Quick Answer

Yes, can a sub S corp own a C corp is one of the most misunderstood corporate ownership questions in tax law. An S Corporation can absolutely own shares of a C Corporation, and it can even own 100% of a C Corp as a wholly owned subsidiary. But the tax consequences of getting this structure wrong cost California business owners an average of $47,000 over five years through double taxation, missed elections, and compliance failures they never saw coming.

This information is current as of April 19, 2026. Tax laws change frequently. Verify updates with the IRS or FTB if reading this later.

Why S Corp Owners Ask About C Corp Subsidiaries in the First Place

Most S Corporation owners do not wake up wanting to own a C Corp. The question usually surfaces when one of three things happens: they want to acquire another business, they need to isolate a high-risk venture from their core operations, or they are exploring venture capital funding that requires a C Corp share structure. Each of these scenarios is legitimate, but each carries a different set of IRS rules that can either protect your tax position or destroy it.

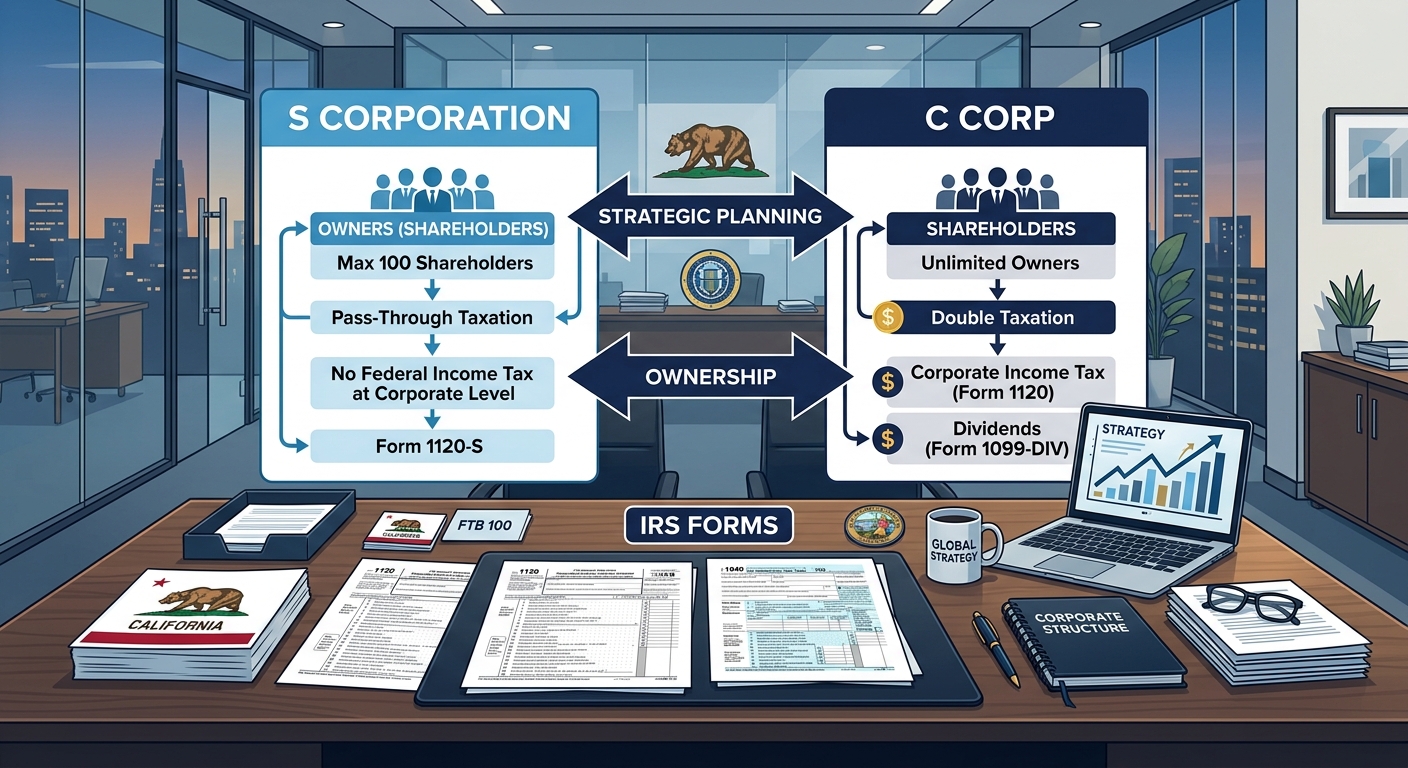

The IRS allows an S Corp to own stock in a C Corporation without any special restrictions. Under IRS Publication 542, a C Corp can have any type of shareholder, including another corporation. The critical distinction is the reverse: a C Corp cannot own shares of an S Corp, because IRC Section 1361(b)(1)(B) restricts S Corp shareholders to individuals, certain trusts, and estates. Corporations are explicitly excluded from that list.

So the ownership arrow only flows one direction without jeopardizing your S election. An S Corp can own part or all of a C Corp. A C Corp cannot own any part of an S Corp. Mixing these up triggers an involuntary termination of your S election under IRC Section 1362(d)(2), and that mistake costs far more than the tax savings the structure was supposed to create.

The Two Legal Ways an S Corp Can Own a C Corp

Partial Stock Ownership

An S Corp can purchase any percentage of a C Corporation’s stock, from 1% to 99%, without any special IRS election. The S Corp simply holds the C Corp stock as an investment asset on its balance sheet. Dividends received from the C Corp flow into the S Corp’s income, pass through to the S Corp shareholders on their K-1s, and get taxed at the shareholder’s individual rate.

Here is where the math matters. If the C Corp earns $200,000 in profit, it pays 21% federal corporate tax, leaving $158,000. When that $158,000 is distributed as a dividend to the S Corp, the S Corp passes it through to the shareholder, who pays qualified dividend rates of up to 23.8% (including the 3.8% Net Investment Income Tax). The combined effective tax rate on that $200,000 of profit hits roughly 39.8% before California even enters the picture.

Many business owners underestimate this double-taxation layer. They see the 21% C Corp rate and assume it is the total cost. It never is.

100% Ownership With or Without QSub Election

When an S Corp owns 100% of a C Corp, the owner faces a choice: keep the subsidiary as a standalone C Corp, or elect Qualified Subchapter S Subsidiary (QSub) status under IRC Section 1361(b)(3). This election changes everything.

Without the QSub election, the C Corp remains a separate taxpaying entity. It files its own Form 1120, pays its own 21% federal tax, and any distributions to the parent S Corp are taxable dividends. In California, the C Corp also pays the 8.84% franchise tax under Revenue and Taxation Code Section 23151, and the S Corp parent pays 1.5% on its own net income.

With the QSub election, the C Corp is treated as if it does not exist for federal tax purposes. All of its income, deductions, credits, and losses flow directly into the parent S Corp’s Form 1120-S. The subsidiary stops filing its own return. For a complete breakdown of advanced S Corp structures, see our comprehensive S Corp tax strategy guide.

Key Takeaway: The QSub election eliminates double taxation entirely, but it also converts the C Corp into what is essentially a division of the S Corp, which means you lose the liability protection between the two entities for tax purposes.

The $47,000 Ownership Trap: Five Costliest Mistakes

Mistake 1: Forgetting the Built-In Gains Tax on QSub Conversion

When you convert a C Corp into a QSub, any appreciated assets inside the C Corp become subject to the Built-In Gains (BIG) tax under IRC Section 1374. If the C Corp holds real estate worth $500,000 with a basis of $200,000, that $300,000 of built-in gain faces a 21% corporate-level tax if the asset is sold within the five-year recognition period. That is $63,000 in tax that would not have existed if you had simply kept the C Corp as a separate entity.

California adds its own BIG tax at the 1.5% S Corp rate, plus it does not conform to the federal five-year recognition period in all cases. Check FTB guidance under R&TC Section 23802 before assuming your recognition window matches federal rules.

Mistake 2: Triggering Passive Investment Income Tax

If the S Corp receives dividends from the C Corp subsidiary (without making a QSub election), those dividends count as passive investment income under IRC Section 1375. When passive investment income exceeds 25% of the S Corp’s gross receipts, and the S Corp has accumulated earnings and profits (AE&P) from a prior C Corp history, the S Corp faces a corporate-level tax on the excess passive income.

Worse, if passive investment income exceeds 25% for three consecutive years while AE&P exists, the S election terminates automatically under IRC Section 1362(d)(3). This is the silent killer of multi-entity structures. The owner does not receive a warning letter. The election simply dies, and the IRS retroactively reclassifies the entity as a C Corp.

Mistake 3: Missing the QSub Election Deadline

Form 8869 (Qualified Subchapter S Subsidiary Election) must be filed within a specific window. If you acquire 100% of the C Corp stock on June 1, the QSub election can be effective as early as that date or up to 75 days prior. Filing late means the subsidiary remains a C Corp for the entire year, generating double taxation you cannot undo retroactively without requesting a Private Letter Ruling at a cost of roughly $15,300.

Mistake 4: California Dual-Filing Failure

California does not automatically recognize the federal QSub election. You must separately notify the FTB and ensure the subsidiary’s California tax obligations are properly handled. The C Corp subsidiary may still owe the $800 minimum franchise tax under R&TC Section 23153 even after the QSub election takes effect for federal purposes. Missing this creates FTB penalties and interest that compound monthly.

Additionally, California does not conform to federal bonus depreciation under R&TC Sections 17250 and 24356. This means the S Corp must maintain dual depreciation schedules for every asset the C Corp subsidiary held at conversion. If you want to estimate how your overall business profit would be taxed under different structures, run the numbers through this small business tax calculator to see the difference.

Mistake 5: Ignoring the AE&P Contamination

When a C Corp becomes a QSub, its accumulated earnings and profits do not disappear. Those AE&P transfer into the parent S Corp under IRC Section 1371. If the S Corp then makes distributions exceeding its Accumulated Adjustments Account (AAA), the excess distributions are treated as dividends to the extent of AE&P under IRC Section 1368(c). This is the same distribution ordering trap that has cost California S Corp owners tens of thousands of dollars in unexpected dividend taxes.

Pro Tip: Before converting any C Corp subsidiary to QSub status, calculate the AE&P balance precisely. Consider distributing all AE&P as qualifying dividends under IRC Section 1371(e) within the post-termination transition period, or elect the AAA bypass under IRC Section 1368(e)(3) to manage distribution ordering strategically.

Can a Sub S Corp Own a C Corp: Side-by-Side Tax Comparison

Below is what happens to $200,000 of subsidiary profit under three structures, assuming the S Corp shareholder is a California resident in the 37% federal bracket:

| Tax Layer | C Corp Subsidiary (No QSub) | QSub Election | Separate S Corp (No Parent) |

|---|---|---|---|

| Federal Entity Tax | $42,000 (21%) | $0 | $0 |

| CA Franchise Tax (Entity) | $17,680 (8.84%) | $0 | $3,000 (1.5%) |

| Federal Individual Tax | $37,620 (23.8% on $158K dividend) | $74,000 (37%) | $74,000 (37%) |

| QBI Deduction Benefit | $0 (dividends ineligible) | -$14,800 (20% of $74K) | -$14,800 (20% of $74K) |

| CA State Income Tax | $20,987 (13.3% on $158K) | $26,600 (13.3%) | $26,600 (13.3%) |

| AB 150 PTE Election | Not available for C Corp layer | -$7,800 (9.3% credit) | -$7,800 (9.3% credit) |

| Total Tax Burden | $118,287 (59.1%) | $78,000 (39.0%) | $81,000 (40.5%) |

| Annual Savings vs C Corp Sub | Baseline | $40,287 | $37,287 |

The QSub election saves $40,287 per year at $200,000 profit. Over five years, that compounds to $201,435 in tax savings, not counting the administrative cost reduction from eliminating a separate corporate return.

When Keeping the C Corp Subsidiary Actually Makes Sense

Not every situation calls for the QSub election. There are three narrow scenarios where maintaining the C Corp as a separate entity is the smarter play.

Scenario 1: Venture Capital or Institutional Investment

If the subsidiary is pursuing outside investment, VCs require preferred stock classes, convertible notes, and multiple share classes. S Corps cannot issue preferred stock, and QSubs inherit those restrictions. Keeping the subsidiary as a C Corp preserves the ability to raise capital through equity rounds.

Scenario 2: QSBS Section 1202 Exclusion

If the C Corp subsidiary qualifies as a Qualified Small Business Stock issuer under IRC Section 1202, the first $10 million in capital gains (or 10x the adjusted basis, whichever is greater) can be excluded from federal tax entirely. This benefit is only available to C Corps. Converting to a QSub permanently destroys QSBS eligibility.

Scenario 3: Full Profit Retention Below $250,000

If the subsidiary needs to retain all profits for growth and reinvestment, the 21% flat C Corp rate may be lower than the S Corp pass-through rate for high-income shareholders. However, this advantage disappears once retained earnings exceed $250,000 and trigger the accumulated earnings tax under IRC Section 531, which adds a 20% penalty tax on top of the 21% corporate rate.

KDA Case Study: Sacramento Tech Firm Owner Saves $47,200 With QSub Election

Marcus, a Sacramento-based software development firm owner, acquired a competing C Corporation for $380,000 in early 2025. His S Corp generated $280,000 in annual profit, and the acquired C Corp was earning $165,000. His previous CPA told him to keep the entities separate, which meant he was paying double taxation on the C Corp income: 21% federal corporate tax, 8.84% California franchise tax, and then qualified dividend rates when distributions flowed to the parent S Corp.

In his first year of separate filing, Marcus paid $118,400 in total taxes across both entities. When he came to KDA, we ran the numbers on a QSub conversion. We evaluated the BIG tax exposure on $92,000 of built-in gains in the C Corp’s assets, determined that a strategic five-year hold on those appreciated assets would avoid the 21% BIG tax entirely, and filed Form 8869 within the required window.

We also cleaned up $48,000 in AE&P from the acquired C Corp by distributing qualifying dividends under IRC Section 1371(e) during the conversion window, set up AB 150 PTE election for the combined entity, and established dual depreciation schedules for California’s bonus depreciation nonconformity. KDA’s fee was $5,800 for the full conversion and first-year compliance setup.

Result: Marcus saved $47,200 in year one, representing an 8.1x return on his investment. Over five years, projected savings reach $224,000, assuming consistent revenue and strategic BIG tax avoidance on the appreciated assets.

Ready to see how we can help you? Explore more success stories on our case studies page to discover proven strategies that have saved our clients thousands in taxes.

The 8-Step Process for an S Corp to Properly Own a C Corp in California

- Evaluate BIG Tax Exposure – Calculate the fair market value of all C Corp assets minus adjusted basis. If built-in gains exceed $50,000, develop a five-year disposition strategy to minimize IRC Section 1374 tax.

- Calculate AE&P Balance – Determine the C Corp’s accumulated earnings and profits using IRC Section 312 rules. This balance follows the entity into the S Corp and affects distribution ordering for years.

- Decide: QSub or Standalone – Run side-by-side projections for at least five years. Factor in BIG tax, AE&P cleanup costs, California franchise tax differential, and QBI deduction eligibility.

- File Form 8869 (If Electing QSub) – Submit to the IRS within 75 days of the effective date. Include all required shareholder consents and EIN information.

- Notify California FTB Separately – File the required California forms to notify the FTB of the QSub election. Ensure the C Corp’s California obligations (franchise tax, gross receipts fee) are properly terminated or adjusted.

- Set Up Payroll for Combined Entity – If the QSub had its own employees, their payroll now runs through the parent S Corp. Update EIN records, W-2 reporting, and California DE-9 filings accordingly. Our entity formation services handle this transition seamlessly.

- Establish Dual Depreciation Schedules – California does not conform to federal bonus depreciation under R&TC Sections 17250 and 24356. Every asset transferred from the C Corp must be tracked on both federal and California depreciation schedules. The California Section 179 cap remains at $25,000 versus the federal $2.5 million limit under OBBBA.

- Activate AB 150 PTE Election – If you have not already elected into California’s Pass-Through Entity tax under AB 150, do so immediately. This provides a workaround for the $40,000 SALT cap by allowing the entity to pay state tax and pass through the credit to shareholders.

OBBBA Permanent Changes That Affect S Corp Subsidiary Structures in 2026

The One Big Beautiful Bill Act made several tax provisions permanent that directly impact how an S Corp interacts with a C Corp subsidiary:

- QBI Deduction (IRC Section 199A) – Now permanent. S Corp shareholders receive a 20% deduction on qualified business income. C Corp subsidiaries generate dividends, not QBI, so income retained in C Corp form loses this deduction permanently.

- 100% Bonus Depreciation – Now permanent at the federal level. California still does not conform under R&TC 17250/24356. QSub conversion allows the parent S Corp to claim federal bonus depreciation on inherited assets, but California requires straight-line or MACRS without bonus.

- $2.5 Million Section 179 Limit – Now permanent. This benefits QSub conversions because the combined entity can expense up to $2.5 million in qualifying assets (federal only; California caps at $25,000).

- $40,000 SALT Cap – Now permanent at $40,000. The AB 150 PTE election becomes even more critical for S Corp owners with combined income from multiple entities. C Corp subsidiaries cannot use the PTE election.

- $15 Million Estate Exemption – Now permanent. For business owners holding S Corp and C Corp structures as part of estate planning, the higher exemption provides more flexibility in transferring ownership interests.

What Happens If You Get the Ownership Structure Wrong?

The IRS uses Palantir SNAP AI to cross-reference Form 1120-S filings, Form 1120 filings, Form 8869 QSub elections, and shareholder K-1 information. If your S Corp reports dividend income from a C Corp but no corresponding Form 1120 is filed by the subsidiary, the system flags the discrepancy automatically.

Similarly, if you file a QSub election but the subsidiary continues filing its own Form 1120, the IRS treats this as a duplicate filing that triggers an examination. California’s FTB runs its own matching program and will assess the $800 minimum franchise tax on any entity it believes should still be filing separately.

Red Flag Alert: If you acquired a C Corp and made the QSub election but failed to notify the FTB, you could face retroactive franchise tax assessments going back to the acquisition date, plus penalties and interest at 1% per month. This single oversight has cost California business owners $8,000 to $24,000 in back taxes and penalties.

Ready to Reduce Your Tax Bill?

KDA Inc. specializes in strategic tax planning for business owners, S Corps, LLCs, and high-net-worth individuals. Book a personalized consultation and walk away with a clear plan.

Frequently Asked Questions

Can a sub S corp own a C corp without making any special election?

Yes. An S Corp can own any amount of C Corp stock without any IRS election. The QSub election under IRC Section 1361(b)(3) is only required if you want the C Corp to be disregarded for tax purposes. Without the election, the C Corp remains a separate taxpaying entity subject to double taxation.

Does owning a C Corp affect my S Corp election?

Owning C Corp stock does not, by itself, threaten your S election. However, if the C Corp pays dividends to the S Corp and those dividends push passive investment income above 25% of gross receipts for three consecutive years while the S Corp has AE&P, the S election terminates automatically under IRC Section 1362(d)(3).

Can I convert the C Corp subsidiary back after making the QSub election?

Revoking a QSub election is possible, but the entity becomes a C Corp again, and you cannot re-elect QSub status for five years under IRC Section 1361(b)(3)(D) without IRS consent. Think carefully before making the initial election, because reversing it is expensive and time-restricted.

What is the BIG tax, and how long does it last?

The Built-In Gains tax under IRC Section 1374 imposes a corporate-level tax (21%) on any gain recognized from assets that had built-in appreciation at the time of the S election or QSub conversion. The recognition period is five years from the conversion date. If you hold the appreciated assets for the full five years, the BIG tax no longer applies.

Does California conform to the federal QSub rules?

California generally follows the federal QSub provisions, but with important differences. The FTB requires separate notification, and the subsidiary may still owe the $800 minimum franchise tax. California also does not conform to federal bonus depreciation, which creates dual-tracking requirements for every depreciated asset the QSub held at conversion.

Will this trigger an IRS audit?

Multi-entity structures receive higher audit scrutiny. The IRS Palantir SNAP system specifically flags S Corps with C Corp subsidiaries for consistency checks. Proper documentation, timely elections, and accurate AE&P tracking significantly reduce audit risk. Sloppy record-keeping or missed filings dramatically increase it.

Book Your Multi-Entity Tax Strategy Session

If you own an S Corp and are considering acquiring a C Corp, converting a subsidiary, or restructuring your multi-entity tax setup, the difference between the right and wrong structure is $40,000 or more per year. Stop guessing and get a personalized analysis from our strategy team. We will map your specific numbers, evaluate your BIG tax exposure, and build a five-year projection that keeps more money in your pocket. Click here to book your consultation now.