What Is Form 1099-SA?

Form 1099-SA (Distributions from an HSA, Archer MSA, or Medicare Advantage MSA) is an IRS tax form sent to taxpayers who take distributions from Health Savings Accounts (HSAs), Archer Medical Savings Accounts (Archer MSAs), or Medicare Advantage MSAs during the tax year. This form reports the gross distribution amount and identifies the type of account. If you received a Form 1099-SA, you need to report those distributions on your tax return using Form 8889 to determine whether the distributions are tax-free (if used for qualified medical expenses) or taxable (if not). For 2026, understanding this form is critical because improper reporting can trigger IRS penalties of 20% on non-qualified distributions plus ordinary income tax on the amount withdrawn.

Quick Answer

Form 1099-SA reports money you took out of your Health Savings Account or other medical savings account during the tax year. If you spent that money on qualified medical expenses, it is tax-free. If you used it for non-medical purposes, you’ll owe income tax plus a 20% penalty (unless you’re over 65). You must report this form on Form 8889 when filing your taxes, even if the distribution was entirely for medical expenses.

Why Form 1099-SA Matters for Your Tax Return

Most taxpayers think HSA contributions are the only tax benefit, but the real power lies in distributions. When you take money out of an HSA and use it for qualified medical expenses, that money comes out completely tax-free. No income tax. No payroll tax. No capital gains. But if you mess up the reporting or use HSA funds for non-qualified expenses, the IRS will treat it as ordinary income and hit you with a 20% additional tax penalty.

Here’s what makes Form 1099-SA important: the IRS already has a copy. Your HSA custodian (like Fidelity, Optum, or HealthEquity) sends this form to both you and the IRS. If you fail to report it, the IRS will assume the entire distribution is taxable. That can cost you thousands in unnecessary taxes and penalties.

Who Receives Form 1099-SA?

You will receive Form 1099-SA if you:

- Withdrew money from your Health Savings Account during the tax year

- Took a distribution from an Archer MSA (rare, but still exists for some small business owners)

- Received funds from a Medicare Advantage MSA

- Used your HSA debit card to pay for anything (qualified or not)

- Transferred HSA funds to yourself rather than directly to a medical provider

Even if you only took out $50 to pay a copay, you’ll get a 1099-SA. The form doesn’t distinguish between qualified and non-qualified expenses; it just reports the gross distribution amount. That’s why Form 8889 exists: to tell the IRS what you actually used the money for.

The Three Distribution Scenarios That Change Your Tax Bill

Scenario 1: Qualified Medical Expenses

You withdrew $3,200 from your HSA to pay for dental work, prescription medications, and a medical procedure. Since all expenses are IRS-qualified medical expenses, the entire $3,200 distribution is tax-free. You still report it on Form 8889, but you owe $0 in taxes and $0 in penalties.

Scenario 2: Non-Qualified Expenses (Under Age 65)

You’re 42 years old and withdrew $2,000 from your HSA to pay off a credit card. This is a non-qualified distribution. You’ll owe ordinary income tax on $2,000 (let’s say 24% federal = $480) plus a 20% penalty ($400). Total tax cost: $880 for a $2,000 withdrawal.

Scenario 3: Non-Qualified Expenses (Age 65 or Older)

You’re 67 and withdrew $2,000 for a vacation. Since you’re over 65, the 20% penalty is waived. You still owe ordinary income tax on $2,000 (24% = $480), but no penalty. At 65+, your HSA essentially becomes a traditional IRA for non-medical withdrawals.

How to Read Your Form 1099-SA

Form 1099-SA is a simple one-page document, but every box matters for your tax reporting. Here’s what you need to know:

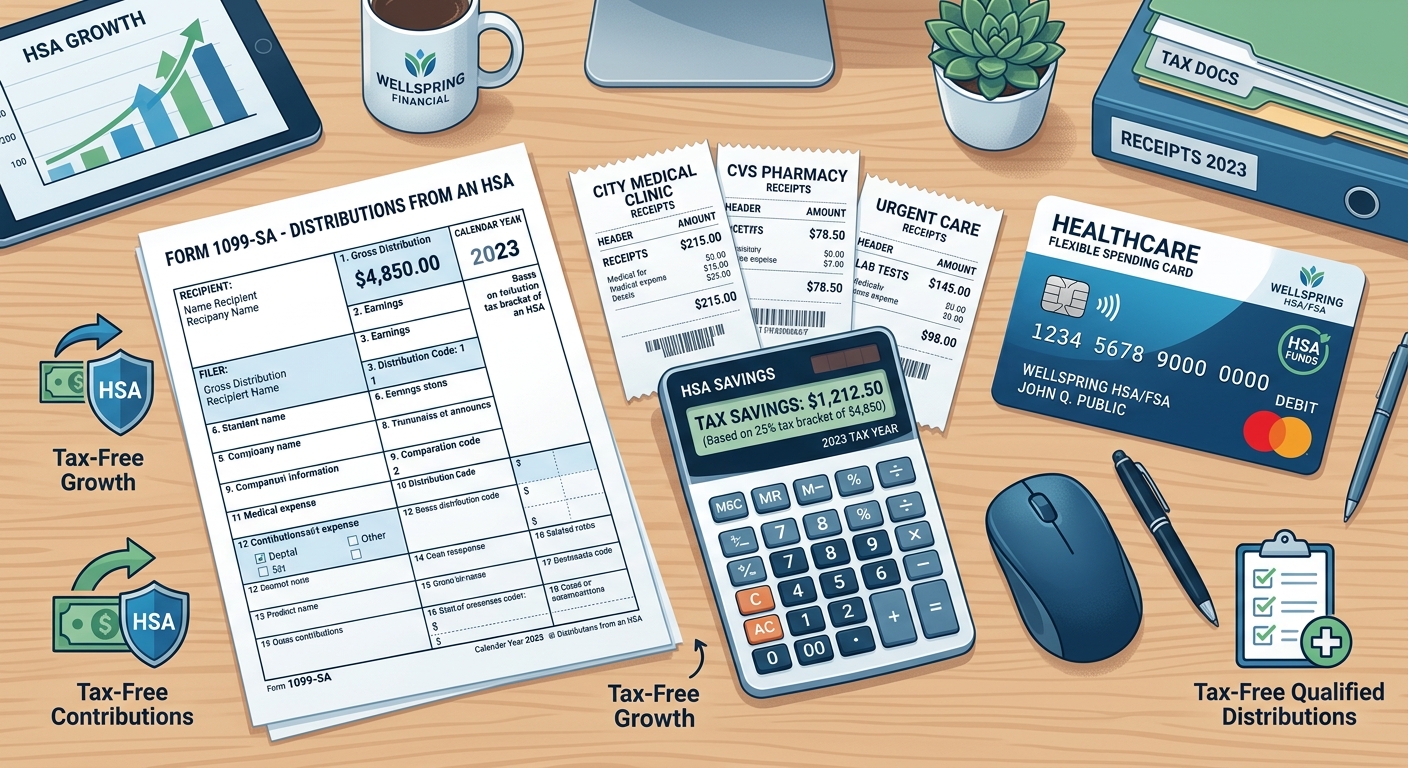

Box 1: Gross Distribution

This is the total amount you took out of your HSA during the tax year. It includes all withdrawals: reimbursements, debit card purchases, direct payments to medical providers, and even mistaken withdrawals. The IRS does not care why you took the money out; Box 1 just reports the gross total.

Example: You made three HSA withdrawals in 2025: $850 for an MRI, $1,400 for dental work, and $600 for a gym membership (non-qualified). Box 1 shows $2,850.

Box 2: Earnings on Excess Contributions

This box is rarely filled in, but when it is, it’s a red flag. Box 2 reports earnings on contributions you made that exceeded the annual HSA contribution limit. If you over-contributed to your HSA and had to withdraw the excess, the earnings on that excess are taxable. Most taxpayers never see a number in Box 2, but if you do, you need to report it as taxable income on Form 8889.

Box 3: Distribution Code

Box 3 tells the IRS what type of account you withdrew from. The codes are:

- Code 1: Health Savings Account (HSA) – most common

- Code 2: Archer MSA – rare, used by self-employed or small business employees

- Code 3: Medicare Advantage MSA – used by certain Medicare enrollees

For most taxpayers reading this, you’ll see Code 1. This code determines which section of Form 8889 you’ll use to report the distribution.

Box 4: Fair Market Value (FMV) on Date of Death

Box 4 is only used if the account holder died during the tax year and you are the beneficiary receiving the distribution. In that case, Box 4 shows the account’s fair market value on the date of death. Most living taxpayers will see this box blank.

Qualified Medical Expenses: What Actually Counts?

The IRS has strict rules about what qualifies as a medical expense for HSA purposes. This is not a “you know it when you see it” situation. The IRS publishes a list in Publication 502, and if your expense is not on that list, it’s taxable.

Always Qualified

- Doctor visits, hospital stays, surgery, lab tests, X-rays, MRIs

- Prescription medications (but not over-the-counter drugs unless prescribed)

- Dental care: cleanings, fillings, braces, extractions, dentures

- Vision care: eye exams, prescription glasses, contact lenses, LASIK surgery

- Physical therapy, occupational therapy, speech therapy

- Mental health counseling and psychiatric care

- Chiropractor visits and acupuncture

- Hearing aids and hearing exams

- Medical equipment: crutches, wheelchairs, blood pressure monitors

- Insulin and diabetic supplies

- Pregnancy and fertility treatments (including IVF)

Never Qualified

- Gym memberships (unless prescribed by a doctor for a specific medical condition)

- Cosmetic procedures (unless medically necessary, like reconstructive surgery after an accident)

- Over-the-counter medications (unless you have a prescription)

- Vitamins and supplements (unless prescribed)

- Health insurance premiums (with limited exceptions for COBRA, long-term care, and premiums while on unemployment)

- Teeth whitening, hair transplants, and other elective procedures

Gray Area: Ask Your Tax Pro

Some expenses fall into a gray area where a doctor’s prescription or letter of medical necessity can make the difference:

- Weight loss programs (qualified only if prescribed for a specific disease like obesity or hypertension)

- Special diet foods (qualified only if prescribed and the cost exceeds normal food costs)

- Home modifications (ramps, grab bars, etc., for medical reasons)

- Travel expenses for medical care (mileage, lodging, but not meals)

When in doubt, get documentation. A letter from your doctor stating the medical necessity can protect you in an audit.

Red Flag Alert: Common Form 1099-SA Mistakes That Trigger IRS Scrutiny

The IRS knows that HSA abuse is common. They specifically look for these red flags when reviewing Form 1099-SA reporting:

1. You Report the Distribution but Don’t File Form 8889

The number one mistake: you include the 1099-SA on your tax return but forget to attach Form 8889. The IRS computer systems are designed to match 1099-SA forms with corresponding Form 8889 filings. If you report the distribution without Form 8889, the IRS assumes the entire amount is taxable and sends you a bill.

Pro Tip: Even if your entire HSA distribution was for qualified medical expenses and you owe zero tax, you must still file Form 8889. There is no exception to this rule.

2. You Use HSA Funds for Non-Medical Expenses and Hope the IRS Won’t Notice

Some taxpayers treat their HSA like a personal checking account, using the debit card for groceries, gas, or other non-medical purchases. The IRS won’t catch this immediately, but if you’re ever audited, they will request receipts for every HSA distribution. If you can’t prove the expenses were qualified, you’ll owe back taxes, penalties, and interest going back years.

Reality Check: HSA audits are rare, but when they happen, the penalties are severe. The IRS can go back three years (or six years in cases of substantial underreporting). If you took $10,000 in non-qualified HSA distributions over three years, you could owe $2,000 in penalties plus $2,400 in taxes (assuming 24% bracket) plus interest. Total bill: $5,000+.

3. You Don’t Keep Receipts

The IRS does not require you to submit receipts with your tax return, but you must keep them in case of an audit. The statute of limitations for HSA distributions is the same as your tax return: three years from the filing date (or six years if you underreport income by 25% or more).

Best Practice: Create a folder (digital or physical) for every tax year. Save every receipt, explanation of benefits (EOB) from your insurance company, and credit card statement showing medical expenses. If you pay out of pocket and reimburse yourself later from your HSA, keep both the original receipt and a record of the HSA reimbursement.

4. You Forget About the 20% Penalty for Early Non-Qualified Withdrawals

If you’re under 65 and take a non-qualified distribution, you owe a 20% penalty on top of ordinary income tax. This is not optional. The penalty applies even if you didn’t realize the expense was non-qualified. The only exceptions:

- You’re 65 or older

- You’re disabled

- The distribution is made to a beneficiary after your death

Example: You’re 50 years old and withdraw $5,000 from your HSA to pay for a family vacation. You’ll owe income tax on $5,000 (let’s say 22% = $1,100) plus a 20% penalty ($1,000). Total tax cost: $2,100. That $5,000 vacation just cost you $7,100.

KDA Case Study: Self-Employed 1099 Contractor

Meet Jordan, a 38-year-old freelance graphic designer earning $95,000 annually as a 1099 contractor. Jordan contributed $4,300 to an HSA in 2025 (self-only coverage) and took two distributions during the year:

- $1,800 for a root canal and dental crown (qualified)

- $900 to pay for a gym membership and supplements (non-qualified)

Jordan received Form 1099-SA showing a $2,700 gross distribution (Box 1). When filing taxes, Jordan mistakenly assumed the entire amount was tax-free because it came from an HSA. Big mistake.

What KDA Did: We reviewed Jordan’s receipts, identified the $900 non-qualified distribution, and properly reported it on Form 8889. We calculated the tax impact: $900 x 24% (Jordan’s tax bracket) = $216 in income tax, plus $900 x 20% = $180 penalty. Total tax cost: $396.

We also advised Jordan to stop using HSA funds for non-medical expenses and set up a separate checking account for personal spending. By catching this early, we avoided a future audit where the IRS could have gone back multiple years and assessed much larger penalties.

Tax Savings Result: Jordan paid $396 in taxes on the non-qualified distribution (unavoidable) but avoided an estimated $2,200 in penalties and interest that would have accrued if the mistake had gone uncorrected for three years. Jordan paid KDA $650 for tax prep and HSA strategy consultation. First-year ROI: 3.4x when considering avoided future penalties.

Ready to see how we can help you? Explore more success stories on our case studies page to discover proven strategies that have saved our clients thousands in taxes.

How to Report Form 1099-SA on Your Tax Return

Reporting Form 1099-SA is a three-step process. You cannot skip any of these steps, even if your entire distribution was for qualified medical expenses.

Step 1: Gather Your Documentation

Before you start filling out Form 8889, collect:

- Your Form 1099-SA from your HSA custodian

- Receipts for all medical expenses you paid during the year (whether reimbursed from HSA or paid out of pocket)

- Your HSA contribution records (Form W-2 Box 12 Code W, or your own records if self-employed)

- Explanation of Benefits (EOB) statements from your health insurance company

You’ll need this documentation to complete Form 8889 accurately.

Step 2: Complete Form 8889

Form 8889 has three parts:

Part I: HSA Contributions and Deductions

Report all HSA contributions made during the year, including employer contributions, payroll deductions, and personal contributions. The 2026 contribution limits are $4,300 for self-only coverage and $8,550 for family coverage. If you’re 55 or older, add a $1,000 catch-up contribution.

Part II: HSA Distributions

This is where you report the gross distribution from Box 1 of Form 1099-SA. On Line 14a, enter the total distribution amount. On Line 15, enter the amount you used for qualified medical expenses. Line 16 calculates the taxable amount (if any).

Example: You took a $3,000 distribution. You spent $2,600 on qualified medical expenses and $400 on non-qualified expenses. Line 14a = $3,000. Line 15 = $2,600. Line 16 = $400 (taxable).

Part III: Income Tax and Additional Tax

If you have a taxable distribution (Line 16 is greater than zero), you’ll calculate the 20% penalty here (unless you’re 65+, disabled, or deceased).

Step 3: Attach Form 8889 to Your Form 1040

Form 8889 is not optional. It must be attached to your Form 1040 (U.S. Individual Income Tax Return) when you file. The taxable distribution flows to Form 1040 Schedule 1 Line 8. The 20% penalty flows to Schedule 2 Line 8.

If you e-file, your tax software will automatically attach Form 8889. If you paper-file, make sure Form 8889 is included in your mailing. Forgetting to attach it is one of the most common IRS audit triggers for HSA holders.

Special Situations That Complicate Form 1099-SA Reporting

You Changed Jobs Mid-Year and Have Multiple HSAs

If you switched employers and opened a new HSA, you may receive multiple Forms 1099-SA (one from each custodian). You must report all distributions on a single Form 8889. Add up the gross distributions from all 1099-SA forms and enter the total on Line 14a.

You Rolled Over HSA Funds to a New Custodian

If you did a trustee-to-trustee HSA rollover (moving funds directly from one HSA to another), you should not receive a Form 1099-SA. However, if you withdrew the funds and redeposited them yourself (an indirect rollover), you will receive a 1099-SA. You have 60 days to complete the rollover and avoid taxes. Report this on Form 8889 Part II and indicate it was a rollover.

Red Flag Alert: You can only do one indirect HSA rollover per 12-month period. If you do more than one, the second distribution is taxable and subject to the 20% penalty.

You Over-Contributed to Your HSA

If you contributed more than the annual limit, you must withdraw the excess contributions plus any earnings on those contributions by the tax filing deadline (including extensions). The excess contribution amount is not taxable when withdrawn, but the earnings are. Those earnings will be reported in Box 2 of Form 1099-SA. You’ll owe income tax on the earnings, but not the 20% penalty (as long as you withdraw by the deadline).

Example: You contributed $5,000 to your HSA in 2025, but the limit for self-only coverage was $4,300. You over-contributed by $700. By April 15, 2026, you withdraw the $700 plus $35 in earnings. You’ll receive a 1099-SA showing $735 in Box 1 and $35 in Box 2. You owe income tax on the $35, but the $700 is not taxable (since you already paid tax on that income when you earned it).

You Used HSA Funds to Pay Health Insurance Premiums

In most cases, health insurance premiums are not qualified medical expenses for HSA purposes. However, there are four exceptions:

- COBRA continuation coverage premiums

- Qualified long-term care insurance premiums (subject to age-based limits)

- Health insurance premiums while receiving unemployment compensation

- Medicare premiums (Parts A, B, C, and D) if you’re 65 or older

If you used HSA funds to pay premiums that don’t fall into one of these categories, the distribution is non-qualified and subject to tax and penalty.

How KDA Can Help You Navigate Form 1099-SA Reporting

HSA tax planning is one of the most powerful tools for reducing lifetime tax liability, but only if you do it right. At KDA, we help self-employed professionals, small business owners, and W-2 employees maximize HSA benefits while staying compliant with IRS rules. Here’s how we can help you with Form 1099-SA reporting and overall tax planning services:

We Review Your HSA Distributions for Red Flags

Before you file your tax return, we review every distribution on your Form 1099-SA and cross-check it against your receipts. If we find non-qualified distributions, we calculate the tax impact and advise you on how to avoid penalties in future years.

We Optimize Your HSA Contribution Strategy

Most taxpayers max out their 401(k) contributions but ignore their HSA. That’s a mistake. HSA contributions are triple tax-advantaged: tax-deductible going in, tax-free growth, and tax-free distributions for medical expenses. We help you determine the optimal HSA contribution amount based on your income, family status, and health expenses.

We Prepare Form 8889 and Handle Complex Situations

If you had multiple HSAs, rolled over funds, over-contributed, or took distributions for both qualified and non-qualified expenses, Form 8889 gets complicated fast. We prepare it for you, ensuring every line is accurate and every deduction is maximized.

We Keep You Audit-Ready

In the rare event of an IRS audit, having clean records and proper documentation is the difference between a quick resolution and a multi-year nightmare. We help you organize your HSA receipts, EOB statements, and distribution records so you’re always audit-ready.

Ready to Reduce Your Tax Bill?

KDA Inc. specializes in strategic tax planning for business owners, S Corps, LLCs, and high-net-worth individuals. Book a personalized consultation and walk away with a clear plan.

Frequently Asked Questions About Form 1099-SA

Do I need to report Form 1099-SA if I only used HSA funds for medical expenses?

Yes. Even if 100% of your HSA distributions were for qualified medical expenses and you owe zero tax, you must still report Form 1099-SA on Form 8889 and attach it to your tax return. There is no exception to this rule. The IRS matches every 1099-SA to a corresponding Form 8889, and if yours is missing, you’ll get a notice.

What happens if I lose my receipts for HSA expenses?

If you’re audited and can’t provide receipts, the IRS will treat the distributions as non-qualified. You’ll owe income tax plus the 20% penalty (if under 65). To avoid this, keep digital copies of all receipts. Most HSA custodians let you upload and store receipts in your online account. Use that feature.

Can I take an HSA distribution in one year and claim it was for medical expenses from a prior year?

Yes, but be careful. You can reimburse yourself for qualified medical expenses incurred in any prior year, as long as the HSA existed when you incurred the expense. However, you must have receipts proving the expense was never reimbursed by insurance or paid from the HSA in a previous year. This is a common audit trigger, so documentation is critical.

What if my Form 1099-SA shows a distribution I didn’t take?

Contact your HSA custodian immediately. Errors happen, and if the form is incorrect, they will issue a corrected 1099-SA. Do not ignore it. If the IRS has a 1099-SA on file and you don’t report it, they’ll assume you owe taxes on the full amount.

Do I need to report HSA distributions if I’m 65 or older?

Yes, but the rules change slightly. If you’re 65 or older, you can take HSA distributions for any reason without the 20% penalty. However, if the distribution is for non-qualified expenses, you still owe income tax on the amount. Essentially, your HSA becomes like a traditional IRA once you turn 65. You still must file Form 8889 to report all distributions.

Book Your Tax Strategy Session

If you received Form 1099-SA and you’re not sure whether your distributions were qualified, or if you want to optimize your HSA strategy for future years, let’s talk. Our team specializes in helping self-employed professionals and small business owners navigate complex HSA rules, avoid penalties, and maximize tax savings. Click here to book your consultation now and get clear, compliant, and confident about your HSA tax reporting.

This information is current as of 3/28/2026. Tax laws change frequently. Verify updates with the IRS or your tax professional if reading this later.