Gift Tax, Charitable Remainder Trusts, and the California Playbook: How the New Rules Are Changing High-Net-Worth Giving in 2026

This information is current as of 2/3/2026. Tax laws change frequently. Verify updates with the IRS or FTB if reading this later.

Most wealthy Californians want their charitable gifts to do double duty: help a cause, minimize estate tax, and keep gift taxes at bay. But too many fall into the trap of thinking a charitable remainder trust (CRT) is an automatic shield from the IRS’s new scrutiny—especially after the changes that hit in 2026. In reality, the wrong move with gift reporting or compliance can create a six-figure tax bill no one sees coming.

Quick Answer

A CRT lets you donate appreciated assets, defer capital gains, and send the remainder to a charity when the term ends. If structured correctly, you receive an immediate charitable deduction and bypass gift tax on most transfers. But with the IRS tightening enforcement and California’s pending Billionaire Tax, every CRT participant needs airtight documentation and a compliance-first gifting plan before moving a dollar.

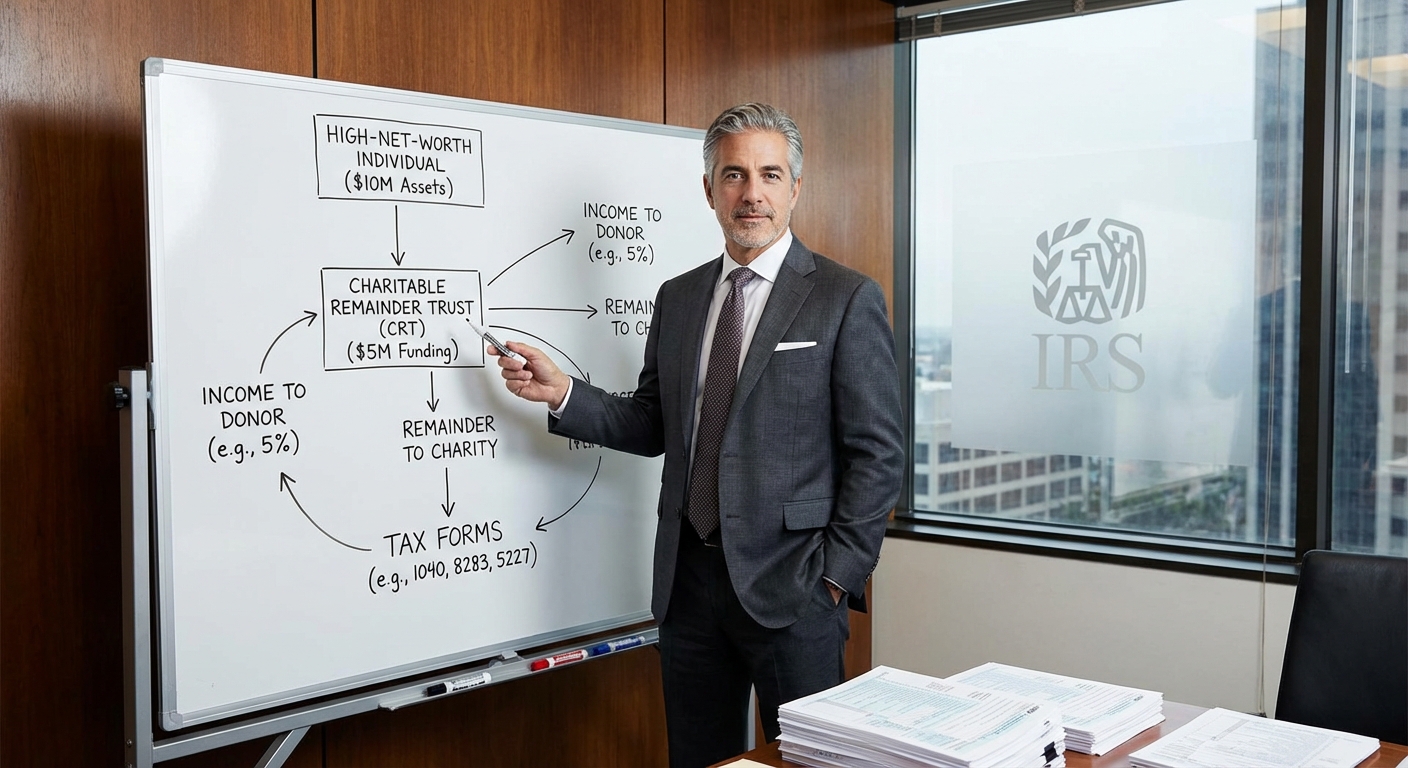

A properly structured gift tax charitable remainder trust is not a blanket exemption—it’s a valuation exercise governed by IRS actuarial tables under IRC §664. Only the portion projected to pass to the qualified charity is excluded from gift tax; any income interest granted to family members must be measured and reported on Form 709. High-net-worth donors get into trouble when they assume “charitable” automatically means “non-taxable.”

Decoding Gift Tax: What Actually Triggers a Bill in 2026?

The federal gift tax kicks in if you transfer more than the annual exclusion ($18,000 per recipient in 2026, per IRS guidance). Exceed the lifetime exemption—$13.61 million as of 2026—and you owe 40% tax on the excess. California piggybacks on federal rules for estate and gift tax, but there are two new angles for high-net-worth and business clients this year:

- Enhanced IRS scrutiny of gifting before expatriation or major asset moves—disclosures on Form 709 and Form 8854 are now cross-reviewed

- CA’s proposed Billionaire Tax Act (pending 2026), pushing more wealthy donors to deploy CRTs and other structures quickly

Simple scenario: Linda gifts $1M in Tesla stock outright to her child and files Form 709. That counts toward her $13.61M exemption. Gift tax only applies post-threshold. But if she gifts to a CRT, she could get a partial charitable deduction and delay or avoid direct gift tax, provided every transfer is documented and IRS-accepted.

When evaluating a gift tax charitable remainder trust, the IRS focuses on how much value leaves your taxable estate today—not the headline asset amount. The charitable remainder reduces your taxable gift, but retained annuity or unitrust payments are treated as a transfer to non-charity beneficiaries and can consume lifetime exemption. This distinction is critical for donors hovering near the $13.61M exemption cap.

What Assets Can You Place in a CRT?

- Highly appreciated public stock (most common)

- Privately held business interests (with more complexity)

- Commercial or residential real estate, including rental property

- Crypto and even alternative assets (but compliance hurdles are higher for nontraditional assets)

To get full IRS and California credit, the CRT’s payout, beneficiary, and remainder values must be calculated by a qualified appraiser and funded before liquidation. Otherwise, audits spike.

For a full breakdown of current estate and gifting strategies, see our California estate and legacy planning guide.

How a Charitable Remainder Trust Sidesteps Gift Tax—If Done Right

A CRT lets you gift assets, claim a deduction, and send future income or principal to family or yourself for a set term (or life), with the rest passing to a named charity. The IRS allows an immediate charitable deduction based on the present value the charity is expected to receive, reducing your taxable gift exposure.

The strategic value of a gift tax charitable remainder trust lies in precision, not generosity. IRS Section 7520 rates, payout percentages, and term length directly affect how much of the transfer escapes gift tax today versus how much is treated as a future family gift. Slight miscalculations—especially with long-term or multi-beneficiary CRTs—are a common audit trigger in 2026.

Example: Eric, a real estate investor, moves $2.5M of appreciated stock into a CRT. He receives a $960,000 charitable deduction (per IRS tables and Sec. 664 calculations) on his 2026 return, pays no capital gains at transfer, and future growth remains untaxed inside the CRT. If Eric’s family receives annuity payments, only the non-charity share may count as a gift—if structured and reported properly, this can sharply reduce total gift tax owed.

California’s high-net-worth legal and finance professionals should note: multi-generational CRTs, when combined with annual gifting, can shield $1M–$4M in appreciated assets per trust from both gift and estate tax in a typical structure.

Mandatory Steps for CRT and Gift Tax Compliance in 2026

- Get a qualified appraisal before funding the CRT (especially for non-cash assets)

- File Form 709 for any non-charity gift component in the CRT structure

- Provide evidence of irrevocable transfer, trust IRS recognition, and 501(c)(3) charity eligibility

- Prepare annual trust tax returns (Form 5227) and recipient income reporting

Failing any of these steps risks audit and retroactive gift tax assessment.

Our tax planning services cover the entire CRT pipeline, from legal formation and IRS filings to annual tracking.

KDA Case Study: High-Net-Worth Investor Shields $1.8M With CRT Planning

Sophia, a Bay Area entrepreneur and pre-exit startup owner, faced a $3.2M capital gain on the sale of her private shares at age 57. A direct gift to her adult children would have eaten into her $13.61M lifetime exclusion, potentially triggering future gift or estate tax if the company grew. Instead, Sophia worked with the KDA team to:

- Transfer $2M in illiquid shares to a 20-year term CRT, naming her children as income beneficiaries for 15 years with a qualified 501(c)(3) as the final remainder beneficiary

- Obtain a $890,000 immediate charitable deduction (as calculated by IRS rates and actuarial tables)

- Spread $1.2M in income payments over 15 years, with most of it received as capital gains income at the children’s lower tax rates

- Keep nearly $1.8M outside the immediate reach of gift and estate taxation, with audit-proof documentation and IRS approval

- Pay $15,500 in legal, appraisal, and tax advisory fees for a 57x ROI in tax savings and deduction value

Ready to see how we can help you? Explore more success stories on our case studies page to discover proven strategies that have saved our clients thousands in taxes.

Donor-Advised Funds, K-12 Gift Credits, and CRTs: The 2026 Shifting Landscape

Charitable strategies are evolving fast in 2026, especially for donors at or above the California net worth threshold for the proposed Billionaire Tax. Major trends for wealthy and upper-middle-class taxpayers:

- Surge in donor-advised fund (DAF) gifts—utilize appreciated stock, real estate, or even crypto to maximize deductions quickly before tax law sunsets (per CNBC and multiple studies)

- Advance funding multiple years of DAF or CRT giving before the 2026/2027 deduction changes phase in

- New $1,700 K-12 education scholarship credit for donations starting in 2027—federal credit, not just deduction (per Chronicle of Philanthropy)

- Heightened IRS tracking on pre-expatriation gifts and CRT strategies—especially with new Form 8854 disclosure requirements

If you want to estimate your federal savings, use a capital gains tax calculator to project deduction value from your largest appreciated assets before CR trust funding.

For Business Owners and Real Estate Investors

If you’re a business owner shifting assets pre-sale or a real estate investor planning for 2026, multi-layer gifting (CRT plus annual exclusion gifts plus lifetime trusts) can combine for 30–50% greater tax efficiency versus direct giving alone. It’s now much harder to rely on backdated gifts or post-hoc appraisals—the IRS and FTB both match reported asset movement on federal and CA filings.

Why Most Donors Miss the Gift Tax Trap in CRTs

Common mistake: assuming that any asset transferred into a CRT is 100% gift-tax free or deductible. If non-charity beneficiaries (children, spouses, business partners) receive payout rights, only the remainder to charity is deductible. Failure to separate these values, report them on Form 709, or get an independent appraisal results in IRS-flagged returns, dollar-for-dollar back taxes, and, in California, possible FTB audit if the property is CA-based.

Red Flag Alert: The IRS has updated Form 8854 to require detailed disclosure of any CRT-funding, asset transfers, or substantial asset movement in the five years preceding expatriation (for those planning to move abroad). Attempting to “zero-out” net worth with clever gifting now requires a paper trail the IRS can—and will—inspect (see Forbes offshore enforcement analysis).

How Do I Know If My CRT Is IRS-Proof?

- Was the trust drafted by a California-qualified attorney?

- Did you file all required IRS and CA forms the year you funded it?

- Did you obtain an IRS-qualified appraisal, updated for 2026?

- Did you allocate the deduction based only on amount passing to charity (not your family)?

- Is each recipient’s share reported separately on Form 709 (if needed)?

Document every step and save copies for at least 7 years. If you’re unsure, get your trust, filings, and gifting blueprint reviewed immediately.

What If My Assets Include Crypto or Nontraditional Investments?

Many high-income Californians now hold partnership interests, crypto wallets, or startup shares that are difficult to appraise. The IRS allows these in CRTs, but two requirements must be met:

- Obtain an independent, IRS-recognized appraisal. “Fair market value” is required, not your best guess.

- Document the transfer with detailed records—transaction ID (for crypto), transfer deed, or capital account proof for business interests.

Failure to meet either standard can result in the deduction being denied or the entire transfer treated as an undisclosed gift, with 40% tax due after your lifetime exemption is exhausted.

Pro Tip:

For taxpayers with large crypto gains or closely held businesses, consider pairing a CRT with a DAF to sequence deductions, give gradually, and manage payout timing. This helps lock in deductions before thresholds tighten after 2026.

FAQs: CRTs and Gift Tax in California—What Next?

Do You Need an Attorney to Set Up a CRT?

Yes—DIY CRTs fail at a high rate, especially for non-cash assets. If you transfer CA real estate, a California-qualified attorney is essential to avoid FTB penalties and IRS reclassification.

How Fast Should I Act Before the Law Changes Again?

Because several popular deductions are narrowing after 2026, now is the optimal window to deploy a CRT strategy. Funding this year often captures a larger deduction and avoids coming reporting rules.

Can a CRT Lower My California Income Tax This Year?

Yes—in many cases, CRT deductions lower state taxable income, though California runs its own conformity checks. Get updated projections as the Billionaire Tax Act approaches.

If I Expatriate, Can I Use a CRT to Dodge the Exit Tax?

No—recently updated Form 8854 and IRS rules mean all CRT transactions must be reported and justified. Attempting to “pre-pack” gifts before renouncing US citizenship almost always results in extra IRS scrutiny and paperwork.

What’s the Penalty for Missing a Required IRS or FTB Form?

Late or omitted Form 709 (gift tax return) brings a 25% penalty on underpaid gift tax, plus interest. Omitted CRT disclosures on trust or charity filings can trigger retroactive tax and trust invalidation. Document everything or face costly audit risk.

Book Your Gift Tax Strategy Session

Don’t risk a single misfiled trust or missed deduction in 2026. Our experts engineer CRT and gifting strategies that stand up to IRS and state scrutiny—so you keep your wealth working for you and your legacy. Book a private consultation and secure your tax advantage here.