Quick Answer

For 2026, California tax brackets for single filers range from 1% on the first $10,412 of taxable income to 13.3% on amounts over $1,000,000. Understanding where your income falls in these brackets is critical because California uses a progressive tax system that taxes different portions of your income at different rates. Most single filers don’t realize that strategic income timing, deduction stacking, and entity structuring can drop them into lower brackets and save $3,000 to $15,000+ annually.

Why California’s Tax Brackets Hit Single Filers Harder Than You Think

If you’re a single filer in California earning $85,000 as a W-2 employee, you might assume you’re solidly in the “middle class” for tax purposes. You’re not. California’s aggressive progressive tax structure means you’re already paying a 9.3% state marginal rate on income above $66,295, plus federal taxes on top.

Here’s the tension: California has the highest state income tax in the nation, yet most single filers leave thousands on the table every year because they don’t understand how to work the bracket system. The turn? Once you know where the bracket thresholds sit, you can use legal strategies to keep income below key breakpoints or shift it into lower-taxed years.

Most tax software won’t tell you this. Your employer certainly won’t. But if you’re a single filer pulling $60,000 to $150,000 in California, this is the guide that shows you exactly how the 2026 brackets work and what to do about them.

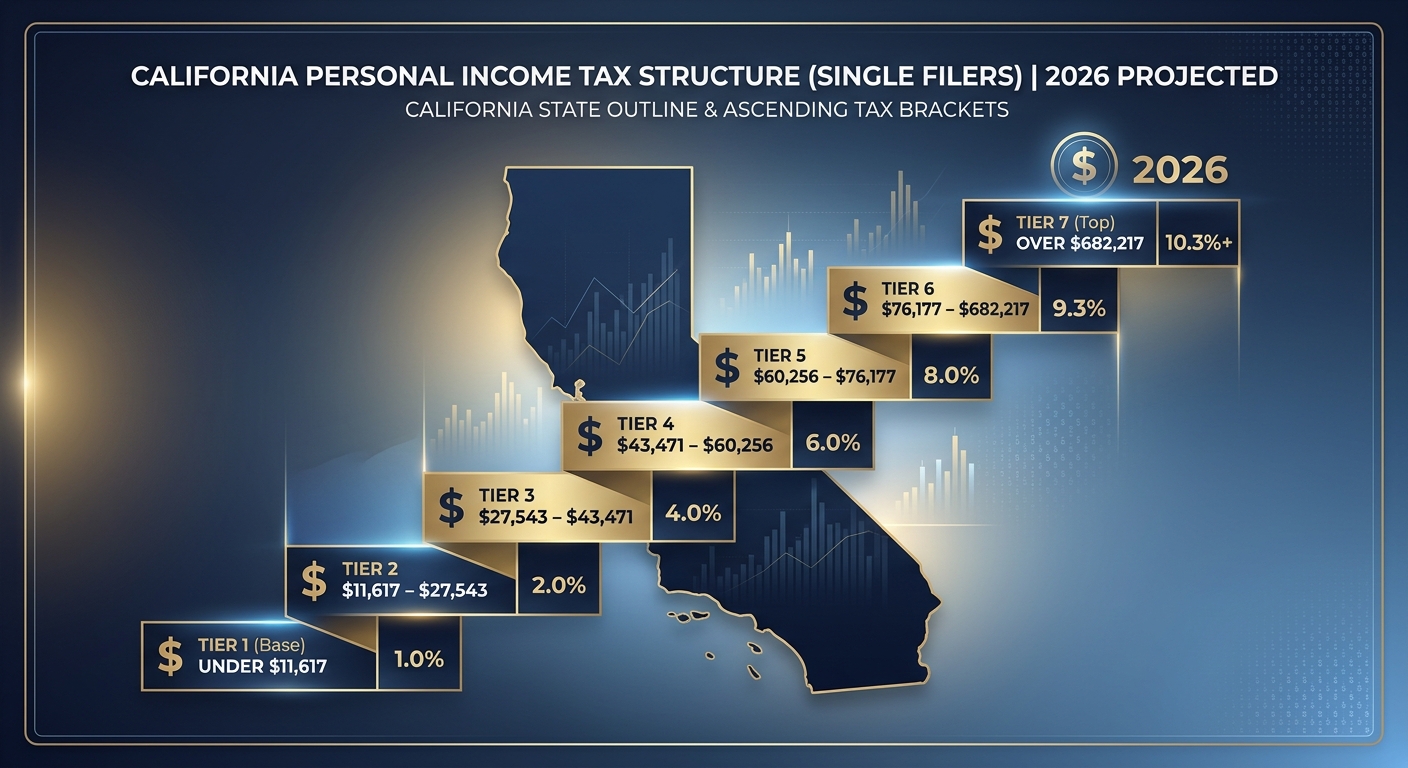

The 2026 California Tax Brackets for Single Filers (Complete Breakdown)

California taxes single filers using nine brackets. Here’s the full structure for 2026:

| Taxable Income Range | Marginal Tax Rate |

|---|---|

| $0 to $10,412 | 1% |

| $10,413 to $24,684 | 2% |

| $24,685 to $38,959 | 4% |

| $38,960 to $54,081 | 6% |

| $54,082 to $66,295 | 8% |

| $66,296 to $338,639 | 9.3% |

| $338,640 to $406,364 | 10.3% |

| $406,365 to $677,275 | 11.3% |

| $677,276 and above | 12.3% |

| $1,000,000 and above | 13.3% |

What This Means in Real Dollars

Let’s say you’re a software engineer in San Francisco earning $95,000 as a single filer. Your California state tax liability breaks down like this:

- First $10,412 taxed at 1% = $104

- Next $14,272 taxed at 2% = $285

- Next $14,275 taxed at 4% = $571

- Next $15,122 taxed at 6% = $907

- Next $12,214 taxed at 8% = $977

- Remaining $28,705 taxed at 9.3% = $2,670

Total California state tax: $5,514

Now here’s where it gets interesting. If you could reduce your taxable income by just $5,000 through retirement contributions or business deductions, you’d save $465 in state taxes alone (9.3% of $5,000). Add federal savings of 22% ($1,100) and you’re looking at $1,565 in total tax savings from a $5,000 deduction.

The Bracket Jumps That Cost Single Filers the Most

Not all bracket increases are created equal. California has three threshold jumps that cause the most financial pain for single filers:

The $66,296 Cliff (8% to 9.3%)

This is the steepest percentage jump in California’s tax code. Once your taxable income crosses $66,295, every additional dollar gets taxed at 9.3% instead of 8%. For someone earning $75,000, that’s $8,705 of income taxed at the higher rate, costing an extra $113 compared to if it were all taxed at 8%.

Red Flag Alert: If you’re a single filer hovering right around $70,000 in taxable income, you’re in the danger zone. A year-end bonus, RSU vesting, or freelance side income could all push you over this threshold. The solution? Max out your 401(k) contributions or open a SEP IRA if you have self-employment income.

The $338,640 Professional Penalty (9.3% to 10.3%)

This bracket hits high-earning W-2 professionals hard. Doctors, lawyers, engineers, and tech workers earning $350,000 to $500,000 often don’t realize they’re paying an extra 1% on every dollar above $338,640. On $450,000 of income, that’s $111,360 taxed at 10.3% or higher.

Pro Tip: If you’re in this income range and operating as a 1099 consultant or side business owner, electing S Corp status and setting up a Solo 401(k) can shelter up to $72,000 in 2026 ($24,500 employee contribution + $47,500 employer contribution for those under 50). That alone saves $7,416 in California state taxes.

The $1,000,000 Millionaire Surcharge (12.3% to 13.3%)

California imposes an additional 1% mental health services tax on income over $1,000,000. If you’re a business owner, real estate investor, or equity holder with a large liquidity event, this bracket can cost you $133,000 in state taxes on every $1,000,000 of taxable income.

Strategic Defense: Spread capital gains events across multiple tax years. If you’re selling a business for $3,000,000, structure the deal as an installment sale over three years. Instead of paying 13.3% on the full amount in one year, you keep portions in the 12.3% or even 11.3% brackets.

How the 2026 Standard Deduction Impacts Your Bracket Position

For 2026, California’s standard deduction for single filers is $5,363. This amount is subtracted from your gross income before calculating your taxable income and determining which bracket you fall into.

Here’s what that means: If you earn $75,000 in gross income and take the standard deduction, your taxable income drops to $69,637. That puts you in the 9.3% bracket instead of being close to any higher threshold.

When Itemizing Beats the Standard Deduction

California allows you to itemize deductions separately from your federal return. This matters if you have:

- Mortgage interest over $5,363

- State and local taxes (SALT) paid if you also have property taxes

- Charitable contributions over 10% of your income

- Unreimbursed medical expenses exceeding 7.5% of AGI

Let’s say you’re a single filer earning $110,000 with $8,500 in mortgage interest and $3,200 in property taxes. Your total itemized deductions are $11,700. By itemizing, you reduce your California taxable income by an additional $6,337 compared to the standard deduction ($11,700 – $5,363). At the 9.3% bracket, that saves you $589.

Pro Tip: California doesn’t conform to the federal $10,000 SALT cap that was raised to $40,000 under the One Big Beautiful Bill Act. On your California return, you can still deduct the full amount of state income taxes and property taxes paid, which often makes itemizing more valuable at the state level even if you take the standard deduction federally.

Strategic Moves Single Filers Use to Drop Tax Brackets

The wealthiest Californians don’t just accept their bracket. They use these four strategies to legally reduce their taxable income and slide into lower tiers:

1. Max Out All Retirement Accounts First

For 2026, single filers can contribute:

- 401(k): $24,500 if under 50, $32,500 if 50-59, $35,750 if 60-63

- Traditional IRA: $7,500 if under 50, $8,600 if 50+

- HSA: $4,400 for individual coverage

A 35-year-old single filer earning $95,000 who maxes out a 401(k) ($24,500) and HSA ($4,400) reduces taxable income to $66,100. That drops them from the 9.3% bracket down to the 8% bracket on the last dollars, saving $318 on those contributions alone.

2. Harvest Capital Losses Before Year-End

California taxes capital gains as ordinary income, unlike the federal government. If you’re sitting on losing stock positions, you can sell them to offset gains and reduce your California taxable income by up to $3,000 per year.

Example: You’re a single filer in the 9.3% California bracket. You sell losing stocks for a $3,000 capital loss. That saves you $279 in California taxes (9.3% of $3,000) plus $660 in federal taxes (22% bracket), totaling $939 in tax savings.

3. Shift Income to a Lower-Tax Year

If you’re a 1099 contractor or small business owner, you control when you invoice and receive payment. If you know 2026 will be a high-income year but 2027 will be lower (maybe you’re taking time off or pivoting to a new business), delay December invoices until January 2027. That income gets taxed in 2027 when you might be in an 8% or even 6% California bracket instead of 9.3%.

4. Take Advantage of California Tax Credits

California offers several credits that directly reduce your tax bill, not just your taxable income:

- Renters Credit: $60 if your gross income is under $49,220

- Child and Dependent Care Credit: Based on federal credit amount

- Solar Energy System Credit: Available for certain installations

These credits come off your final tax bill dollar-for-dollar, which is more valuable than a deduction. A $500 tax credit saves you $500. A $500 deduction at the 9.3% bracket saves you $46.50.

KDA Case Study: W-2 Employee

Jennifer is a 34-year-old product manager at a Bay Area tech company earning $125,000 as a W-2 employee. She came to KDA in March 2026 after realizing she’d owe $3,800 in California state taxes on top of her federal bill.

Her taxable income was $119,637 after the standard deduction, putting her solidly in the 9.3% bracket. She had no retirement contributions set up and was taking the default 6% into her 401(k) for the company match.

What KDA did: We immediately increased her 401(k) contributions to the 2026 max of $24,500. We also enrolled her in her company’s HSA (she was on a high-deductible health plan but didn’t know she qualified) and contributed the full $4,400. We helped her document a small freelance consulting side project she’d done for $2,800 and set up a Solo 401(k) to shelter that income.

Tax savings result: Her taxable income dropped from $119,637 to $90,537. That reduced her California tax bill by $2,706 and her federal bill by an additional $3,850. Total first-year savings: $6,556.

What she paid: $2,400 for tax planning and preparation.

ROI: 2.7x return in year one, plus ongoing savings every year she maintains this structure.

Ready to see how we can help you? Explore more success stories on our case studies page to discover proven strategies that have saved our clients thousands in taxes.

Special Situations and Edge Cases for Single Filers

Part-Year Residents and Bracket Calculation

If you moved to California mid-year or left the state partway through 2026, you’re considered a part-year resident. California only taxes the income you earned while physically residing in the state. However, the bracket calculation is based on your full-year income, then prorated.

Example: You moved to California on July 1, 2026, and earned $50,000 in California plus $50,000 in Texas (before the move). Your total income is $100,000, but California only taxes the $50,000 earned as a resident. The bracket calculation uses your full $100,000 income to determine the rate, then applies it to the $50,000 California-source income.

RSU Vesting and Bracket Spikes

Tech workers with restricted stock units face a unique challenge. When RSUs vest, they’re taxed as ordinary income at your marginal rate. If $40,000 in RSUs vest in one day, that’s $40,000 added to your California taxable income at 9.3% or higher.

Pro Tip: If your company allows it, stagger RSU vesting across two calendar years. Instead of having $80,000 vest in December 2026, split it so $40,000 vests in December 2026 and $40,000 vests in January 2027. If you can also make a large 401(k) contribution in the second year, you keep more income in lower brackets.

Married Filing Separately vs. Single

If you’re married but considering filing separately, know that California’s brackets for Married Filing Separately are identical to Single filer brackets. The difference is that each spouse reports their own income separately. This rarely saves money unless one spouse has significant medical expenses or miscellaneous deductions that are limited by AGI thresholds.

What Happens If You Miscalculate Your California Bracket?

Underpaying California taxes triggers penalties and interest. If you owe more than $500 when you file, California charges an underpayment penalty of 5% plus interest (currently around 3% annually). On a $5,000 underpayment, that’s $250 in penalties plus $150 in interest, or $400 total.

Red Flag Alert: This hits 1099 contractors and gig workers the hardest. If you’re not making quarterly estimated tax payments and you owe California more than $500 at filing time, you’re almost guaranteed to face penalties. The solution is to make quarterly payments using Form 540-ES based on your expected annual income and bracket position.

How to Avoid Underpayment Penalties

California requires you to pay the smaller of:

- 90% of your current year tax liability, or

- 100% of your prior year tax liability (110% if your prior year AGI was over $150,000)

The easiest safe harbor: If you paid $8,000 in California taxes last year, make sure you pay at least $8,000 in withholding or estimated payments this year. Even if you end up owing more, you won’t face penalties as long as you hit that threshold.

Many single filers in California are navigating complex self-employment scenarios or business growth. If you need strategic support with quarterly planning, entity optimization, or compliance, check out our tax planning services designed specifically for California taxpayers.

California-Specific Considerations for 2026

FTB Conformity with Federal Tax Law

California does not automatically conform to federal tax law changes. The One Big Beautiful Bill Act passed in 2025 created new federal deductions for tips, overtime, senior income, and auto loan interest. However, California has not adopted these deductions as of April 2026.

What this means: You might get a federal deduction for tip income that lowers your federal taxable income, but California will add that income back when calculating your state tax liability. Your California taxable income will be higher than your federal taxable income.

The Proposed Billionaire Tax and Single Filers

While the proposed one-time 5% billionaire tax applies only to those with net worths over $1 billion as of January 1, 2026, it’s created uncertainty in California tax policy. Single filers earning $500,000+ are watching closely because any expansion of high-earner taxes could impact them in future years.

Current Strategy: If you’re a single filer with income over $400,000 and considering relocating out of California, 2026 is a critical planning year. Establishing residency in a no-income-tax state like Texas, Florida, Nevada, or Washington before a major liquidity event (business sale, large RSU vesting, real estate sale) can save 13.3% in California taxes on that income.

Ready to Reduce Your Tax Bill?

KDA Inc. specializes in strategic tax planning for business owners, S Corps, LLCs, and high-net-worth individuals. Book a personalized consultation and walk away with a clear plan.

Frequently Asked Questions About 2026 California Tax Brackets for Single Filers

Do I pay California taxes on income earned in other states?

It depends. If you’re a California resident, you pay California income tax on all income regardless of where it was earned. California then gives you a credit for taxes paid to other states to avoid double taxation. If you’re a non-resident who only works in California temporarily, you only pay California tax on the income earned while physically in the state.

How do I calculate my California taxable income if it’s different from federal?

Start with your federal adjusted gross income (AGI) from your Form 1040. Then make California-specific adjustments on Schedule CA. Common adjustments include adding back federal deductions California doesn’t recognize (like the new tip and overtime deductions) and subtracting California-specific deductions. Your final California taxable income is what determines your bracket position.

Can I use tax-loss harvesting to drop into a lower California bracket?

Yes. California taxes capital gains as ordinary income, so harvesting capital losses reduces your California taxable income dollar-for-dollar, up to $3,000 per year. If you’re right on the edge of a bracket threshold (like $67,000 when the 9.3% bracket starts at $66,296), realizing a $3,000 capital loss can drop you back into the 8% bracket on a portion of your income.

Are California tax brackets adjusted for inflation each year?

Yes. California adjusts its tax brackets annually based on the California Consumer Price Index. For 2026, brackets increased by approximately 3.2% compared to 2025. This means the income thresholds for each bracket are slightly higher, giving you a bit more room before jumping to the next tax tier.

What’s the difference between marginal and effective tax rate in California?

Your marginal tax rate is the percentage you pay on your last dollar of income (the highest bracket you reach). Your effective tax rate is your total California tax divided by your total taxable income. Example: A single filer with $95,000 in taxable income has a 9.3% marginal rate but an effective rate of only 5.8% because the first $66,295 was taxed at lower rates.

Key Takeaway

Key Takeaway: California’s 2026 tax brackets for single filers create critical threshold points at $66,296, $338,640, and $1,000,000 where strategic income management can save between $3,000 and $15,000+ annually. The most effective strategies involve maximizing retirement contributions, timing income recognition, and understanding California-specific conformity issues with federal tax law changes.

Lock In Your 2026 Tax Savings Before It’s Too Late

If you’re a single filer earning between $60,000 and $400,000 in California and you’re still using basic tax software or a general preparer who doesn’t specialize in California tax strategy, you’re leaving thousands on the table every year. The bracket thresholds in 2026 create clear savings opportunities, but only if you know where to look and how to execute.

Book a personalized tax strategy consultation with our California-focused team and we’ll show you exactly where you fall in the 2026 brackets, which deductions you’re missing, and how to structure your income to keep more of what you earn. Click here to book your consultation now.

This information is current as of April 21, 2026. Tax laws change frequently. Verify updates with the IRS or FTB if reading this later.