrong structure.

Layer 1: Federal Entity Tax (21% vs 0%)

C Corps pay a flat 21% federal corporate tax on all profits before distributions. S Corps pay 0% at the entity level. On $200,000 in profit, that is $42,000 paid by the C Corp before the owner takes anything home.

Layer 2: Federal Dividend Double Taxation

After the C Corp pays its 21%, the remaining profit gets taxed again when distributed as dividends. Qualified dividends face a 15% to 23.8% rate depending on the owner’s income. On the $158,000 remaining after corporate tax, that is another $23,700 to $37,604 in tax. S Corp distributions from the Accumulated Adjustments Account (AAA) face zero additional tax because the income was already taxed on the owner’s personal return.

Layer 3: California Franchise Tax Differential

California taxes C Corps at 8.84% of net income. S Corps pay only 1.5%. On $200,000 in profit, the C Corp pays $17,680 to the Franchise Tax Board while the S Corp pays $3,000. That is a $14,680 gap at the state level alone. The $800 minimum franchise tax applies to both, but the percentage-based calculation creates the real damage at any meaningful profit level.

Layer 4: QBI Deduction Exclusivity Under IRC 199A

The Qualified Business Income deduction, made permanent by the One Big Beautiful Bill Act (OBBBA), allows S Corp owners to deduct up to 20% of their qualified business income. On $200,000 in S Corp profit, that is up to $40,000 deducted from taxable income, saving $8,800 to $14,800 depending on the owner’s marginal rate. C Corp shareholders get zero QBI deduction. Zero. This deduction is exclusive to pass-through entities, and OBBBA locked it in permanently.

Layer 5: AB 150 Pass-Through Entity Tax Election

California’s AB 150 allows S Corps to elect a pass-through entity tax at 9.3%, generating a dollar-for-dollar credit on the owner’s personal return. This effectively bypasses the $40,000 SALT deduction cap imposed by OBBBA. C Corps cannot make this election. For California S Corp owners in high tax brackets, this adds another $4,000 to $12,000 in annual savings that C Corps cannot access.

If you want to see exactly how these layers affect your specific profit level, run your numbers through this small business tax calculator to estimate the difference between entity structures.

Side-by-Side Tax Comparison: S Corp vs C Corp at Three Profit Levels

| Tax Layer | $100K Profit | $200K Profit | $350K Profit |

|---|---|---|---|

| C Corp Federal Tax (21%) | $21,000 | $42,000 | $73,500 |

| C Corp Dividend Tax (15-23.8%) | $11,850 | $23,700 | $52,267 |

| C Corp CA Franchise Tax (8.84%) | $8,840 | $17,680 | $30,940 |

| S Corp Total Tax (all layers) | $24,090 | $44,093 | $91,439 |

| Annual S Corp Advantage | $17,600 | $39,287 | $65,268 |

These numbers assume reasonable salary compliance, QBI deduction at full eligibility, and AB 150 election. The gap widens at every profit level because double taxation is multiplicative, not additive.

The Three Narrow Scenarios Where C Corp Actually Wins

Despite the overwhelming S Corp advantage, certain business situations genuinely favor C Corp status. Understanding these exceptions is critical because choosing the wrong structure in either direction costs real money. KDA’s entity formation services evaluate all five tax layers before recommending any structure.

Scenario 1: Venture Capital Funding

Most institutional investors require C Corp structure. VC firms need preferred stock classes, convertible notes, and unlimited shareholder capacity. S Corps are limited to 100 shareholders, one class of stock, and cannot have non-resident alien shareholders. If you are raising Series A or later institutional capital, C Corp is likely your path. The tax premium is the cost of accessing that capital.

Scenario 2: Qualified Small Business Stock (QSBS) Under IRC Section 1202

OBBBA expanded the QSBS benefit with tiered exclusions. C Corp shareholders who hold stock for five or more years can exclude up to $10 million in capital gains from the sale of that stock. This is an extraordinary benefit for founders building toward a large exit. S Corp shareholders cannot access QSBS because Section 1202 applies exclusively to C Corporation stock. If your five-year exit plan involves a sale above $10 million, the QSBS exclusion may outweigh the annual tax premium.

Scenario 3: Full Profit Retention Below $250,000

If a business retains all profits for reinvestment and never distributes them, the C Corp’s flat 21% rate can appear attractive. But this strategy has a hard ceiling: the accumulated earnings tax under IRC Section 531 imposes a 20% penalty on retained earnings the IRS considers unreasonable. For most businesses, retained earnings above $250,000 trigger scrutiny. This narrows the legitimate full-retention window significantly.

For a deeper look at how S Corp tax strategy works across all these scenarios, read our comprehensive S Corp tax guide for California business owners.

Key Takeaway: Only three narrow scenarios favor C Corp status. If you are not raising VC, pursuing QSBS, or retaining all profits below $250K, the S Corp advantage applies to your business.

Five Costliest Entity Selection Mistakes California Owners Make

Understanding whether are most businesses S Corp or C Corp is the starting point. Avoiding these five mistakes is where the real money gets saved or lost.

Mistake 1: Defaulting to C Corp Without Evaluation ($16,000-$65,000/Year)

When you incorporate without filing Form 2553, the IRS classifies your corporation as a C Corp by default. Many business owners incorporate through LegalZoom or similar services, never realize they are a C Corp, and overpay for years. The fix is filing Form 2553 to elect S Corp status, but the deadline is March 15 of the tax year. Miss it, and you wait another full year or file under Rev. Proc. 2013-30 for late election relief.

Mistake 2: Setting an Unreasonable Salary ($12,000-$25,000 Exposure)

S Corp owners must pay themselves a “reasonable salary” before taking distributions. The landmark case Watson v. Commissioner established that the IRS takes this seriously. Pay yourself too little, and the IRS reclassifies distributions as wages, adding back all self-employment taxes plus penalties. Pay yourself too much, and you eliminate the distribution tax savings that make S Corp worthwhile. The sweet spot depends on your industry, geography, and experience level.

Mistake 3: Ignoring California’s Bonus Depreciation Nonconformity ($3,000-$18,000/Year)

OBBBA restored 100% bonus depreciation at the federal level. California does not conform. Under Revenue and Taxation Code Sections 17250 and 24356, California requires its own depreciation schedule. Every S Corp and C Corp in California must maintain dual depreciation books. Owners who take the federal deduction without adjusting their California return face FTB notices, penalties, and interest.

Mistake 4: Missing the AB 150 PTE Election Deadline ($4,000-$12,000/Year)

California’s pass-through entity tax election under AB 150 is one of the most powerful SALT cap workarounds available to S Corp owners. But the election must be made annually, and the deadline is the original due date of the return. Miss it by one day, and you lose the entire benefit for that tax year. No extensions. No late filings. This election is exclusively available to pass-through entities, making it another reason the S Corp structure dominates.

Mistake 5: Failing to Track Shareholder Basis on Form 7203 ($5,000-$35,000 Exposure)

The IRS now requires S Corp shareholders to file Form 7203 every year to track stock and debt basis. If your basis drops to zero, you cannot deduct losses. If you take distributions exceeding your basis, those distributions become taxable capital gains. Many owners skip this form entirely, creating a ticking time bomb that detonates during an audit or when they sell the business.

Pro Tip: The IRS Palantir SNAP AI system now cross-references S Corp salary levels against industry benchmarks, 1099 filings, and distribution patterns. Unreasonable salary discrepancies are flagged automatically, not by human reviewers. The technology has made this the single most common S Corp audit trigger in 2026.

OBBBA Permanent Changes That Locked In the S Corp Advantage

The One Big Beautiful Bill Act, signed into law in 2025, made several temporary provisions permanent. These changes cemented the S Corp’s structural advantage over C Corps for the foreseeable future.

QBI Deduction Made Permanent

The 20% Qualified Business Income deduction under IRC Section 199A was set to expire after 2025. OBBBA made it permanent. S Corp owners earning $200,000 in qualified business income deduct $40,000 every year, indefinitely. C Corp owners get nothing. This single change is worth $8,800 to $14,800 per year depending on marginal tax rate.

100% Bonus Depreciation Restored

Bonus depreciation had phased down to 60% in 2024. OBBBA restored it to 100% retroactively and permanently. Both S Corps and C Corps benefit from this provision at the federal level, but remember: California does not conform. S Corp owners who also hold real estate or significant equipment must maintain dual depreciation schedules and may benefit from separate cost segregation analysis.

Section 179 Limit Increased to $2.5 Million

The Section 179 expensing limit jumped to $2.5 million under OBBBA, with a phase-out threshold of $4 million. This allows both entity types to immediately expense qualifying asset purchases, but S Corp owners stack this benefit on top of QBI and AB 150 advantages that C Corps cannot access.

SALT Cap Set at $40,000

OBBBA raised the state and local tax deduction cap from $10,000 to $40,000. While this helps all taxpayers, S Corp owners bypass the cap entirely through the AB 150 PTE election. C Corp owners have no equivalent workaround. The PTE election turns what could be a $40,000 ceiling into an unlimited state tax deduction through the entity-level payment structure.

Estate Exemption Raised to $15 Million

While not directly related to entity taxation, the $15 million estate exemption makes succession planning easier for S Corp owners. Transferring S Corp shares to family members or trusts becomes more tax-efficient with the higher exemption threshold, reinforcing the S Corp’s flexibility for multi-generational business planning.

KDA Case Study: Sacramento Restaurant Group Owner Saves $42,800 With Entity Restructure

Marcus operated three restaurant locations in the Sacramento area through a C Corporation his attorney had set up in 2019. His annual profit across all three locations was $240,000. He had never questioned his entity structure because his attorney told him “corporations protect you” without specifying which type of corporation made tax sense.

When Marcus came to KDA, his annual tax bill told the story. His C Corp was paying $21,216 in California franchise tax at 8.84%, $50,400 in federal corporate tax, and he was paying another $26,460 in qualified dividend tax when he distributed the remaining profit. His total tax burden exceeded $98,000 on $240,000 in profit.

KDA evaluated Marcus’s eligibility for S Corp status and confirmed he met all five requirements under IRC Section 1361(b). We filed Form 2553 and California FTB Form 3560, established a reasonable salary of $85,000 based on restaurant management industry benchmarks, set up payroll through a compliant provider, activated the AB 150 PTE election, built dual depreciation schedules for his kitchen equipment under both federal and California rules, and opened a Solo 401(k) with $23,500 in annual contributions plus employer profit-sharing.

Marcus’s first-year tax savings totaled $42,800. His KDA engagement cost $5,800. That is a 7.4x first-year return on investment. Over five years, projected savings reach $214,000 at current profit levels, not including additional retirement account benefits.

Ready to see how we can help you? Explore more success stories on our case studies page to discover proven strategies that have saved our clients thousands in taxes.

How to Convert From C Corp to S Corp in California: 8-Step Process

If you are currently operating as a C Corp and the analysis shows S Corp status is the right move, here is the exact process KDA follows for California conversions.

Step 1: Verify IRC 1361(b) Eligibility

Confirm your corporation meets all five requirements: domestic corporation, 100 or fewer shareholders, only individuals/estates/certain trusts as shareholders, one class of stock, and no non-resident alien shareholders. If any requirement fails, S Corp election is unavailable.

Step 2: Evaluate Built-In Gains Tax Exposure

Under IRC Section 1374, any appreciated assets held by the C Corp at the time of conversion may trigger Built-In Gains (BIG) tax if sold within five years. Calculate the fair market value of all assets and compare to tax basis. If significant appreciation exists, plan asset dispositions around the five-year recognition window.

Step 3: Calculate and Plan AE&P Elimination

Accumulated Earnings and Profits (AE&P) from C Corp years follow the entity into S Corp status. Under IRC Section 1368(c), distributions exceeding the AAA are treated as dividends to the extent of AE&P. Plan a controlled distribution schedule or use the AAA bypass election under IRC 1368(e)(3) to eliminate AE&P systematically.

Step 4: File IRS Form 2553

Submit Form 2553 by March 15 of the tax year you want the election to take effect. All shareholders must consent. Late elections may qualify under Rev. Proc. 2013-30 if you meet the reasonable cause standard.

Step 5: File California FTB Form 3560

California requires separate S Corp election notification. File Form 3560 with the Franchise Tax Board. This is a separate filing from the IRS form, and missing it creates compliance gaps that generate FTB notices.

Step 6: Establish Payroll With Reasonable Salary

Set up payroll immediately upon S Corp election. Research industry salary benchmarks for your role, geography, and experience. Register with California EDD for state employment taxes. The salary must be established before any distributions are taken.

Step 7: Activate AB 150 PTE Election

Make the pass-through entity tax election on or before the original due date of your S Corp return (March 15 for calendar-year filers). This election must be renewed annually. The 9.3% entity-level tax generates a dollar-for-dollar credit on your personal return, bypassing the SALT cap.

Step 8: Build Dual Depreciation Schedules

Federal 100% bonus depreciation under OBBBA does not apply in California under R&TC Sections 17250 and 24356. Maintain separate federal and California depreciation schedules for all qualifying assets. This dual tracking is mandatory and must be reconciled annually on your California return.

What If You Just Started Your Business?

New business owners face this question at the very beginning. If you are forming a new entity and your projected net profit exceeds $60,000 annually, S Corp election from day one typically makes financial sense. The administrative costs of running payroll and filing Form 1120-S are real, but they are dwarfed by the self-employment tax savings once profit crosses the $60,000 threshold.

At $80,000 in net profit, the S Corp election saves approximately $4,960 per year in Social Security tax alone on distributions above a reasonable salary. At $150,000, the combined savings from self-employment tax reduction, QBI deduction, and AB 150 election reach $18,000 or more. At $250,000, you are looking at over $35,000 in annual savings.

The breakeven analysis is simple: if the $2,000 to $4,000 annual cost of payroll processing, additional tax return preparation, and compliance is less than the tax savings, elect S Corp status. For the vast majority of profitable businesses in California, that crossover happens between $50,000 and $70,000 in annual net profit.

Will Choosing S Corp Status Trigger an Audit?

This fear keeps some business owners locked in C Corp status unnecessarily. The reality is that IRS audit rates for S Corporations are low. According to IRS enforcement data, S Corp audit rates hover around 0.15% to 0.30% annually. The key audit triggers are not the S Corp election itself but rather specific compliance failures within the S Corp structure.

The top S Corp audit triggers in 2026 include:

- Officer compensation reported as zero on Form 1120-S while significant distributions were taken

- Salary-to-distribution ratios that deviate dramatically from industry norms

- Failure to file Form 7203 for shareholder basis tracking

- Discrepancies between 1099 income reported to the IRS and amounts on the S Corp return

- Large deductions without proper documentation, particularly vehicle and home office expenses

The IRS Palantir SNAP AI system, deployed across enforcement divisions since 2025, automatically cross-references these data points. Staying compliant with reasonable salary requirements and proper documentation makes S Corp status one of the lowest audit-risk entity structures available.

Ready to Reduce Your Tax Bill?

KDA Inc. specializes in strategic tax planning for business owners, S Corps, LLCs, and high-net-worth individuals. Book a personalized consultation and walk away with a clear plan.

Frequently Asked Questions

Can an LLC Be Taxed as an S Corp?

Yes. An LLC can elect S Corp taxation by filing Form 2553 with the IRS and Form 3560 with the California FTB. The LLC retains its legal liability protection while being taxed as an S Corp. This is the most common structure for small businesses in California because it combines the operational flexibility of an LLC with the tax efficiency of an S Corp.

What Happens If I Revoke My S Corp Election?

Revoking S Corp status converts your entity to a C Corp. Under IRC Section 1362(g), you cannot re-elect S Corp status for five years without IRS approval through a Private Letter Ruling, which costs approximately $15,300. The five-year lockout makes revocation a decision that should only be made with comprehensive five-year tax projections.

Does California Conform to the Federal QBI Deduction?

No. California does not allow the QBI deduction on your state return. The deduction only reduces your federal taxable income. However, the AB 150 PTE election provides a different mechanism for reducing California tax burden on S Corp income, partially compensating for the state-level QBI exclusion.

How Many Shareholders Can an S Corp Have?

S Corps are limited to 100 shareholders under IRC Section 1361(b)(1)(A). Family members can elect to be treated as a single shareholder under IRC 1361(c)(1), which extends the practical limit for family-owned businesses. If your shareholder count exceeds 100, S Corp status is not available.

Is the S Corp Advantage Permanent After OBBBA?

The core advantages are now permanent. The QBI deduction, 100% bonus depreciation, and the $2.5 million Section 179 limit were all made permanent by OBBBA. The C Corp rate remains at 21%. Unless Congress passes new legislation changing these provisions, the S Corp structural advantage is locked in for the foreseeable future.

What Is the Minimum Income to Justify S Corp Election?

Most tax professionals recommend S Corp election when net business profit consistently exceeds $50,000 to $60,000 annually. Below that level, the administrative costs of payroll, additional tax filings, and compliance management may offset the tax savings. Above $60,000, the savings typically accelerate rapidly, making S Corp election a clear financial win.

“The IRS is not hiding the S Corp election from you. It is sitting right there on Form 2553. The question is whether you will file it before another $40,000 walks out the door.”

Book Your Entity Structure Strategy Session

If you are operating as a C Corp, an LLC taxed as a sole proprietor, or you have never evaluated which entity structure saves you the most, it is time to get clear answers backed by real numbers. Book a personalized consultation with our strategy team and walk away knowing exactly how much you are overpaying and what to do about it. Click here to book your consultation now.