Cracking the Code: MACRS Depreciation for Schedule C in 2024—California’s Self-Employed Playbook for Immediate Write-Offs

It’s the write-off almost every California solopreneur misses: properly optimizing MACRS depreciation for Schedule C 2024 California filers. The result? Overpaying by thousands every year thanks to fear of IRS scrutiny and misunderstanding the “depreciation vs. expense” dance. But here’s the turn—when you understand how to harness MACRS, you’ll unlock immediate cash flow, minimize audit risk, and put your home office, computer, car, and equipment to work remodeling your bottom line.

Quick Answer: For tax year 2024, if you’re filing Schedule C as a self-employed professional in California, the Modified Accelerated Cost Recovery System (MACRS) lets you deduct the declining value of most business-use property—like computers, furniture, and vehicles—rather than writing it off all at once. Doing this accurately means bigger refunds and beefier cash flow, but only if you follow the right asset class, in-service rules, and IRS documentation standards. Miss a step and you risk missing five-figure savings or drawing a red flag in audit season. (See IRS Publication 946 for full MACRS rules.)

For California filers, MACRS depreciation for schedule C 2024 California is less about speed and more about defensibility. The IRS treats MACRS as the default method for tangible business property, which means returns using proper asset lives and Form 4562 schedules generally face less scrutiny than aggressive one-year expensing. When your depreciation matches IRS tables and California Form 3885, you reduce audit risk while preserving deductions for higher-income future years. That trade-off is often intentional—and smart.

This information is current as of 1/18/2026. Tax laws change frequently. Verify updates with the IRS or FTB if reading this later.

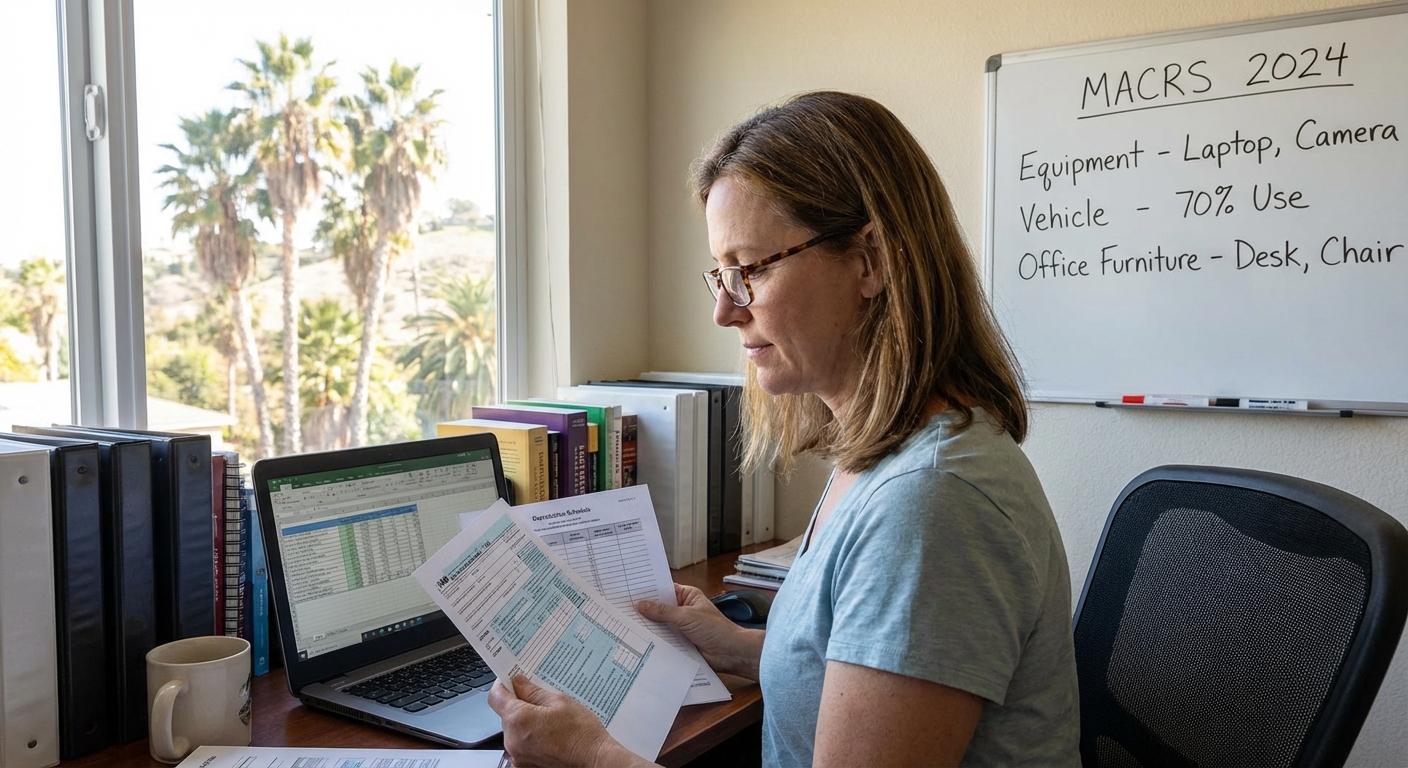

What MACRS Depreciation Means for Schedule C Filers in California

Every time you purchase equipment, computers, or vehicles for your business, you have two core options: deduct it now (through Section 179 if eligible) or spread the value across multiple years using MACRS depreciation. The IRS designed MACRS as the default for most tangible assets—giving you structured, year-by-year deductions that can often be “accelerated” in the early years for bigger initial tax breaks.

Under MACRS depreciation for schedule C 2024 California, most equipment defaults to the 200% declining balance method with a half-year convention unless you elect otherwise on IRS Form 4562. Computers and electronics fall into 5-year property, furniture into 7-year, and light vehicles into 5-year property—but only for the documented business-use percentage. California generally conforms to these asset lives but forces separate calculations when bonus depreciation or large Section 179 elections are used federally. That split is where most self-employed filers make expensive mistakes.

For a California self-employed designer who buys a $2,500 MacBook in March 2024, using MACRS means:

- Classifying the computer as a 5-year property asset

- Claiming about 20% as a first-year deduction ($500), then scheduled amounts for years 2-5 following the MACRS table

- If you choose bonus depreciation for 2024 (if allowed), you might write off 100% in year one—but with state adjustments in California

Unlike Section 179, MACRS does NOT have the same strict dollar limits per year (see IRS Publication 946). However, California often decouples from the IRS on bonus depreciation, so always check the current Franchise Tax Board (FTB) updates: some expensing allowed federally may be limited or deferred for your CA state return.

If you’re an independent engineer or digital agency, structured MACRS deductions—even if smaller per year—often beat big write-offs for audit protection and stable cash flow.

Persona-Based MACRS Scenarios: Who Gets the Most from 2024 Rules?

Let’s get specific. Here are real-world profiles to show how the right approach to MACRS depreciation for Schedule C 2024 California can add up fast for various self-employed taxpayers:

- 1099 Consultant: Buys $8,000 in hardware (laptop, external monitor, printer). Depreciates $1,600 in year one, leaving more deductions for future years—critical if their income will increase (likely moving into higher brackets).

- Real Estate Professional: Picks up home office equipment and staging materials worth $4,200. Uses MACRS over 5 years for $840 year one deduction, with the rest smoothing out income/stress across years.

- Sole Prop Therapist (using LLC): Purchases a $25,000 used therapy couch and decor package. MACRS allows for a more measured deduction schedule, reducing IRS scrutiny compared to an all-at-once Section 179 claim.

Many self-employed professionals get tripped up by confusing asset lives or by not keeping records of how business (not personal) each asset’s use really is. This is especially true for vehicles—where writing off depreciation can get very complex fast.

Pro Tip: Use the small business tax calculator to estimate your exact depreciation tax impact as you plan purchases.

KDA Case Study: California 1099 Consultant Avoids $10K Audit HIT Using MACRS Correctly

Danielle, a Bay Area independent tech consultant, grossed about $180,000 in 2024 and had a habit of depreciating all her business assets in one year for “maximum refund.” Problem: this pattern flagged her for IRS and state review after claiming $22,000 in one-time deductions on Schedule C last year.

When Danielle came to KDA, here’s what we did:

- Reclassified all 2024 purchases by real MACRS asset life (computers: 5 years, desks: 7 years, vehicle: 5 years for business portion only)

- Correctly allocated personal vs. business use and adjusted prior-year returns

- Shifted $12,000 of “one-time” write-off into MACRS depreciation, spreading deductions over future years and staying 100% audit-compliant

- Net result: Danielle’s risk score was reduced, her return flagged as normal, and she’s on track to save $3,250 on 2025 taxes—at a cost of $1,800 for KDA’s work. ROI = 1.8x (first year), with far lower audit risk for years to come

Ready to see how we can help you? Explore more success stories on our case studies page to discover proven strategies that have saved our clients thousands in taxes.

Getting Documented: MACRS Records and IRS Must-Haves

If you want to defend your MACRS deductions in an audit, every asset must have:

- Date placed in service (usually when first used for business)

- Purchase price—including sales tax, shipping, setup fees

- Classified asset life per IRS Publication 946 table (5 years for computers, 7 for furniture, 5 for light vehicles)

- Percentage used for business if mixed-use (e.g., vehicle, phone)

- Year-by-year deduction schedule using 200% declining balance (default for most MACRS federal claims)

Most CPAs never demand this until you get the IRS letter. The better play: set up a “business assets” spreadsheet the day you make your purchase, logging everything. If you sell or dispose of the property, update the schedule—because the IRS could claw back prior deductions on the day you stop using an item for work.

For comprehensive help on deductions, see our tax planning services — we’ll set up or audit-proof your depreciation schedules so you’re always in the clear.

For a summary of asset lives and depreciation rates by property type, refer to the California business owner tax strategy hub.

The CA Twist: State Rules That Trip Up Most Schedule C Filers

California decouples from federal bonus depreciation—while you may claim 100% bonus depreciation for many items on your federal return, California usually says “not so fast.” For the 2024 filing year, CA generally follows MACRS for depreciation lives, but does not allow instant bonus depreciation or Section 179 expensing over certain amounts ($25,000 aggregate limit for Section 179 on the CA return). Pay close attention to the IRS vs. California divide:

- If you buy a $30,000 van for business: Federal MACRS may allow almost full expensing in year one (using bonus depreciation), but CA limits you to classic MACRS schedules, spreading the write-off over multiple years.

- Failing to properly “add back” bonus depreciation on your California return is a major audit trigger for 1099s and LLCs.

Always file California Form 3885 with your state return if you’re claiming business depreciation. Missing this triggers penalties and reversed deductions during state audits.

Business owners looking for a more strategic setup should consider our business owner tax help.

Common Mistake That Triggers an Audit: Improper Asset Classification

Here’s the silent killer: treating all business purchases as short-lived assets (or worse, expensing them outright even when they clearly don’t qualify). The IRS routinely snags California Schedule C filers for:

- Depreciating assets for too short a period (claiming 3 years instead of 5, for example)

- Mixing up business and personal use (writing off the full value of a computer used 60% for family Netflix, 40% for business—IRS says only 40% may be depreciated)

- Not keeping a depreciation schedule or missing mandatory forms (Schedule C, Form 4562 for federal, Form 3885 for CA)

Red Flag Alert: If the IRS audits your return, they’ll demand to see every invoice, business use calculation, and year-by-year depreciation. If records aren’t available—or worse, assets have been disposed and not tracked—expect to repay past deductions plus penalties and interest. (See IRS Form 4562 guidance.)

Pro Tips, Shortcuts, and Social-Share Mic Drop

Pro Tip: Using Section 179 and MACRS together can deliver the best of both worlds—but requires precise calculations and tracking. Never let your tax software “auto-complete” these fields unless you’ve cross-checked with IRS depreciation tables.

Shortcut: For vehicles, if you use the Standard Mileage Rate (67 cents/mile in 2024 for business miles), you generally cannot depreciate the vehicle—choose actual expense if you want to deduct MACRS depreciation.

Mic Drop: The IRS isn’t hiding MACRS write-offs—the rules are published. Most pros overpay because they never learn how to classify, schedule, and defend their business assets.

FAQs: MACRS Depreciation for California Schedule C Filers

How do I know if my property is MACRS-eligible?

Almost any tangible property with a useful life over one year (excluding land) placed into service after 1986 is eligible. Common assets: computers, furniture, machinery, vehicles.

Can I use MACRS for my home office?

You generally can’t depreciate your actual house under MACRS for Schedule C, but you can depreciate office-specific items like furniture, computers, and eligible improvements to the office area.

What if I sell or dispose of an asset early?

You must report the sale/disposition; remaining depreciation stops, and you may have to recognize gain or loss (IRS Form 4797).

Does MACRS look different on federal vs. CA forms?

Yes—California limits bonus depreciation and Section 179 more sharply than the IRS. For 2024, you’ll need to recalculate and likely “add back” deductions on your state return for some assets.

What records do I need for audit-proof depreciation?

Receipts, business use log (especially for vehicles), asset life table (from IRS Publication 946), and Form 4562 completed annually.

Book Your Self-Employed Tax Optimization Session

If you’re filing Schedule C as a California solopreneur or 1099 and worried you’ve missed out on the depreciation bonanza—let’s audit your 2024 asset list together. Book your tailored strategy call and get a step-by-step plan for legal, auditable deductions that protect every dollar you’ve earned. Click here to book your consultation now.