What the 2024 CA Tax Table Actually Costs You

You filed your California taxes. You saw the bracket. You paid the bill. But did you actually understand what hit you? Most taxpayers treat the 2024 CA tax table like a fixed sentence instead of a negotiable framework. The difference between those two mindsets is often $5,000 to $15,000 in unnecessary payments every single year.

California operates one of the most progressive state tax systems in the nation, with nine income brackets ranging from 1% to 12.3%, plus an additional 1% Mental Health Services Tax on income over $1 million. If you earned $150,000 in 2024, your effective state tax rate landed around 6.8%, but your marginal rate sat at 9.3%. That gap is where strategy lives.

Quick Answer

The 2024 CA tax table is California’s graduated income tax structure with rates from 1% to 13.3% (including the mental health surcharge). Your actual tax depends on your filing status, total income, and available deductions. Strategic planning around this table can reduce your effective rate by 2-4 percentage points, saving $8,000 to $20,000 annually for mid-to-high earners.

Breaking Down the 2024 California Tax Brackets

California’s tax brackets adjust annually for inflation. For 2024, the structure looked materially different than federal brackets, and understanding these thresholds is critical for planning.

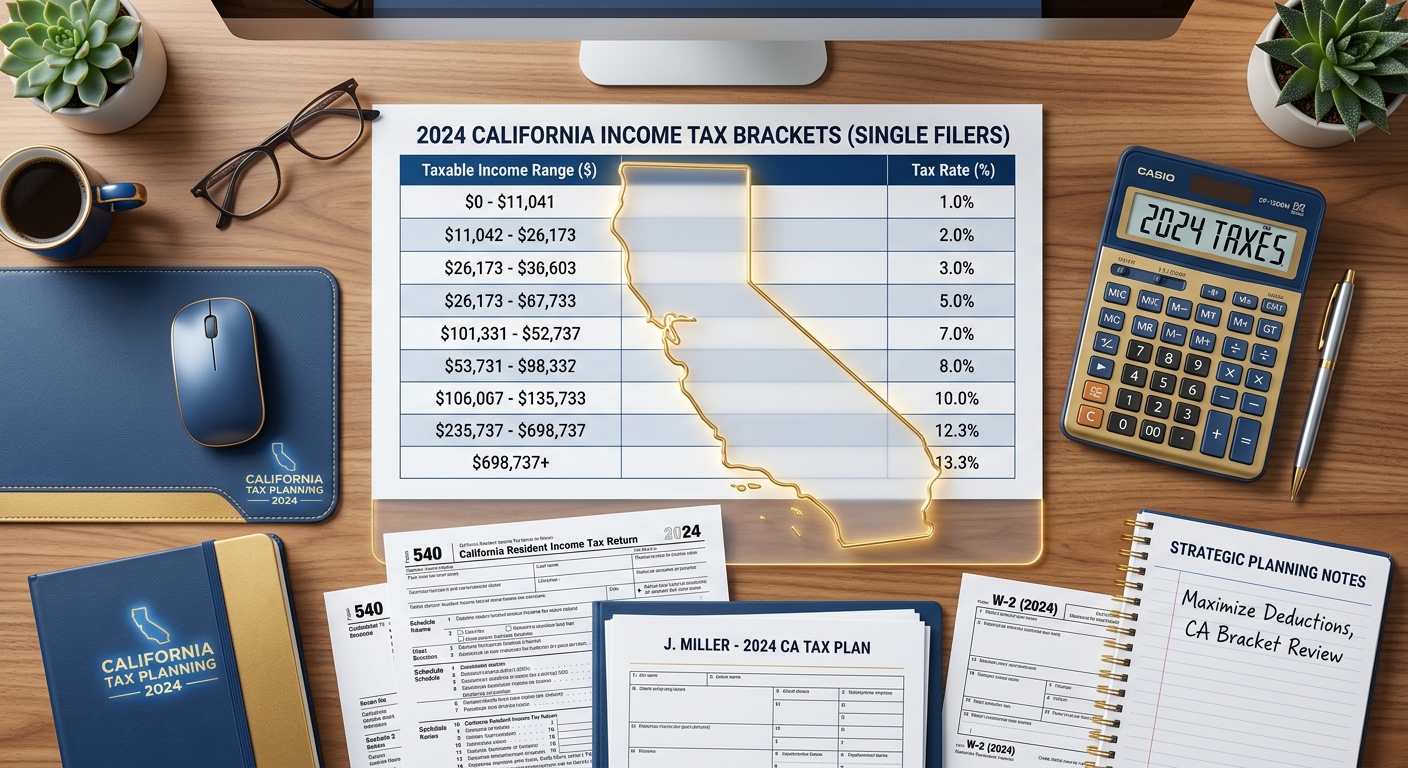

2024 CA Tax Table: Single Filers

| Taxable Income Range | Tax Rate | Tax Owed (Cumulative) |

|---|---|---|

| $0 – $10,412 | 1% | $104.12 |

| $10,413 – $24,684 | 2% | $389.56 |

| $24,685 – $38,959 | 4% | $960.56 |

| $38,960 – $54,081 | 6% | $1,867.82 |

| $54,082 – $68,350 | 8% | $3,009.34 |

| $68,351 – $349,137 | 9.3% | $29,120.42 |

| $349,138 – $418,961 | 10.3% | $36,311.89 |

| $418,962 – $698,271 | 11.3% | $67,864.88 |

| $698,272+ | 12.3% | Calculated on excess |

| $1,000,000+ | 13.3% (with MHST) | Calculated on excess |

2024 CA Tax Table: Married Filing Jointly

| Taxable Income Range | Tax Rate | Tax Owed (Cumulative) |

|---|---|---|

| $0 – $20,824 | 1% | $208.24 |

| $20,825 – $49,368 | 2% | $779.12 |

| $49,369 – $77,918 | 4% | $1,921.12 |

| $77,919 – $108,162 | 6% | $3,735.76 |

| $108,163 – $136,700 | 8% | $6,018.80 |

| $136,701 – $698,274 | 9.3% | $58,240.96 |

| $698,275 – $837,922 | 10.3% | $72,623.78 |

| $837,923 – $1,396,542 | 11.3% | $135,729.76 |

| $1,396,543+ | 12.3% | Calculated on excess |

| $1,000,000+ (each spouse) | 13.3% (with MHST) | Calculated on excess |

Key Takeaway: California’s brackets double for married couples, but the 9.3% bracket extends much further than you’d expect. A married couple earning $600,000 still sits in the 9.3% marginal bracket, not the top rate.

What Most Taxpayers Miss About the 2024 CA Tax Table

Understanding the brackets is step one. Exploiting the structure is step two. Here are three critical insights that separate strategic filers from those who overpay year after year.

Marginal vs. Effective Rate Confusion

If you earned $100,000 as a single filer in 2024, your marginal rate was 9.3%. But your effective California tax rate was only around 4.8%. That means you paid roughly $4,800 in state income tax, not $9,300. The difference matters because most people mentally budget based on their marginal rate and end up surprised when their actual bill is lower, or they fail to recognize savings opportunities in lower brackets.

A W-2 employee making $95,000 might avoid a side hustle because “it’ll all be taxed at 9.3%.” In reality, the first $10,412 of that side income is taxed at just 1%, the next chunk at 2%, and so on. That $10,000 freelance project might only generate $700 in additional California tax, not $930.

The Standard Deduction Shield

California offers its own standard deduction separate from the federal system. For 2024, single filers received a $5,363 standard deduction, and married couples filing jointly received $10,726. This amount comes directly off your California taxable income before the brackets even apply.

Here’s the math: A single filer with $60,000 in California adjusted gross income first subtracts the $5,363 standard deduction, leaving $54,637 in taxable income. That puts them squarely in the 8% bracket instead of pushing higher. The standard deduction alone saves approximately $429 in state taxes (8% of $5,363).

Strategic Income Timing Around Bracket Thresholds

If your taxable income sits near a bracket threshold, small shifts create outsize savings. Consider a consultant earning $67,000 in 2024. They sit just below the $68,350 threshold where the 9.3% rate kicks in. By deferring a $5,000 December payment to January 2025, they keep that income in the 8% bracket for 2024, saving $65 on that specific chunk (1.3% difference on $5,000).

Multiply this across multiple income streams, retirement contributions, or business expenses, and bracket management becomes a repeatable $2,000 to $5,000 annual savings lever. Many taxpayers ignore this entirely and let income fall wherever it lands.

How Business Owners Use the 2024 CA Tax Table Strategically

W-2 employees have limited control over their California taxable income. Business owners and self-employed individuals, however, can structure entities, time income, and deploy deductions to navigate the 2024 CA tax table with precision.

S Corp Salary Optimization

S Corp owners pay California income tax on their total share of business profit, but they can control the timing and character of distributions. An LLC taxed as an S Corp with $200,000 in net profit might pay the owner a $80,000 salary and distribute the remaining $120,000 as a distribution. While both are subject to California income tax, the distribution avoids the 15.3% self-employment tax at the federal level.

On the California side, the owner pays 9.3% on income over $68,350. Strategic planning focuses on maximizing federal deductions (like retirement contributions) that also reduce California taxable income, pulling total income closer to lower brackets. A Solo 401(k) contribution of $30,000 reduces both federal and California taxable income, saving approximately $2,790 in state taxes alone (9.3% of $30,000).

Timing Year-End Bonuses and Estimated Payments

Business owners can defer December bonuses, customer payments, or contract revenue into January to keep 2024 income below specific thresholds. A real estate investor selling a rental property in late 2024 might structure the close for early January 2025, deferring the entire capital gain into the next tax year. This doesn’t reduce total tax, but it provides cash flow control and planning flexibility.

California requires estimated quarterly tax payments. If you underpay, you’ll owe penalties. If you overpay, you’re giving the state an interest-free loan. Using the 2024 CA tax table to project your exact liability ensures you pay just enough to avoid penalties while keeping cash working for you throughout the year.

Leveraging California-Specific Deductions

California doesn’t conform to all federal tax law changes, which creates unique planning opportunities. For example, California still allows a full deduction for state and local taxes (SALT) on your state return, even though the federal SALT deduction is capped at $10,000. If you paid $18,000 in property taxes in 2024, you deduct the full amount on your California return, reducing your state taxable income and saving approximately $1,674 (9.3% of $18,000 if you’re in that bracket).

California also offers credits for renters, dependent care, and solar installations. These reduce your tax liability dollar-for-dollar, which is far more valuable than a deduction. A renter credit of $120 directly cuts your tax bill by $120, regardless of your bracket.

KDA Case Study: High-Earning W-2 Engineer

Marcus, a software engineer in San Francisco, earned $185,000 in W-2 income in 2024. His wife earned $95,000 as a healthcare consultant. Filing jointly, their combined California taxable income hit $280,000 before deductions, landing them firmly in the 9.3% marginal bracket.

They came to KDA frustrated by their $18,500 California tax bill and felt they had no control. We implemented three immediate changes:

- Maxed 401(k) contributions: Both spouses contributed the full $23,000 to their employer 401(k) plans, reducing California taxable income by $46,000 and saving $4,278 in state taxes (9.3% of $46,000).

- Opened a backdoor Roth IRA: While this doesn’t reduce current-year California taxes, it created a tax-free growth vehicle for retirement.

- Claimed all available itemized deductions: We identified $22,000 in California itemized deductions (property taxes, mortgage interest, charitable contributions) versus the $10,726 standard deduction, saving an additional $1,048 in state taxes.

Total first-year California tax savings: $5,326. They paid KDA $2,400 for tax planning and preparation, netting a 2.2x return in year one alone. Over five years, the compounding effect of optimized contributions and strategic deductions will save them over $30,000.

Ready to see how we can help you? Explore more success stories on our case studies page to discover proven strategies that have saved our clients thousands in taxes.

Special Situations and Edge Cases

The 2024 CA tax table works predictably for most taxpayers, but several scenarios create planning complications or opportunities.

Part-Year Residents and Non-Residents

If you moved to or from California during 2024, you’ll file as a part-year resident and only pay California tax on income earned while you were a California resident. This gets complex fast. California taxes all income from California sources, even if you’re a non-resident. If you lived in Nevada but earned consulting income from a California client, that income is subject to California tax.

Example: You lived in California from January through June 2024, then moved to Texas. You earned $80,000 during those six months and $80,000 in Texas for the rest of the year. California will tax the first $80,000 using the 2024 CA tax table, but you’ll prorate the standard deduction and personal exemption credits based on months of residency.

Multi-State Tax Credits

If you paid income tax to another state in 2024, California offers a credit to prevent double taxation. You’ll still pay California tax on all your income as a resident, but you receive a credit for taxes paid to other states on income earned there. This credit is limited to the amount of California tax on that same income.

Let’s say you earned $50,000 from a Colorado rental property and paid $2,000 in Colorado state tax. California will tax that $50,000, but you’ll receive a credit of up to $2,000 (or the California tax on that income, whichever is lower). If the California tax on that $50,000 would’ve been $4,650 (9.3%), you’d still owe California an additional $2,650 after the credit.

Capital Gains and the Mental Health Services Tax

California taxes capital gains as ordinary income. There’s no preferential rate like the federal system. If you sold stock in 2024 and realized a $100,000 long-term capital gain, California treats it identically to $100,000 in W-2 wages. This is brutal for high earners.

The Mental Health Services Tax adds another 1% on taxable income over $1 million. If you’re a single filer with $1.2 million in taxable income (perhaps from a business sale or major stock sale), you’ll pay 12.3% on income between $698,272 and $1 million, then 13.3% on income over $1 million. On that $200,000 above the threshold, you’ll owe $26,600 in California tax alone.

This is where strategic planning around tax planning services becomes essential. Spreading income recognition across multiple years, using installment sales, or structuring asset sales inside specific entities can mitigate these spikes.

Passive Activity Losses and California Adjustments

If you own rental properties or invest as a limited partner, passive activity loss rules apply. California generally conforms to federal passive loss rules but with key exceptions. For example, California doesn’t allow the $25,000 rental real estate exception available to active participants under federal law unless you meet stricter California criteria.

A real estate investor with $15,000 in rental losses might deduct those losses federally but find them suspended in California, increasing California taxable income. This creates a temporary timing difference that reverses when the property is sold or when you generate passive income to absorb the losses.

What Happens If You Miss This?

Ignoring the structure of the 2024 CA tax table doesn’t just cost you money once. It creates a compounding penalty across multiple areas:

Overpayment of estimated taxes: If you calculate quarterly payments based on your marginal rate instead of your effective rate, you’ll consistently overpay and tie up cash that could earn returns elsewhere. On a $150,000 income, overestimating by even 2 percentage points means $3,000 in unnecessary advance payments each year.

Missed deduction opportunities: Failing to understand how deductions interact with the brackets means you don’t prioritize the right strategies. A $10,000 business expense deduction saves you $930 in California tax if you’re in the 9.3% bracket, but only $123 if you’re in the 1% bracket. Knowing where you land tells you which deductions deliver real value.

Poor entity structure decisions: Business owners who don’t model their income against the California tax table often choose the wrong entity. An LLC owner earning $250,000 might save $3,500 annually by electing S Corp status and implementing reasonable salary strategies, but they’ll never discover that without running the numbers.

Audit risk from misreporting: California’s Franchise Tax Board aggressively audits high earners and businesses. Misunderstanding your tax liability often leads to incorrect estimated payments, which triggers automated notices. These notices create administrative headaches and potential penalties even if you don’t owe additional tax.

California-Specific Considerations for 2024

California’s tax code diverges from federal law in several critical areas that directly impact how you use the 2024 CA tax table.

No Federal TCJA Conformity

California did not conform to many provisions of the 2017 Tax Cuts and Jobs Act. This means California still allows personal exemption credits ($144 per exemption in 2024), while the federal return does not. A family of four receives $576 in personal exemption credits on their California return, reducing tax owed by that amount directly.

Different Depreciation Rules

California requires different depreciation schedules for assets placed in service after certain dates. If you claimed 100% bonus depreciation on equipment federally, California might require you to depreciate it over five or seven years. This creates a timing difference where your California taxable income is higher in early years and lower in later years compared to your federal return.

Health Insurance Mandate Penalty

California enforces an individual health insurance mandate. If you or your dependents lacked minimum essential coverage in 2024 and don’t qualify for an exemption, you’ll owe a penalty calculated as the greater of 2.5% of household income over the filing threshold or $900 per adult and $450 per child (up to $2,700 per family). This penalty is separate from the income tax calculated using the 2024 CA tax table but increases your total tax liability.

Earned Income Tax Credit (CalEITC)

California offers its own Earned Income Tax Credit, which phases in and out at different income levels than the federal EITC. For 2024, CalEITC was available to taxpayers with earned income up to approximately $30,950 (depending on filing status and number of qualifying children). The credit maxes out around $3,417 for filers with three or more children.

This is a refundable credit, meaning if your CalEITC exceeds your total California tax liability, the state sends you a refund for the difference. Many eligible taxpayers never claim it because they don’t realize California has a separate EITC system.

5 Steps to Use the 2024 CA Tax Table to Cut Your Bill

Here’s the exact process KDA uses to help clients minimize California income tax using the bracket structure as a strategic framework.

Step 1: Calculate Your True Taxable Income

Start with your federal adjusted gross income, then make California-specific adjustments. Add back items California doesn’t allow (like certain business deductions limited under federal law but allowed in California). Subtract California-specific deductions (full SALT deduction, for example). This gives you your California adjusted gross income.

From there, subtract either the standard deduction or itemized deductions (whichever is greater) and apply personal exemption credits. The result is your California taxable income, which you’ll run through the 2024 CA tax table.

Time estimate: 20-30 minutes with organized records

Step 2: Identify Your Marginal and Effective Rates

Use the table earlier in this post to pinpoint your marginal bracket. Then calculate your effective rate by dividing your total California tax liability by your California taxable income. This tells you two critical numbers: what rate applies to your next dollar of income, and what rate you’re actually paying on average.

If your marginal rate is 9.3% but your effective rate is 5.2%, you know there’s room to add income (from Roth conversions, side hustles, etc.) without hitting punitive rates.

Time estimate: 10 minutes

Step 3: Model Major Decisions Against the Brackets

Before you take a distribution, sell an asset, or exercise stock options, run the numbers. Add that income to your current taxable income and see where it lands. A $50,000 stock option exercise might push you from the 8% bracket into the 9.3% bracket, costing an extra $650 on that income alone (1.3% on $50,000).

Knowing this ahead of time lets you split the exercise across two years, keeping more income in lower brackets.

Time estimate: 15-20 minutes per decision

Step 4: Maximize Deductions That Reduce California Taxable Income

Prioritize deductions that work on both your federal and California returns. These include:

- Traditional 401(k) or 403(b) contributions (up to $23,000 in 2024, or $30,500 if age 50+)

- Health Savings Account contributions ($4,150 individual, $8,300 family in 2024)

- Self-employed retirement plans (SEP-IRA, Solo 401(k))

- Educator expenses, student loan interest, IRA contributions (if eligible)

Each dollar of deduction in the 9.3% bracket saves $0.093 in California tax, plus your federal tax savings. A $10,000 traditional IRA contribution saves $930 in California tax and approximately $2,400 in federal tax (assuming 24% federal bracket), totaling $3,330.

Time estimate: 30-45 minutes to review all options

Step 5: File Correctly and Track for Next Year

Use tax software that handles California-specific adjustments or work with a CPA who specializes in California tax. Errors on California returns trigger Franchise Tax Board notices, which are time-consuming to resolve even when you don’t owe additional tax.

After filing, document what worked. If a specific strategy saved $2,000, repeat it next year and look for ways to scale it. Tax planning is a year-round process, not a one-time April event.

Time estimate: 2-4 hours for filing, 15 minutes for documentation

Key Takeaway: Using the 2024 CA tax table strategically requires five disciplined steps. Most taxpayers skip Step 3 (modeling decisions) and Step 5 (tracking results), which is why they repeat the same costly mistakes every year.

Ready to Reduce Your Tax Bill?

KDA Inc. specializes in strategic tax planning for business owners, S Corps, LLCs, and high-net-worth individuals. Book a personalized consultation and walk away with a clear plan.

Frequently Asked Questions

Does California tax Social Security income?

No. California does not tax Social Security retirement benefits, even though the federal government may tax a portion of those benefits depending on your income. If you received $30,000 in Social Security in 2024, that amount is completely excluded from your California taxable income.

How does California tax unemployment benefits?

California taxes unemployment benefits as ordinary income, just like wages. If you collected $15,000 in unemployment in 2024, that’s added to your other income and taxed according to the 2024 CA tax table. Unemployment benefits are also subject to federal income tax.

What’s the difference between California AGI and federal AGI?

California adjusted gross income starts with your federal AGI, then adds or subtracts California-specific items. For example, California adds back certain federal deductions it doesn’t recognize and subtracts items it allows that the federal return doesn’t. The result is often different from your federal AGI, sometimes by thousands of dollars.

Can I deduct my federal tax payment on my California return?

No. You cannot deduct federal income taxes on your California return. However, you can deduct state and local taxes (including California income tax) on your federal return, subject to the $10,000 SALT cap. California, in turn, allows you to deduct the full amount of property taxes and other state and local taxes on your California return without a cap.

What if I owe California tax but can’t pay by the deadline?

File your return on time even if you can’t pay. California charges penalties and interest on unpaid balances, but the failure-to-file penalty is much steeper than the failure-to-pay penalty. You can request a payment plan through the Franchise Tax Board’s website. Interest accrues on the unpaid balance, but a payment plan prevents collection actions like liens or levies.

Red Flag Alert: Common Mistakes That Trigger FTB Scrutiny

Mismatched federal and California deductions: The Franchise Tax Board receives a copy of your federal return. If your California itemized deductions wildly differ from your federal Schedule A without clear explanation, expect a notice asking for documentation.

Underreporting estimated tax payments: If you made quarterly payments but forget to claim them on your return, California will assess additional tax and penalties. Always keep confirmation numbers and payment records for every estimated payment.

Incorrectly claiming non-resident status: High earners try to claim Nevada or Texas residency while still living in California. The FTB audits residency aggressively. If you spent more than nine months in California, maintained a California driver’s license, registered your car here, or kept your primary residence here, you’re a California resident for tax purposes regardless of what you claim.

Overstating business losses: Hobby loss rules apply in California just like they do federally. If you report business losses year after year without ever showing a profit, the FTB will reclassify your activity as a hobby and disallow the losses. Make sure your business has a genuine profit motive and keep detailed records proving it.

Pro Tip: The FTB’s automated systems flag returns with statistical outliers. If your deductions are significantly higher than other taxpayers in your income range, document everything meticulously and consider attaching explanations to your return.

Looking Ahead: 2025 and Beyond

California adjusts its tax brackets annually for inflation. The 2025 brackets will shift slightly higher, meaning the income thresholds where each rate kicks in will increase by approximately 3-4% based on recent inflation trends. If the $68,350 threshold in 2024 adjusts to $70,800 in 2025, you’ll keep an extra $2,450 of income in the 8% bracket instead of the 9.3% bracket, saving roughly $32 on that slice alone.

Proposed legislation in Sacramento could introduce new brackets or surtaxes on ultra-high earners. A wealth tax bill has been floated multiple times. While not yet law, it’s worth monitoring if your net worth exceeds $50 million.

Strategic planning in 2024 sets the foundation for multi-year savings. Maxing retirement contributions, optimizing entity structures, and timing major income events aren’t one-time wins. They’re repeatable systems that compound over decades.

This information is current as of 4/18/2026. Tax laws change frequently. Verify updates with the IRS or FTB if reading this later.

Book Your California Tax Strategy Session

If you’re still treating the 2024 CA tax table like a fixed bill instead of a framework you can navigate, you’re leaving thousands on the table every single year. Our team specializes in California-specific tax strategy for W-2 earners, business owners, real estate investors, and high-net-worth individuals.

We’ll model your exact income against the brackets, identify deductions you’re missing, and build a multi-year plan that reduces your effective California tax rate by 2-4 percentage points. That’s $8,000 to $25,000 in annual savings for most clients. Click here to book your consultation now.