What Is Withheld From Your Paycheck? The Complete Breakdown

You land your first serious W-2 job. The offer letter says $75,000 a year. You do the math and figure that’s $6,250 per month, enough to finally move out of your cramped apartment and start building real wealth. Then your first paycheck hits: $4,487. Where did the other $1,763 go?

The answer is what is withheld from every paycheck you earn as a W-2 employee. Most workers watch 25% to 35% of their gross income vanish before they ever see a cent of it. But here’s the part that stings: many taxpayers have no idea what they’re actually paying for, whether it’s correct, or how to fix it when the government is taking too much.

Quick Answer

What is withheld refers to the mandatory taxes and voluntary deductions your employer removes from your gross pay before issuing your net paycheck. Federal income tax, Social Security, Medicare, state income tax, and any voluntary contributions to retirement accounts or health insurance are all withheld automatically. The exact amount depends on your income level, filing status, and the information you provided on Form W-4.

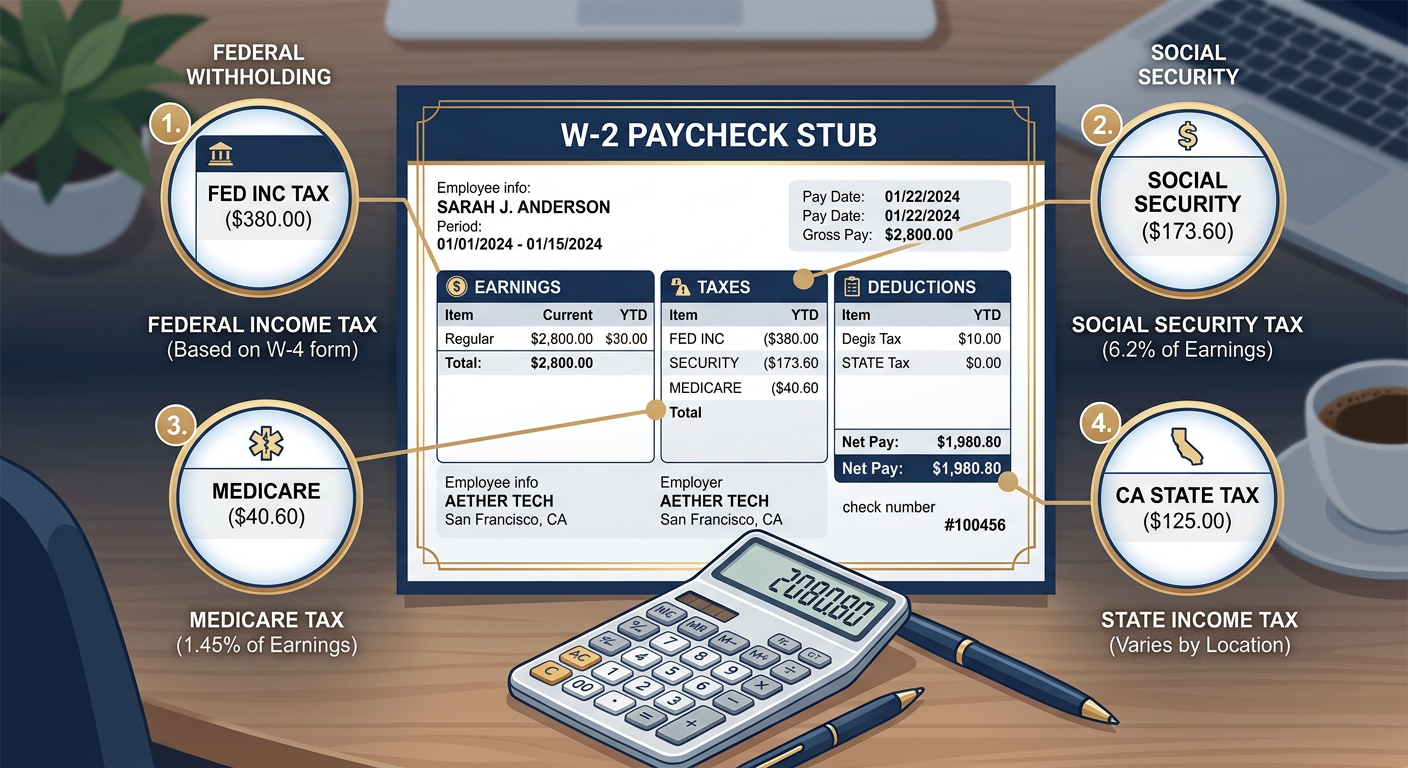

The Five Core Withholdings Every W-2 Employee Pays

Understanding what is withheld starts with breaking down the five primary categories that drain your paycheck every pay period. These aren’t suggestions or optional contributions. They’re mandatory deductions enforced by federal and state law, calculated based on your income and the elections you made when you started your job.

1. Federal Income Tax Withholding

Federal income tax is the largest single withholding for most workers. Your employer calculates this based on the W-4 form you filled out when you were hired. The IRS uses a progressive tax bracket system, which means the more you earn, the higher percentage you pay on the top portion of your income.

For 2026, a single filer earning $75,000 annually falls into the 22% marginal tax bracket. But you don’t pay 22% on all $75,000. You pay 10% on the first $11,600, 12% on income between $11,600 and $47,150, and 22% on everything above $47,150. Your employer uses IRS withholding tables to estimate this and pulls it from every check.

The key variable here is your W-4. If you claimed zero allowances and requested extra withholding, you’ll see a larger federal income tax deduction. If you claimed dependents or additional credits, you’ll see less taken out. Most people treat their W-4 like a set-it-and-forget-it document, but it’s one of the most powerful tools you have to control cash flow and avoid surprise tax bills.

Pro Tip: Run your paycheck through the IRS Tax Withholding Estimator every year to make sure you’re not massively overpaying and giving the government an interest-free loan.

2. Social Security Tax (FICA)

Social Security tax is a flat 6.2% on all wages up to $176,100 in 2026. Once you hit that cap, Social Security withholding stops for the rest of the year. If you earn $75,000, you’ll pay $4,650 annually in Social Security taxes, or $193.75 per biweekly paycheck.

This is not negotiable. It doesn’t matter what you put on your W-4 or how many dependents you claim. Social Security tax is a fixed percentage that funds the federal Social Security program, which provides retirement and disability benefits. Your employer matches your 6.2% contribution dollar-for-dollar, bringing the total to 12.4%, though you never see their half.

3. Medicare Tax (FICA)

Medicare tax is another flat 1.45% on all wages with no income cap. Unlike Social Security, there’s no ceiling. If you earn $75,000, you pay $1,087.50 per year in Medicare taxes. If you earn $500,000, you pay $7,250 plus an additional 0.9% on income over $200,000 (or $250,000 for married couples filing jointly), thanks to the Additional Medicare Tax introduced under the Affordable Care Act.

Your employer also matches your 1.45% contribution, bringing the total Medicare tax to 2.9% on all wages. High earners pay an extra 0.9% on income above the threshold, but there’s no employer match on that additional amount.

4. State Income Tax Withholding

State income tax withholding depends entirely on where you live. California residents face some of the highest state tax rates in the country, with a top marginal rate of 13.3%. A single filer earning $75,000 in California will pay approximately 9.3% in state income tax, or around $6,975 annually.

Other states like Texas, Florida, Nevada, and Washington have no state income tax at all. If you live in one of these states, you skip this withholding entirely. But if you live in California, New York, New Jersey, or any other high-tax state, state income tax withholding can rival or exceed your federal withholding, especially at higher income levels.

Your employer calculates state withholding based on the state equivalent of the federal W-4. In California, that’s the DE 4 form. Just like with federal withholding, you can adjust your state withholding allowances to increase or decrease the amount taken from each paycheck.

5. Voluntary Withholdings and Pre-Tax Deductions

Beyond mandatory tax withholdings, most employees also have voluntary deductions taken from their paychecks. These include contributions to employer-sponsored retirement plans like a 401(k), health insurance premiums, HSA contributions, FSA elections, and sometimes life or disability insurance premiums.

The advantage of pre-tax deductions is that they reduce your taxable income. If you contribute $500 per month to your 401(k), that $500 comes out before federal and state income taxes are calculated, which lowers your overall tax burden. You still pay Social Security and Medicare taxes on that income, but you defer federal and state income tax until you withdraw the money in retirement.

For a W-2 employee earning $75,000 who contributes 10% to a 401(k), that’s $7,500 per year in pre-tax contributions, which drops taxable income to $67,500. That alone can save $1,650 in federal taxes and another $697 in California state taxes annually.

How to Calculate What Is Withheld From Your Paycheck

Let’s walk through a real-world example using a single filer in California earning $75,000 per year, paid biweekly (26 pay periods). Here’s the step-by-step breakdown of what gets withheld from each paycheck:

Gross Pay Per Paycheck: $75,000 / 26 = $2,884.62

Step 1: Calculate Federal Income Tax Withholding

Using the 2026 IRS withholding tables for a single filer claiming standard deduction with no dependents:

- Estimated federal withholding: $385 per paycheck

- Annual federal withholding: $10,010

Step 2: Calculate Social Security Tax

Social Security is a flat 6.2% on all wages up to the annual cap:

- $2,884.62 x 6.2% = $178.85 per paycheck

- Annual Social Security tax: $4,650

Step 3: Calculate Medicare Tax

Medicare is a flat 1.45% on all wages with no cap:

- $2,884.62 x 1.45% = $41.83 per paycheck

- Annual Medicare tax: $1,087.50

Step 4: Calculate California State Income Tax

Using California’s progressive tax brackets for a single filer:

- Estimated state withholding: $268 per paycheck

- Annual California state tax: $6,968

Step 5: Subtract Voluntary Deductions

If this employee contributes 10% to a 401(k):

- $2,884.62 x 10% = $288.46 per paycheck

- Annual 401(k) contribution: $7,500

Total Withholdings Per Paycheck

Adding it all up:

- Federal income tax: $385

- Social Security: $178.85

- Medicare: $41.83

- California state tax: $268

- 401(k) contribution: $288.46

- Total withheld: $1,162.14

Net Pay Per Paycheck: $2,884.62 – $1,162.14 = $1,722.48

That’s a take-home rate of 59.7%. This employee is losing 40.3% of their gross income to withholdings before they ever see the money. Over the course of a year, they take home $44,784.48 out of $75,000 in gross earnings.

Why Your W-4 Is the Most Important Form You’ll Ever Fill Out

The W-4 is not a static document. It’s a living, breathing tool that directly controls how much cash you see in every paycheck versus how much the IRS holds onto throughout the year. Most employees fill it out once on their first day of work and never look at it again. That’s a mistake that costs thousands of dollars in lost cash flow or surprise tax bills.

Understanding the 2020 W-4 Redesign

In 2020, the IRS completely redesigned the W-4 form. The old system used “allowances” where you could claim 0, 1, 2, or more allowances to control withholding. The new form eliminated allowances and replaced them with a more straightforward approach based on your filing status, number of dependents, and any additional income or deductions you expect.

The new W-4 has five sections:

- Step 1: Enter your personal information and filing status

- Step 2: Account for multiple jobs or a working spouse

- Step 3: Claim dependents and the Child Tax Credit

- Step 4: Make additional adjustments for other income, deductions, or extra withholding

- Step 5: Sign and date the form

Only Step 1 and Step 5 are required. Everything else is optional, but those optional sections are where you gain control over your withholding strategy.

When to Update Your W-4

Life changes, and so should your W-4. Here are the events that should trigger an immediate W-4 review and update:

- You get married or divorced

- You have a child or gain a dependent

- You start a side business or 1099 income stream

- You buy a home and start paying mortgage interest

- Your spouse starts or stops working

- You receive a significant raise or bonus

- You get a massive tax refund (you’re overpaying all year)

- You owe a large tax bill at filing (you’re underpaying)

If you received a $5,000 tax refund last year, you essentially gave the government an interest-free loan of $416 per month. You could have invested that money, paid down debt, or built an emergency fund instead. Adjusting your W-4 to reduce withholding puts that cash back in your pocket every pay period.

Red Flag Alert: If you consistently owe $1,000 or more at tax time, the IRS may assess underpayment penalties. The safe harbor rule requires you to pay at least 90% of your current year tax liability or 100% of your prior year tax liability (110% if your adjusted gross income exceeds $150,000) to avoid penalties.

What Happens If Too Much Is Withheld?

When your employer withholds more tax than you actually owe, you get a refund when you file your tax return. Sounds great, right? Not exactly. A large refund means you’ve been underpaid all year. That’s money you could have used to invest, pay off high-interest debt, or cover living expenses.

The average tax refund in 2026 is projected to be around $3,200 according to IRS data. That’s $266 per month of your own money that the government held onto interest-free. If you had invested that $266 monthly in an index fund earning 8% annually, you’d have an extra $3,315 at year-end instead of just getting your $3,200 back with zero interest.

How to Reduce Over-Withholding

If you consistently receive large refunds, here’s how to fix it:

- Use the IRS Tax Withholding Estimator at IRS.gov to calculate your ideal withholding

- Submit a new W-4 to your employer reducing your withholding by claiming dependents or adjusting Step 4

- Monitor your paychecks for 2-3 pay periods to ensure the adjustment is correct

- Re-check mid-year to make sure you’re on track

You’re not locked into your W-4 selection. You can change it as often as you want throughout the year. If you realize in July that you’re overpaying, submit a new W-4 immediately and keep more of your money for the rest of the year.

What Happens If Too Little Is Withheld?

On the flip side, if your employer withholds too little, you’ll owe money when you file your tax return. This is common for taxpayers with multiple income sources, self-employment income, significant investment income, or those who claim too many credits or deductions on their W-4.

Owing at tax time isn’t necessarily bad if you planned for it and set money aside. The problem is when taxpayers are surprised by a $5,000 tax bill they weren’t expecting and don’t have the cash to pay.

IRS Underpayment Penalties

If you owe more than $1,000 at filing and didn’t meet the safe harbor withholding requirements, the IRS will assess an underpayment penalty. For 2026, the penalty rate is tied to the federal short-term rate plus 3%, which currently works out to around 8% annually.

The safe harbor rules protect you from penalties if you meet one of these two conditions:

- You paid at least 90% of the tax owed for the current year through withholding or estimated payments

- You paid at least 100% of the tax shown on your prior year’s return (110% if your AGI exceeded $150,000)

If you realize mid-year that you’re under-withheld, you can either increase your W-4 withholding for the rest of the year or make estimated tax payments using Form 1040-ES to avoid penalties.

California-Specific Withholding Considerations

California has its own set of withholding rules that layer on top of federal requirements. The state’s progressive tax system means high earners face significantly higher withholding rates than residents of low-tax or no-tax states.

The SALT Deduction Cap and California Taxpayers

The State and Local Tax (SALT) deduction cap was a major hit to California taxpayers when it was introduced in 2017. The cap limited the federal deduction for state and local taxes to $10,000 per year. For California residents paying $15,000 or more in state income and property taxes, this meant losing a valuable federal deduction.

However, the One, Big, Beautiful Bill Act passed in 2025 raised the SALT cap to $40,000 for married couples filing jointly and $20,000 for single filers, effective for the 2025 tax year. This is a game-changer for California homeowners and high earners who were previously capped at $10,000.

If you’re a California resident who itemizes deductions, the increased SALT cap could save you $1,500 to $3,000 or more in federal taxes. However, this doesn’t affect your withholding unless you update your W-4 to account for the additional deduction in Step 4.

California DE 4 Form

California uses the DE 4 form instead of the federal W-4 to determine state income tax withholding. Like the federal form, you can adjust your California withholding by claiming allowances or requesting additional withholding.

One quirk of California withholding: if you work remotely for an out-of-state employer, your employer may not automatically withhold California state taxes. In that case, you’re responsible for making estimated tax payments to California’s Franchise Tax Board (FTB) using Form 540-ES.

Pro Tip: If you moved to California mid-year or started working remotely for a California employer, double-check that state withholding is set up correctly. The FTB is aggressive about collecting unpaid taxes and will assess penalties and interest on late payments.

Common Withholding Mistakes That Cost You Money

Most taxpayers don’t intentionally make withholding mistakes. They simply don’t understand how the system works or fail to update their W-4 when their financial situation changes. Here are the five most expensive mistakes and how to avoid them:

Mistake 1: Never Updating Your W-4 After Major Life Events

Getting married, having a child, buying a home, or starting a side business all change your tax picture significantly. If you don’t update your W-4 to reflect these changes, you’ll either massively overpay (and get a huge refund) or underpay (and owe at filing).

Mistake 2: Claiming Exempt When You Don’t Qualify

Some employees claim “exempt” on their W-4 to avoid withholding entirely. This is legal only if you had no tax liability last year and expect no tax liability this year. For most workers, claiming exempt is a fast track to a large tax bill and penalties.

Mistake 3: Forgetting About Side Income

If you earn 1099 income from freelancing, consulting, or a side business, your employer has no idea. Your W-4 withholding is based solely on your W-2 wages. You need to either increase your W-4 withholding to cover the additional tax on your side income or make quarterly estimated tax payments.

Mistake 4: Ignoring State Withholding

Federal withholding is important, but state withholding can be just as significant, especially in high-tax states like California. If you adjust your federal W-4 but forget to update your state DE 4, you’ll end up with a surprise state tax bill.

Mistake 5: Treating Your Refund Like a Savings Account

A tax refund is not free money. It’s your own money that you overpaid throughout the year. If you’re relying on your refund to pay off holiday debt or fund a vacation, you’re essentially forcing yourself to save by overpaying taxes. That’s an expensive and inefficient way to build savings.

KDA Case Study: W-2 Engineer Saves $4,200 by Optimizing Withholding

Meet James, a 32-year-old software engineer earning $110,000 per year at a tech company in San Francisco. James had been receiving tax refunds of $4,500 to $5,000 every year and thought that was a good thing. He treated his refund like forced savings and used it to pay off credit card debt and fund his annual vacation.

When James came to KDA for a tax strategy consultation, we ran his withholding through the IRS estimator and discovered he was overpaying by nearly $400 per month. We helped him submit a new W-4 that reduced his federal withholding by claiming the correct number of dependents and accounting for his student loan interest deduction and 401(k) contributions.

The result? James kept an extra $385 per paycheck, or $10,010 annually. We advised him to automate that extra $385 into a high-yield savings account earning 4.5%, which generated an additional $225 in interest over the course of the year. Instead of giving the government an interest-free loan, James earned money on his own cash.

By the following April, James received a small refund of $250 instead of $4,500, which meant his withholding was nearly perfect. He paid KDA $1,200 for the consultation and ongoing tax planning support, resulting in a first-year net gain of $3,035 and improved cash flow for years to come.

Ready to see how we can help you? Explore more success stories on our case studies page to discover proven strategies that have saved our clients thousands in taxes.

How Self-Employed Workers Handle Withholding Differently

If you’re self-employed or earn 1099 income, there’s no employer withholding taxes for you. You’re responsible for calculating and paying your own taxes through quarterly estimated tax payments using Form 1040-ES.

Self-employed workers pay both the employee and employer portions of Social Security and Medicare taxes, known as self-employment tax. That’s 15.3% on net self-employment income (12.4% for Social Security up to the wage cap and 2.9% for Medicare with no cap). On top of that, you owe federal and state income taxes.

For self-employed individuals, the key to avoiding penalties is making quarterly estimated tax payments by these deadlines:

- Q1: April 15, 2026

- Q2: June 16, 2026

- Q3: September 15, 2026

- Q4: January 15, 2027

If you have both W-2 income and self-employment income, you can increase your W-4 withholding to cover the tax on your side income instead of making separate estimated payments. This simplifies your tax compliance and ensures you’re paying as you go.

Many self-employed workers we work with at KDA benefit from our tax planning services, which include quarterly check-ins, estimated tax calculations, and proactive strategies to minimize tax liability throughout the year.

Ready to Reduce Your Tax Bill?

KDA Inc. specializes in strategic tax planning for business owners, S Corps, LLCs, and high-net-worth individuals. Book a personalized consultation and walk away with a clear plan.

Frequently Asked Questions About Withholding

Can I change my W-4 withholding at any time during the year?

Yes. You can submit a new W-4 to your employer as often as you want. There’s no limit on how many times you can adjust your withholding. Most payroll systems will apply your new W-4 within one to two pay periods after submission.

What happens if I don’t fill out a W-4?

If you don’t submit a W-4, your employer is required to withhold taxes at the highest rate, which is single filer with no adjustments. This typically results in significant over-withholding and a large refund when you file.

How do bonuses and commissions affect withholding?

Bonuses and commissions are considered supplemental wages and are typically withheld at a flat 22% federal rate (or your marginal rate if the bonus exceeds $1 million). State withholding on bonuses varies by state. California withholds bonuses at a flat 10.23% rate. This withholding is often higher than your actual tax liability, which means you’ll get some of it back as a refund when you file.

Do I have to pay taxes on my employer’s 401(k) match?

No. Your employer’s 401(k) match is not included in your taxable income in the year it’s contributed. You’ll pay taxes on both your contributions and your employer’s contributions when you withdraw the money in retirement. However, you do pay Social Security and Medicare taxes on your own contributions in the year they’re made.

What if I work in one state but live in another?

If you work in one state and live in another, you may be subject to withholding in both states. Most states have reciprocal agreements that prevent double taxation, but you’ll need to file tax returns in both states and claim a credit for taxes paid to the non-resident state. This gets complicated quickly, which is why many cross-border workers benefit from professional tax planning support.

Take Control of Your Withholding Strategy

Understanding what is withheld from your paycheck is the first step toward taking control of your cash flow and tax strategy. Too many employees treat withholding as something that just happens automatically without realizing they have the power to adjust it.

Whether you’re over-withholding and giving the government an interest-free loan or under-withholding and setting yourself up for a surprise tax bill, the solution is the same: review your W-4, use the IRS withholding estimator, and make adjustments that align with your actual tax liability.

Your paycheck is your biggest wealth-building tool. Don’t let poor withholding strategy drain thousands of dollars every year.

This information is current as of 3/6/2026. Tax laws change frequently. Verify updates with the IRS or FTB if reading this later.

Optimize Your Tax Withholding and Keep More of Your Paycheck

If you’re tired of watching 30% to 40% of your paycheck disappear and want a clear, personalized strategy to optimize your withholding, it’s time to talk to a tax professional who understands W-2 withholding, self-employment tax, and California state tax rules. Book a consultation with KDA’s tax strategy team and get a customized withholding plan that maximizes your cash flow without triggering IRS penalties. Click here to book your consultation now.