When One Year Makes a $15,000 Difference

You bought Tesla stock in early 2024 for $40,000. It is now worth $95,000. You want to sell. Should you?

If you have held it for 364 days, selling today means the IRS treats that $55,000 gain as ordinary income. At the 32% federal bracket, you will hand over $17,600 in federal taxes alone. Add California’s 9.3% state rate, and you are looking at $22,715 in total taxes.

Wait one more day. Cross the 365-day threshold. That same $55,000 gain now qualifies for the long term vs short term gains preferential rate of 15% federal, cutting your federal bill to $8,250. Your total tax drops to $13,365. One extra day of patience saves you $9,350.

That is not a loophole. That is tax law working exactly as Congress designed it. And most investors leave tens of thousands on the table every year because they do not understand the timing rules.

Quick Answer

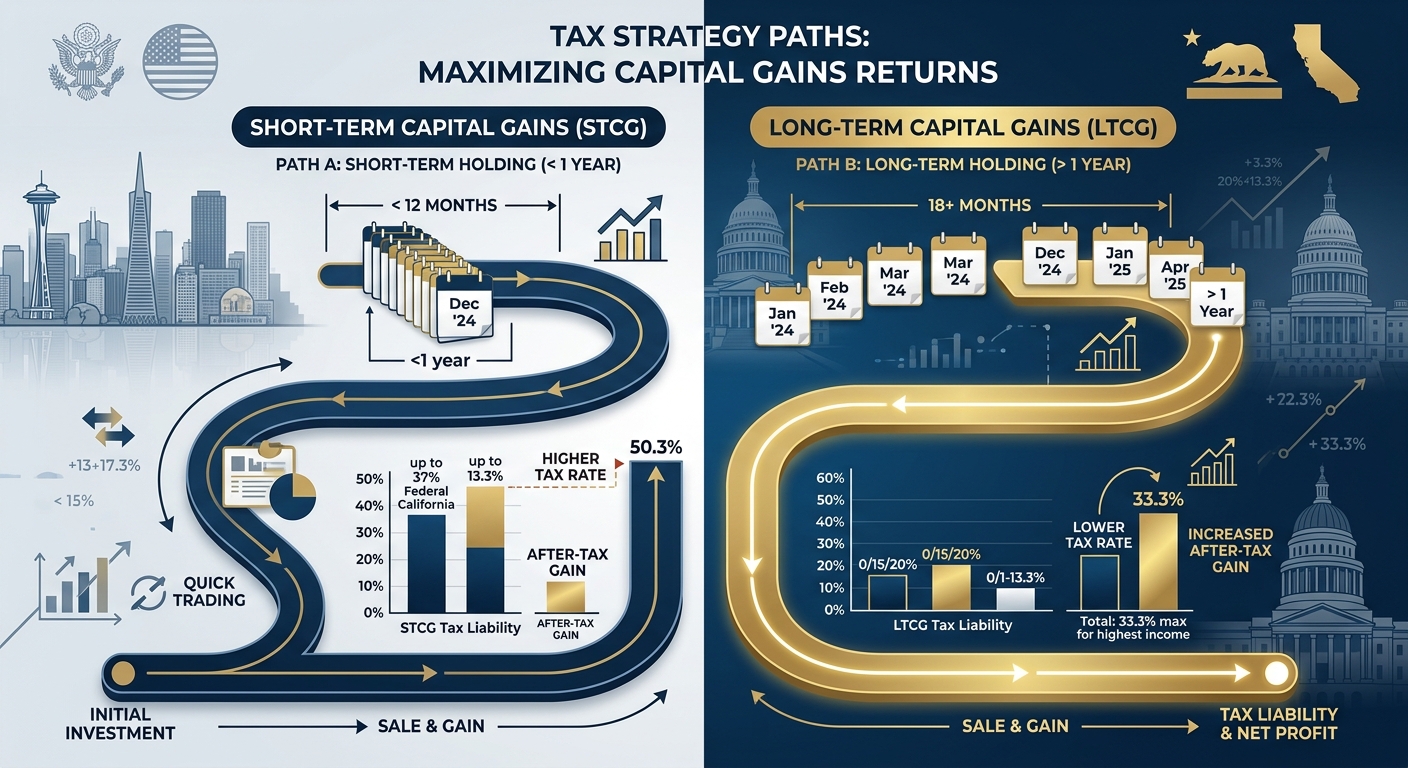

Long-term capital gains apply to assets held longer than one year and are taxed at 0%, 15%, or 20% federally, depending on income. Short-term capital gains apply to assets held one year or less and are taxed as ordinary income at rates up to 37% federally. California taxes both at the same ordinary income rates, ranging from 1% to 13.3%. The holding period clock starts the day after you purchase the asset and ends on the sale date.

What Counts as a Capital Gain?

A capital gain occurs when you sell an asset for more than you paid for it. The IRS uses the term “capital asset” broadly. It includes stocks, bonds, mutual funds, ETFs, real estate (primary residence, rental property, raw land), business interests (LLC units, S Corp shares, partnership interests), collectibles (art, coins, classic cars), and cryptocurrency (Bitcoin, Ethereum, NFTs).

Not everything qualifies as a capital asset. Inventory you sell as part of your business, property used in your trade (equipment, vehicles), and accounts receivable do not get capital gain treatment. Those get taxed as ordinary business income regardless of how long you hold them.

How the IRS Defines Your Holding Period

Your holding period starts the day after you acquire the asset and ends on the day you sell it. If you buy stock on March 15, 2025, your holding period begins March 16, 2025. To qualify for long-term treatment, you must sell on or after March 16, 2026.

The IRS does not round. There is no “close enough.” Day 364 is short-term. Day 366 is long-term. This rule applies to every capital asset, whether you bought $500 of Dogecoin or a $2 million commercial building.

Inherited assets get special treatment. If you inherit property, the IRS automatically treats it as long-term, regardless of how long you hold it after the person dies. This rule exists because you also receive a step-up in basis to the fair market value on the date of death, which wipes out any gains that occurred during the decedent’s lifetime.

Federal Tax Rates: The Math That Drives Every Sale Decision

The federal government taxes short-term and long-term capital gains at completely different rate structures. Short-term gains get added to your ordinary income and taxed at your marginal rate, which ranges from 10% to 37% in 2026. Long-term gains get their own preferential rate schedule.

2026 Federal Long-Term Capital Gains Rates

For single filers: 0% rate applies to taxable income up to $47,025, 15% rate applies to income from $47,026 to $518,900, and 20% rate applies to income above $518,900.

For married filing jointly: 0% rate applies to taxable income up to $94,050, 15% rate applies to income from $94,051 to $583,750, and 20% rate applies to income above $583,750.

These thresholds adjust annually for inflation. If your taxable income sits just below a threshold, selling a large position could push you into the next bracket. You might want to spread the sale across two tax years to stay in the lower bracket both times.

Short-Term Gains: Ordinary Income Treatment

Short-term capital gains do not get a special rate. The IRS adds them to your W-2 wages, 1099 income, business profit, rental income, and everything else. Then it applies the ordinary income tax brackets, which range from 10% to 37% in 2026.

If you are a $180,000 W-2 earner and you sell stock after 8 months for a $40,000 gain, that gain gets taxed at 24% or 32%, depending on where it lands in your bracket. You do not get the 15% long-term rate. You hand the IRS $9,600 to $12,800 on that $40,000 instead of the $6,000 you would pay if you had held another four months.

California Makes No Distinction

California does not recognize the difference between short-term and long-term capital gains. The state treats all capital gains as ordinary income and applies its graduated income tax rates, which range from 1% to 13.3% depending on your total taxable income.

If you are in California’s 9.3% bracket and you sell an asset for a $50,000 gain, the state takes $4,650 whether you held it for 6 months or 6 years. There is no preferential rate for patience. The Franchise Tax Board does not care about your holding period.

This creates a planning asymmetry. Federal law rewards you for holding longer. California law does not. For high earners in the state, this means your combined federal and state rate on long-term gains might be 15% + 13.3% = 28.3%, while your combined rate on short-term gains could be 37% + 13.3% = 50.3%. That 22-point spread makes timing critical.

California-Specific Scenarios

If you are a part-year California resident, the state only taxes gains on assets sold while you were a resident. If you moved to Nevada in June and sold your stock in August, California gets nothing. But if you sold in May before the move, California taxes the full gain at ordinary rates.

If you moved to California mid-year and then sold an asset you bought years earlier while living in Texas, California still taxes the entire gain as a resident. Your holding period for federal purposes remains intact, but California’s tax applies to the full amount because you were a resident on the sale date.

Real-World Example: Tech Employee RSU Vest and Sell

Maya is a senior engineer at a Bay Area tech company. She earns $220,000 in W-2 salary. In March 2025, 500 shares of her company stock vested. The shares were worth $150 per share on the vest date, so her employer reported $75,000 of ordinary income on her W-2 and withheld taxes. Her cost basis in those shares is now $150.

By March 2026, the stock has climbed to $240 per share. She wants to sell. She has two choices: sell now (364 days) or wait one more week.

Scenario 1: Sell at 364 days (short-term)

Sale proceeds: 500 shares x $240 = $120,000

Cost basis: 500 shares x $150 = $75,000

Gain: $45,000

Federal tax: 32% x $45,000 = $14,400

California tax: 9.3% x $45,000 = $4,185

Total tax: $18,585

Net after tax: $101,415

Scenario 2: Sell at 372 days (long-term)

Sale proceeds: $120,000 (assuming price holds)

Cost basis: $75,000

Gain: $45,000

Federal tax: 15% x $45,000 = $6,750

California tax: 9.3% x $45,000 = $4,185

Total tax: $10,935

Net after tax: $109,065

Waiting one week saves Maya $7,650. That is $7,650 she keeps by doing nothing but letting the calendar turn. If the stock drops 3% during that week, she still comes out ahead because the tax savings exceeds the price risk.

Investment Property: Where Holding Period Gets Complicated

Real estate follows the same one-year rule, but the calculation gets messier because of depreciation recapture. If you bought a rental property for $500,000 and claimed $50,000 in depreciation over five years, your adjusted basis is now $450,000. If you sell for $600,000, your total gain is $150,000.

The IRS splits that gain into two pieces. The $50,000 of depreciation you claimed gets recaptured and taxed at 25% federally (called unrecaptured Section 1250 gain). The remaining $100,000 of appreciation gets taxed at the long-term capital gains rate of 15% or 20%, depending on your income.

California taxes the entire $150,000 gain at ordinary income rates. If you are in the 9.3% California bracket, the state takes $13,950. Add federal tax of $12,500 (recapture) + $15,000 (long-term gain) = $27,500. Your total tax bill is $41,450.

If you had sold the property at 11 months instead of 5 years, the entire $150,000 gain would be short-term, taxed federally at 32% ($48,000) plus 9.3% California ($13,950) = $61,950. Holding past one year saved you $20,500 in federal tax alone.

1031 Exchange Timing Trap

Many real estate investors assume they can defer capital gains indefinitely through 1031 exchanges. That is true, but the exchange does not eliminate the short-term vs long-term distinction. It only defers recognition.

If you sell a property you have held for 10 months and complete a 1031 exchange, the gain is still short-term, even though you are not paying tax yet. If you later sell the replacement property without doing another exchange, the IRS will look back at the holding period of the relinquished property. You carry over the character of the gain.

The safer move: hold the property at least one year before entering the 1031 exchange. That locks in long-term treatment, so if you eventually sell the replacement property, you get long-term rates on the entire accumulated gain.

Red Flag Alert: Wash Sale Rule Resets Your Holding Period

If you sell stock at a loss and then repurchase the same or substantially identical security within 30 days before or after the sale, the IRS disallows the loss under the wash sale rule. What many investors miss: the wash sale rule also affects your holding period.

When you repurchase the stock, your holding period for the new shares does not start until the wash sale period ends. If you sold shares on March 1 at a loss and bought them back on March 10, your new holding period starts March 10, not March 1. This can turn what you thought was a long-term gain into a short-term gain if you are not careful.

Example: You bought 100 shares of Apple on June 1, 2025. On May 15, 2026, the stock drops, and you sell at a loss to harvest the tax benefit. On May 20, 2026, you rebuy the same shares because you still like the stock. You plan to sell on June 5, 2026, assuming you have held the stock more than a year.

Wrong. The wash sale rule resets your holding period to May 20, 2026. If you sell on June 5, 2026, you have only held the replacement shares for 16 days. That is a short-term gain, taxed at ordinary income rates. You just lost the 15% long-term rate because you repurchased too quickly.

Crypto and NFTs: No Special Treatment

The IRS treats cryptocurrency and NFTs as property, not currency. That means every time you sell, trade, or even spend crypto, you trigger a taxable event. The same short-term vs long-term rules apply.

If you bought 2 Bitcoin for $50,000 in January 2025 and sold them for $90,000 in November 2025, you have a $40,000 short-term capital gain. It gets taxed at your ordinary income rate. If you are in the 24% federal bracket, you owe $9,600 in federal tax, plus California’s 9.3% ($3,720) = $13,320 total.

If you held those same Bitcoin until February 2026 (more than one year), the federal rate drops to 15% ($6,000), and your total tax falls to $9,720. Waiting three extra months saves you $3,600.

Trading One Crypto for Another

Swapping Bitcoin for Ethereum is not a like-kind exchange. You cannot defer the gain. The IRS treats the swap as a sale of Bitcoin followed by a purchase of Ethereum. If you held the Bitcoin for less than a year, the gain is short-term. Your holding period for the Ethereum starts the day you receive it.

Day traders who move in and out of crypto positions every few weeks rack up short-term gains taxed at the highest rates. A $100,000 profit from day trading crypto in California could trigger $50,300 in combined federal and state tax (37% + 13.3%) if you are a high earner. The same $100,000 profit from holding Bitcoin for 13 months would cost $28,300 (15% + 13.3%).

KDA Case Study: Real Estate Investor

Marcus is a Sacramento-based real estate investor. He bought a single-family rental in Elk Grove for $420,000 in September 2024. By July 2025, the property had appreciated to $495,000. He received an unsolicited cash offer and was tempted to take the quick profit.

The $75,000 gain would have been short-term (only 10 months of ownership). At his 32% federal rate and 9.3% California rate, the tax would have been $31,000. After paying his $6,000 Realtor commission, his net would have been $38,000.

KDA advised Marcus to wait until October 2025 to close the sale. By holding just three more months, the gain became long-term. His federal rate dropped to 15%, cutting his federal tax from $24,000 to $11,250. His California tax remained $6,975. Total tax: $18,225 instead of $31,000. After the same $6,000 commission, his net increased to $50,775.

Marcus paid KDA $2,800 for the year’s tax planning and entity structuring. His first-year ROI was 4.5x. He reinvested the tax savings into his next rental acquisition and has since repeated the strategy on four additional properties.

Ready to see how we can help you? Explore more success stories on our case studies page to discover proven strategies that have saved our clients thousands in taxes.

Timing Strategies: When to Sell and When to Wait

If you are sitting on an unrealized gain and your holding period is about to cross one year, the default strategy is simple: wait. The tax savings from long-term treatment almost always exceeds the risk of a short-term price decline, especially for stable assets like index funds or blue-chip stocks.

If the asset is volatile (small-cap stock, speculative crypto, startup equity), you need to weigh the tax benefit against the downside risk. Saving 17% in taxes does not help if the asset drops 30% while you wait. In that case, sell now and take the short-term hit.

Harvesting Losses to Offset Gains

You can use capital losses to offset capital gains dollar-for-dollar. If you have $50,000 in long-term gains and $20,000 in short-term losses, you only pay tax on $30,000 of net gain. The losses apply against gains in this order: short-term losses first offset short-term gains, then long-term gains; long-term losses first offset long-term gains, then short-term gains.

If your losses exceed your gains, you can deduct up to $3,000 per year against ordinary income. The rest carries forward indefinitely. This creates a planning opportunity: if you know you will have a large gain in 2026, look for losing positions in your portfolio to sell before year-end to offset the gain.

Pro Tip: Pair short-term losses with short-term gains whenever possible. A short-term loss offsets a gain that would have been taxed at 37%, while a long-term loss only offsets a gain taxed at 15% or 20%. You get more value from the short-term loss.

What Happens If You Miss the One-Year Mark by a Day?

Nothing. There is no grace period. The IRS does not round up. If you sell on day 364, the entire gain is short-term, taxed at ordinary income rates. If you sell on day 366, the entire gain is long-term, taxed at the preferential rate.

This creates a hard cliff. Many investors lose thousands because they did not track the purchase date correctly. They think they bought the stock in “early March” but the actual trade settled March 18, not March 3. They sell on March 15 of the next year, assuming they cleared one year. They didn’t. The gain is short-term.

The solution: set a calendar reminder for the one-year anniversary of every significant asset purchase. If you buy $100,000 of Tesla stock on May 10, 2026, set a reminder for May 11, 2027. Do not sell before that date unless you are willing to pay the short-term rate.

Special Rules for Collectibles and Section 1202 Stock

Not all long-term capital gains get the 15% or 20% rate. Collectibles (art, coins, stamps, antiques, precious metals) get taxed at a maximum 28% federal rate, even if you hold them for more than one year. California still taxes them at ordinary income rates.

Qualified small business stock under Section 1202 gets even better treatment. If you hold stock in a C corporation with gross assets under $50 million for more than five years, you can exclude up to $10 million of gain or 10 times your basis, whichever is greater. The excluded gain pays zero federal tax. California does not recognize the exclusion and taxes the full gain at ordinary rates, but eliminating the federal tax still saves 20% to 37% on the gain.

Section 1202 has strict requirements: the stock must be original issue (not purchased from another shareholder), the corporation must be a C corp (not an S corp or LLC), and the corporation must use at least 80% of its assets in an active trade or business. If you qualify, the five-year holding period becomes critical. Selling at four years and 364 days costs you the exclusion.

How Gifting Affects Holding Period

If you gift an appreciated asset to someone else, the recipient takes over your holding period. If you bought stock two years ago and you gift it to your daughter today, her holding period includes your two years. If she sells it next week, she gets long-term treatment.

But the recipient also takes over your basis. If you paid $10,000 for the stock and it is now worth $30,000, your daughter’s basis is $10,000. When she sells for $30,000, she pays tax on the $20,000 gain.

Gifting works well for shifting income to lower-bracket family members. If you are in the 37% federal bracket and your adult child is in the 12% bracket, gifting appreciated stock to them and having them sell it can save 25 percentage points in federal tax. California tax applies based on the recipient’s residency, so if your child lives in Nevada or Texas (no state income tax), you eliminate the California 13.3% as well.

Kiddie Tax Rules Limit This Strategy

If the recipient is under 19 (or under 24 and a full-time student), the kiddie tax applies. Unearned income above $2,600 (2026 threshold) gets taxed at the parent’s marginal rate, not the child’s rate. That eliminates the bracket arbitrage. Gifts to minor children only make sense if the gain is small enough to stay under the kiddie tax threshold.

Installment Sales: Spreading Gain Over Multiple Years

If you sell property and finance part of the sale yourself (the buyer pays you over time instead of getting a bank loan), you can use installment sale treatment. This lets you recognize the gain as you receive payments, rather than all at once in the year of sale.

The character of the gain (short-term or long-term) is determined by your holding period at the time of sale. If you held the property for three years, the gain is long-term, even though you receive the payments over the next five years. Each payment you receive includes a portion of gain, which gets taxed at the long-term rate.

Installment sales work well when you want to avoid a large one-time tax hit. If you sell a rental property for $800,000 with a $300,000 gain, recognizing the full gain in one year could push you into the 20% long-term capital gains bracket and trigger the 3.8% net investment income tax. By spreading the gain over four years, you might stay in the 15% bracket each year and avoid the additional 3.8% surtax, saving $11,400 in federal tax.

Ready to Reduce Your Tax Bill?

KDA Inc. specializes in strategic tax planning for business owners, S Corps, LLCs, and high-net-worth individuals. Book a personalized consultation and walk away with a clear plan.

Frequently Asked Questions

Can I Convert a Short-Term Gain to Long-Term by Waiting to Settle the Trade?

No. The IRS uses trade date, not settlement date. If you place a sell order on day 364 and the trade settles three days later on day 367, the gain is still short-term. The clock stops on the trade date, which is the day your order executes.

Does the Holding Period Reset If I Move Shares from One Brokerage to Another?

No. Transferring shares between your own accounts (moving from Fidelity to Schwab) is not a sale. Your holding period continues uninterrupted. The original purchase date carries over to the new account.

What If I Inherit Property and Sell It the Next Month?

Inherited property is automatically long-term, regardless of how long you hold it. If your father bought the house in 2020, passed away in 2026, and you sell it 30 days later, the gain is long-term. You also get a step-up in basis to the fair market value on the date of death, which often eliminates or reduces the taxable gain.

Do Short-Term Losses Offset Long-Term Gains?

Yes. The IRS lets you use any type of capital loss to offset any type of capital gain. If you have $50,000 in long-term gains and $30,000 in short-term losses, your net taxable gain is $20,000, taxed at long-term rates. The short-term loss wipes out $30,000 of the long-term gain.

Does California Offer Any Capital Gains Breaks?

No. California taxes all capital gains as ordinary income. There is no preferential rate for long-term gains. The state does allow you to carry forward capital losses indefinitely, just like the IRS, and you can use up to $3,000 per year to offset ordinary income.

Book Your Tax Strategy Session

If you are sitting on unrealized gains and you are not sure whether to sell now or wait, the tax cost of guessing wrong is real. A single mistimed sale can cost you thousands in unnecessary taxes. Book a personalized consultation with our strategy team and get a clear plan for your specific situation. We will walk you through your holding periods, project your tax liability under different scenarios, and show you exactly when to sell to keep the most money in your pocket. Click here to book your consultation now.

This information is current as of 3/21/2026. Tax laws change frequently. Verify updates with the IRS or FTB if reading this later.