Most California S Corp Owners Think Acquiring a C Corp Is Simple. The IRS Disagrees by About $47,000.

You finally found the perfect acquisition target. The revenue fits, the client list is gold, and the price is right. There is just one problem: your company is an S Corporation, and the target is a C Corporation. Before you sign a single document, you need to understand that the question can an S Corp acquire a C Corp is not a yes-or-no question. It is a five-layer tax trap that has cost California business owners anywhere from $12,000 to $47,000 in unexpected federal and state taxes, penalties, and blown elections. The mechanics of this acquisition determine whether you walk away with a strategic asset or a tax liability that follows you for years.

Quick Answer

Yes, an S Corporation can legally acquire a C Corporation through either a stock purchase or an asset purchase. However, the method you choose triggers dramatically different tax consequences. A stock purchase turns the C Corp into a subsidiary (which S Corps generally cannot hold unless they make a Qualified Subchapter S Subsidiary election under IRC Section 1361(b)(3)), while an asset purchase lets you cherry-pick what you want but forces the C Corp to recognize gains on everything sold. Neither path is simple, and both require careful California-specific planning to avoid six-figure tax surprises.

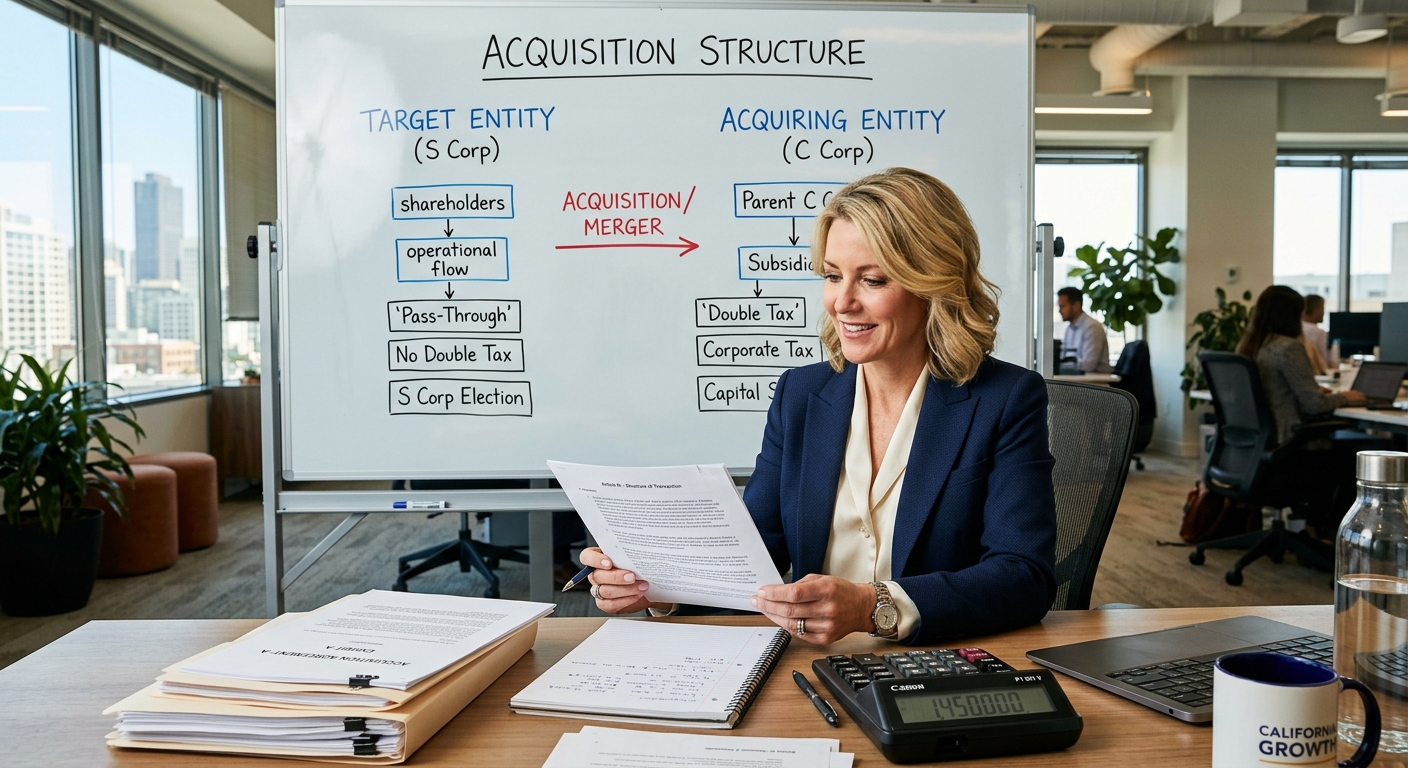

Can an S Corp Acquire a C Corp Through a Stock Purchase?

When an S Corporation buys 100% of a C Corporation’s stock, the C Corp does not disappear. It becomes a subsidiary of the S Corp. And here is where the first trap springs open.

The S Corp Subsidiary Rule Under IRC Section 1361(b)(1)(B)

S Corporations can only have certain types of shareholders. Under IRC Section 1361(b)(1)(B), an S Corp generally cannot own stock in a C Corporation without jeopardizing the flow-through tax treatment that makes S Corps valuable. But there is a critical exception: if the S Corp acquires 100% of the C Corp stock, it can elect to treat the acquired company as a Qualified Subchapter S Subsidiary, commonly called a QSub, under IRC Section 1361(b)(3).

A QSub election effectively dissolves the C Corp for federal tax purposes. The subsidiary’s assets, liabilities, income, and deductions all roll up into the parent S Corp’s tax return. Sounds clean. But the IRS treats this deemed liquidation as if the C Corp actually distributed all its assets to the S Corp, which triggers several potential tax events.

The Built-In Gains Tax Trap

When a C Corp converts to S Corp status (or is absorbed via QSub election), IRC Section 1374 imposes a Built-In Gains (BIG) tax on any appreciation that existed at the time of conversion. The BIG tax applies at the highest corporate rate of 21% on any built-in gains recognized during the five-year recognition period following the conversion.

Here is how this hits your wallet. Say the C Corp you are acquiring holds assets with a fair market value of $500,000 but a tax basis of $200,000. That $300,000 in built-in gains is subject to the 21% BIG tax if those assets are sold or deemed sold within five years. That is $63,000 in unexpected federal tax before California even enters the picture.

Many business owners pursuing acquisitions never model the BIG tax exposure. They see the deal economics, skip the tax layer, and discover a five-figure surprise when their CPA prepares the first post-acquisition return.

Accumulated Earnings and Profits Contamination

C Corporations accumulate earnings and profits (AE&P) over their lifetime. When an S Corp acquires a C Corp and makes a QSub election, those accumulated earnings do not vanish. They follow the assets into the S Corp. Under IRC Section 1368(c), any distributions from the S Corp that exceed its Accumulated Adjustments Account (AAA) get pulled from this inherited AE&P pool and taxed as dividends at up to 23.8% (including the 3.8% Net Investment Income Tax).

On a $200,000 distribution, if $80,000 comes from inherited AE&P, the shareholder faces $19,040 in dividend taxes they would never have owed if the S Corp had clean books. For a deeper dive into S Corp strategy nuances, read our comprehensive California S Corp tax strategy guide.

Can an S Corp Acquire a C Corp Through an Asset Purchase?

The alternative to buying stock is buying assets directly from the C Corp. This gives the S Corp more control over what it acquires (and what liabilities it leaves behind), but it creates a different set of tax consequences.

The C Corp Recognizes Gain on Asset Sales

When the C Corp sells its assets to your S Corp, it recognizes gain on each asset sold. That gain is taxed at the 21% federal corporate rate inside the C Corp. Then, when the C Corp distributes the remaining cash to its shareholders in liquidation, those shareholders pay capital gains tax on the difference between what they receive and their stock basis.

This is the classic double-taxation problem. If you want to run those numbers for your specific scenario, plug your figures into this small business tax calculator to see how entity structure affects your total tax bill.

Here is the math on a $600,000 asset purchase where the C Corp has $250,000 in basis:

- C Corp gain: $350,000

- Federal corporate tax at 21%: $73,500

- Remaining for distribution: $526,500

- Shareholder capital gains tax (assuming 23.8% combined rate): up to $65,807

- Total tax hit: $139,307

Your S Corp, however, gets a stepped-up basis in the acquired assets equal to the purchase price. This means higher depreciation deductions going forward, which partially offsets the seller’s tax pain through your own future savings.

The IRC Section 338(h)(10) Election Alternative

There is a hybrid approach that deserves serious attention. If both the buyer and seller agree, they can make an election under IRC Section 338(h)(10). This election allows a stock purchase to be treated as an asset purchase for tax purposes. The S Corp buys the C Corp’s stock, but the IRS pretends the C Corp sold all its assets, paid tax, and liquidated.

Why would anyone volunteer for this? Because the S Corp buyer gets the stepped-up basis in assets (bigger depreciation deductions) while avoiding the mechanical complexity of transferring individual assets, contracts, and licenses. It also sidesteps potential issues with non-assignable contracts, permits, and customer agreements that would otherwise need to be individually transferred in a true asset purchase.

The catch: the C Corp still pays corporate-level tax on the deemed asset sale. Both parties need to model the economics carefully because the buyer’s future depreciation benefits must outweigh the seller’s additional tax cost for this election to make sense.

Five Costliest Mistakes When an S Corp Acquires a C Corp

After reviewing hundreds of acquisition structures, these five errors consistently destroy the most value for California S Corp owners.

Mistake 1: Ignoring the QSub BIG Tax Exposure

Estimated cost: $15,000 to $63,000.

Making a QSub election without calculating built-in gains exposure means you could face a 21% federal tax on appreciation that existed before the acquisition. The five-year recognition period under IRC Section 1374 applies to any gains recognized on assets that had built-in appreciation at the conversion date. Most buyers skip this analysis entirely and discover the BIG tax liability on their first post-acquisition return.

Mistake 2: Failing to Eliminate Inherited AE&P

Estimated cost: $8,000 to $25,000.

Inherited accumulated earnings and profits from the C Corp contaminate your S Corp’s distribution ordering. Without a deliberate AE&P elimination strategy using the AAA bypass election under IRC Section 1368(e)(3) or a qualifying dividend under IRC Section 1371(e), every shareholder distribution risks being recharacterized as a taxable dividend instead of a tax-free return of basis.

Mistake 3: Missing California’s Separate Tax Layer

Estimated cost: $4,200 to $18,000.

California does not conform to federal bonus depreciation under Revenue and Taxation Code Sections 17250 and 24356. This means your stepped-up basis from the acquisition generates different depreciation schedules at the federal and state levels. You must maintain dual depreciation tracking from day one. California also imposes its own 1.5% franchise tax on S Corps (versus 8.84% on C Corps), and the gross receipts fee applies if the acquired business pushes your total revenue over $250,000.

Mistake 4: Triggering an Involuntary S Election Termination

Estimated cost: $22,000 to $47,000.

If you acquire C Corp stock without immediately making the QSub election, your S Corp now holds stock in a C Corporation. Under IRC Section 1361(b)(1)(B), S Corps can only have permitted shareholders. A C Corp subsidiary that is not a QSub can terminate your S election entirely, retroactively converting your S Corp back to C Corp status. The five-year re-election lockout under IRC Section 1362(g) applies, and you would need a $15,300 Private Letter Ruling to recover early.

Mistake 5: Skipping the AB 150 PTE Election Post-Acquisition

Estimated cost: $6,000 to $14,000.

California’s AB 150 Pass-Through Entity (PTE) tax election lets S Corp owners bypass the $40,000 SALT deduction cap made permanent under the One Big Beautiful Bill Act (OBBBA). After an acquisition that increases your S Corp’s taxable income, the PTE election benefit grows proportionally. Missing the annual June 15 election deadline means losing this SALT workaround for the entire tax year. On $300,000 in combined S Corp income, the missed PTE election costs roughly $9,800 in unnecessary federal tax.

KDA Case Study: Sacramento Marketing Agency Owner Navigates $1.2M C Corp Acquisition

Marcus, a Sacramento-based S Corp owner running a digital marketing agency, wanted to acquire a competing C Corporation with $1.2 million in annual revenue and $400,000 in net assets. The C Corp had $180,000 in accumulated earnings and profits, equipment with $120,000 in built-in gains, and three non-assignable client contracts worth $250,000 annually.

His attorney recommended a straight stock purchase. His previous accountant said “it should be fine.” Neither mentioned the BIG tax, the AE&P contamination, or California’s bonus depreciation nonconformity.

KDA intervened with a three-part strategy. First, we modeled the IRC Section 338(h)(10) election against a QSub election and determined the QSub route saved Marcus $34,200 over five years because the BIG tax exposure on his specific asset mix was only $25,200, while the 338(h)(10) would have triggered $59,400 in immediate C Corp-level tax. Second, we implemented an AE&P elimination schedule using the IRC Section 1368(e)(3) bypass election, preventing $42,840 in potential dividend recharacterization over three years. Third, we activated the AB 150 PTE election, capturing $11,400 in SALT savings in year one alone.

Total first-year tax savings: $38,400. KDA engagement cost: $5,800. First-year ROI: 6.6x. Projected five-year savings: $164,000.

Ready to see how we can help you? Explore more success stories on our case studies page to discover proven strategies that have saved our clients thousands in taxes.

California-Specific Rules That Change the Acquisition Math

If you are operating in California, the federal rules above are only half the story. The state adds its own tax layers that change the cost-benefit analysis on every acquisition structure.

Franchise Tax Differential

California taxes C Corps at 8.84% of net income and S Corps at 1.5%. When your S Corp acquires a C Corp and makes a QSub election, the combined entity’s California tax rate drops from 8.84% to 1.5% on the acquired business’s income. On $200,000 in acquired profit, that is a $14,680 annual California tax reduction. However, if the QSub election is delayed or botched, the C Corp continues filing separately at 8.84% until the election is properly effective.

Bonus Depreciation Nonconformity

Under the OBBBA, 100% federal bonus depreciation is now permanent. California does not conform under R&TC Sections 17250 and 24356. When you acquire assets with a stepped-up basis (whether through asset purchase or 338(h)(10) election), your federal depreciation deductions will be significantly higher than California’s in years one through five. You must maintain dual depreciation schedules for every acquired asset. Failing to do so results in either overpaying California taxes or underpaying them (which triggers FTB penalties and interest).

AB 150 PTE Election Interaction

Post-acquisition, your S Corp’s income likely increases substantially. The AB 150 PTE election allows the entity to pay state tax at the entity level, generating a dollar-for-dollar credit on each shareholder’s personal return. This effectively bypasses the OBBBA’s permanent $40,000 SALT cap. The election must be made annually by June 15, and the first estimated payment is due with the election. Our entity formation services include post-acquisition restructuring to ensure every election and filing deadline is met.

Gross Receipts Fee Adjustment

California’s gross receipts fee applies to LLCs (not S Corps directly), but if the acquired C Corp was structured as an LLC taxed as a C Corp, converting it to a QSub changes the fee calculation. The fee ranges from $900 to $11,790 depending on gross receipts. Understanding whether this fee applies post-acquisition requires analyzing the acquired entity’s legal structure, not just its tax classification.

OBBBA Permanent Changes That Affect Every S Corp Acquisition in 2026

The One Big Beautiful Bill Act made several provisions permanent that directly impact how an S Corp acquires a C Corp.

Permanent 100% Bonus Depreciation

Previously scheduled to phase down from 80% in 2024 to 0% by 2027, bonus depreciation is now permanently set at 100%. This makes asset purchases and 338(h)(10) elections significantly more attractive because the stepped-up basis generates immediate, full depreciation deductions at the federal level. On a $400,000 asset acquisition, that is a $400,000 first-year federal deduction, saving a 37% bracket taxpayer $148,000 in federal taxes.

Permanent QBI Deduction Under IRC Section 199A

The 20% Qualified Business Income deduction is now permanent. After acquiring a C Corp and converting it to a QSub, the acquired business’s income flows through to the S Corp shareholder’s personal return and qualifies for QBI treatment (subject to income limitations and specified service trade or business rules). On $200,000 in acquired QBI, the deduction saves up to $14,800 in federal taxes annually.

Permanent $40,000 SALT Cap

The SALT deduction cap, originally set at $10,000 under the 2017 Tax Cuts and Jobs Act, is now permanently set at $40,000. California S Corp owners must use the AB 150 PTE election to work around this cap. Post-acquisition, the larger S Corp income makes the PTE election even more valuable.

$2.5 Million Section 179 Limit

The expanded Section 179 expensing limit of $2.5 million (with a $4 million phase-out threshold) gives acquiring S Corps additional flexibility to immediately deduct qualifying equipment and property from the acquired C Corp. Combined with permanent bonus depreciation, the depreciation strategy on acquired assets is more powerful than any point in the last 20 years. Remember, California caps Section 179 at $25,000 under R&TC Section 17255, creating yet another dual-tracking requirement.

Stock Purchase vs. Asset Purchase vs. 338(h)(10): Decision Framework

| Factor | Stock Purchase + QSub | Asset Purchase | 338(h)(10) Election |

|---|---|---|---|

| Stepped-Up Basis | No (carryover basis) | Yes (full FMV basis) | Yes (full FMV basis) |

| BIG Tax Risk | Yes, 5-year period | No (C Corp pays on sale) | No (C Corp pays on deemed sale) |

| AE&P Contamination | Yes, must eliminate | No (stays with C Corp) | No (eliminated in deemed liquidation) |

| Non-Assignable Contracts | Preserved automatically | Must be reassigned | Preserved automatically |

| Seller Tax Impact | Capital gains on stock sale | Double tax (corporate + shareholder) | Double tax (deemed sale + deemed liquidation) |

| Complexity Level | Moderate | High (individual asset transfers) | Moderate (stock transfer + election) |

| Best For | Low built-in gains, clean AE&P | Cherry-picking specific assets | Wanting stepped-up basis without asset transfer hassle |

What Happens If the Acquired C Corp Has Net Operating Losses?

If the C Corp you are acquiring has accumulated net operating losses (NOLs), those losses do not simply transfer to your S Corp. Under IRC Section 382, a change in ownership limits the annual amount of NOLs that can be used post-acquisition. The annual limitation equals the value of the acquired corporation multiplied by the long-term tax-exempt rate (published monthly by the IRS).

For a $500,000 acquisition with a 4.5% long-term rate, the annual Section 382 limitation would be approximately $22,500. If the C Corp had $300,000 in NOLs, it would take over 13 years to use them all, and that assumes the acquired business generates enough income each year. Many buyers overvalue C Corp NOLs in their acquisition pricing, paying premium prices for tax attributes they can barely use.

In a QSub election scenario, the C Corp’s NOLs become subject to both Section 382 and the SRLY (Separate Return Limitation Year) rules, further restricting their availability. Asset purchases eliminate this issue entirely because the buyer does not acquire the seller’s tax attributes.

Will This Acquisition Trigger an IRS Audit?

The IRS Palantir SNAP AI system cross-references Form 2553 (S Corp election), Form 1120-S (S Corp return), and Form 1120 (C Corp return) filings. When a C Corp’s final return is filed in the same year an S Corp reports a significant income increase, the matching algorithm flags the transaction for review.

Three specific audit triggers to manage:

- QSub election timing: If the QSub election date does not align with the stock acquisition closing date, the IRS will question whether the S Corp held impermissible C Corp stock during the gap period.

- Built-in gains reporting: Form 1120-S, Schedule D requires detailed reporting of recognized built-in gains during the recognition period. Incomplete reporting triggers automatic correspondence audits.

- AE&P distribution ordering: If post-acquisition distributions exceed the AAA balance without proper documentation of the AE&P elimination strategy, the IRS recharacterizes excess distributions as dividends retroactively.

The best defense is meticulous documentation: a formal acquisition agreement referencing the chosen tax structure, a contemporaneous BIG tax calculation, an AE&P ledger with elimination timeline, and dual depreciation schedules for California.

Ready to Reduce Your Tax Bill?

KDA Inc. specializes in strategic tax planning for business owners, S Corps, LLCs, and high-net-worth individuals. Book a personalized consultation and walk away with a clear plan.

Frequently Asked Questions

Can an S Corp own stock in a C Corp without making a QSub election?

Only if the S Corp owns less than 80% of the C Corp stock. Holding 80% or more without a QSub election does not automatically terminate the S election, but holding 100% of a C Corp’s stock while failing to make the QSub election creates significant compliance risk. The safest approach is to make the QSub election effective on the same day as the stock acquisition closing.

How long does the Built-In Gains tax recognition period last?

Five years from the date the QSub election becomes effective. Any built-in gains recognized during this period are taxed at 21% at the corporate level, in addition to the shareholder-level tax on the pass-through income. After the five-year period expires, the BIG tax no longer applies.

Does California impose its own Built-In Gains tax?

Yes. California imposes a 1.5% BIG tax on S Corporations, applied to the same built-in gains that trigger the federal 21% BIG tax. While 1.5% sounds small, on $300,000 in built-in gains, that is an additional $4,500 in California tax on top of the $63,000 federal BIG tax.

Can the S Corp use the C Corp’s tax credits after acquisition?

Generally no. Most tax credits are non-transferable in a stock acquisition. In an asset purchase, tax credits remain with the selling C Corp. Some credits, like the R&D credit, may have limited carryforward potential under Section 382 limitations, but the practical value is usually minimal.

What is the deadline to make a QSub election?

The QSub election on Form 8869 can be filed at any time during the tax year, effective on a specified date. However, the election should be filed to be effective on or before the stock acquisition closing date to avoid any period where the S Corp holds impermissible C Corp stock. Late elections may be available under Rev. Proc. 2013-30 with reasonable cause.

Should I buy the C Corp’s stock or its assets?

It depends on five factors: the amount of built-in gains, the AE&P balance, the existence of non-assignable contracts, the seller’s tax situation, and your post-acquisition depreciation strategy. Stock purchases are simpler but carry BIG tax and AE&P risk. Asset purchases give you stepped-up basis but trigger double taxation for the seller. The 338(h)(10) election offers a middle ground. Model all three scenarios with exact numbers before deciding.

This information is current as of April 18, 2026. Tax laws change frequently. Verify updates with the IRS or FTB if reading this later.

Book Your Acquisition Tax Strategy Session

If you are an S Corp owner considering acquiring a C Corporation, the difference between the right structure and the wrong one is $30,000 to $140,000 in unnecessary taxes. Do not let a handshake deal turn into a six-figure tax bill. Book a personalized acquisition strategy session with our team, and we will model every scenario, identify every trap, and build the structure that keeps more of the deal value in your pocket. Click here to book your consultation now.

“The IRS does not care how good your acquisition deal was. It only cares whether you structured it correctly.”